Clean cooking finance is becoming easier to talk about, but still harder to count. An IRENA report shows that public financial support across 100 clean cooking access-deficit countries remains limited, fragmented and heavily dependent on domestic budgets, even as governments say grants, concessional loans and stronger policy frameworks are what they need most.

The gap matters acutely for Africa and other emerging markets, where billions still cook with polluting fuels, public-health burdens remain high, and investment timelines are slipping beyond 2030.

The report suggests the real challenge is no longer just mobilising finance, but building the policy certainty and data systems that can attract it at scale.

Finance gaps keep kitchens polluting

An IRENA assessment of 100 clean cooking access-deficit countries finds that tracked finance remains far below what is needed to close one of the world’s most persistent energy poverty gaps.

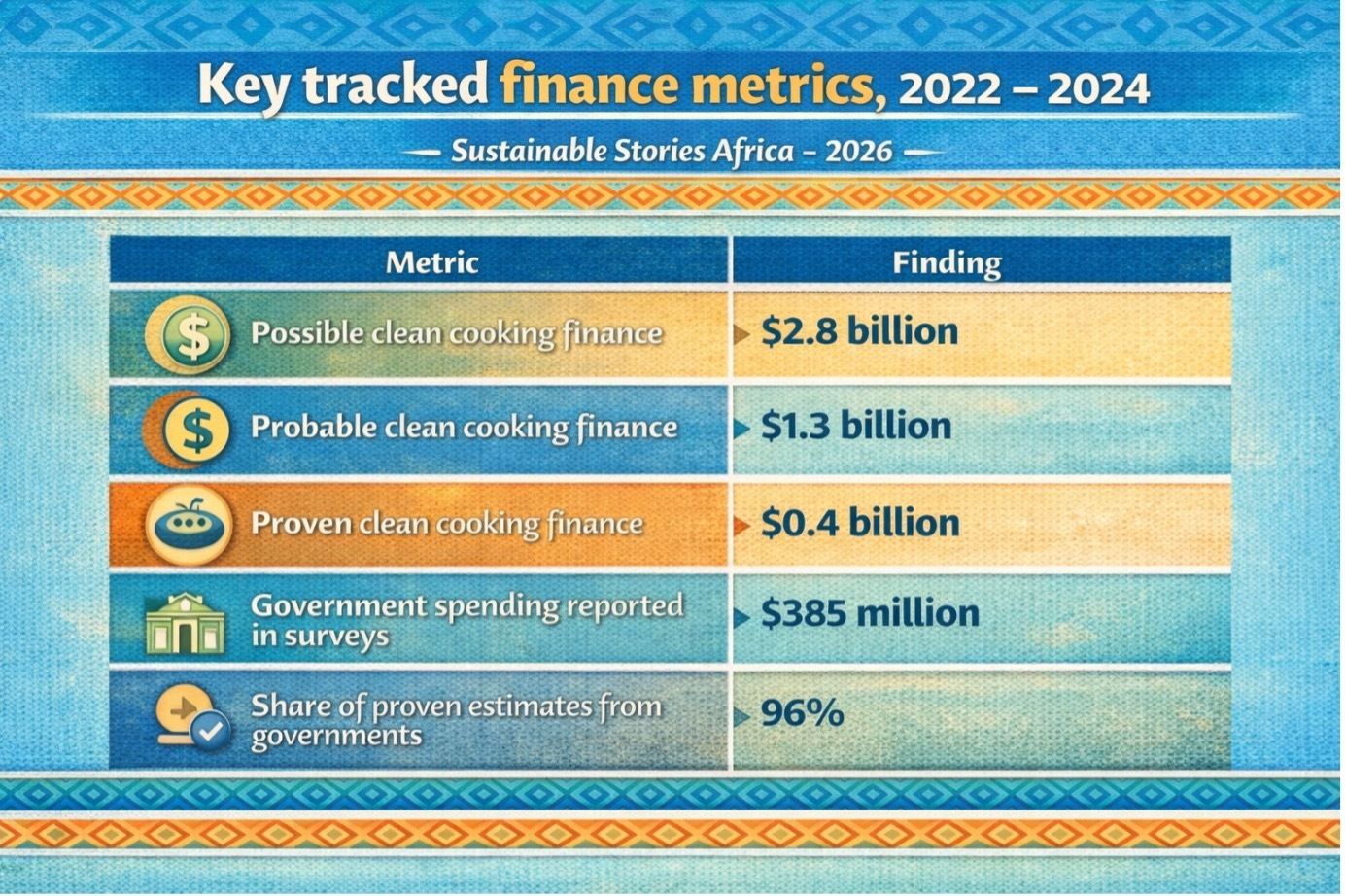

The agency estimates that clean cooking investment across these countries between 2022 and 2024 ranged from a “proven” floor of $0.4 billion to a “possible” ceiling of $2.8 billion, with a “probable” midpoint of $1.3 billion.

The report arrives at a moment when clean cooking is gaining gradual visibility in climate, health care and development debates; however, it still lacks coherent financing records.

IRENA says approximately 2.1 billion people globally still lack access to clean cooking solutions, while financing remains volatile, uneven and often poorly tagged across databases.

For African countries, the stakes are even higher. Sub-Saharan Africa dominates IRENA’s list of the 100 surveyed countries, and the report notes that 27 of them have more than 80% of their population still cooking with polluting fuels, while 22 exceed 90%.

Why the numbers matter now

The report’s core contribution is methodological as much as financial. Rather than pretending precision where none exists, IRENA built a three-tier framework: possible, probable and proven.

- The “possible” estimate captures broader development and energy flows where clean cooking might be embedded.

- The “proven” estimate tracks verified bottom-up investments.

- The “probable” figure extrapolates from known data to the wider group of countries.

That matters because clean cooking finance lies within a messy ecosystem. IRENA says the investment landscape spans at least 26 different financial support flows involving 11 main stakeholder groups.

It also notes that the sector suffers from ambiguous definitions, limited reporting, fragmented datasets and survey fatigue among respondents.

Even so, the report offers some of the clearest public benchmarks now available.

The structure of that finance is revealing.

Government spending reported through IRENA’s surveys totalled $385 million, accounting for 96% of the proven estimate. Within that, two-thirds came from national budgets, and LPG infrastructure absorbed 65% of reported government support, followed by improved biomass cookstoves at 32%.

That suggests two things at once:

- First, governments are still carrying most of the visible burden.

- Second, the sector remains concentrated in relatively established technologies rather than a broad, diversified transition.

Public budgets are carrying too much

IRENA’s survey evidence shows that national budgets remain the main visible source of support, even though governments themselves say self-funding is not the instrument most likely to deliver universal access.

In survey responses, 56% said their countries had used national budgets for clean-cooking-related activities between 2022 and 2024, with LPG the most commonly supported technology.

By contrast, grants and concessional flows were much thinner. Only eight countries confirmed that they allocated grants or concessional funding during the period. Where such support existed, it was spread more widely across emerging technologies, including improved biomass cookstoves, biogas, ethanol and electric cooking.

Debt finance was also limited. IRENA found that only 11 survey responses reported debt capital being used for clean-cooking-related activities between 2022 and 2024, with LPG and improved biomass cookstoves again appearing as the most common recipients.

For policymakers and investors, that is the signal worth watching. The market is not yet financing clean cooking at the scale, speed or diversity needed for a full transition.

What governments say they need

Perhaps the most important part of the report is not what countries spent, but what they said would unlock more spending.

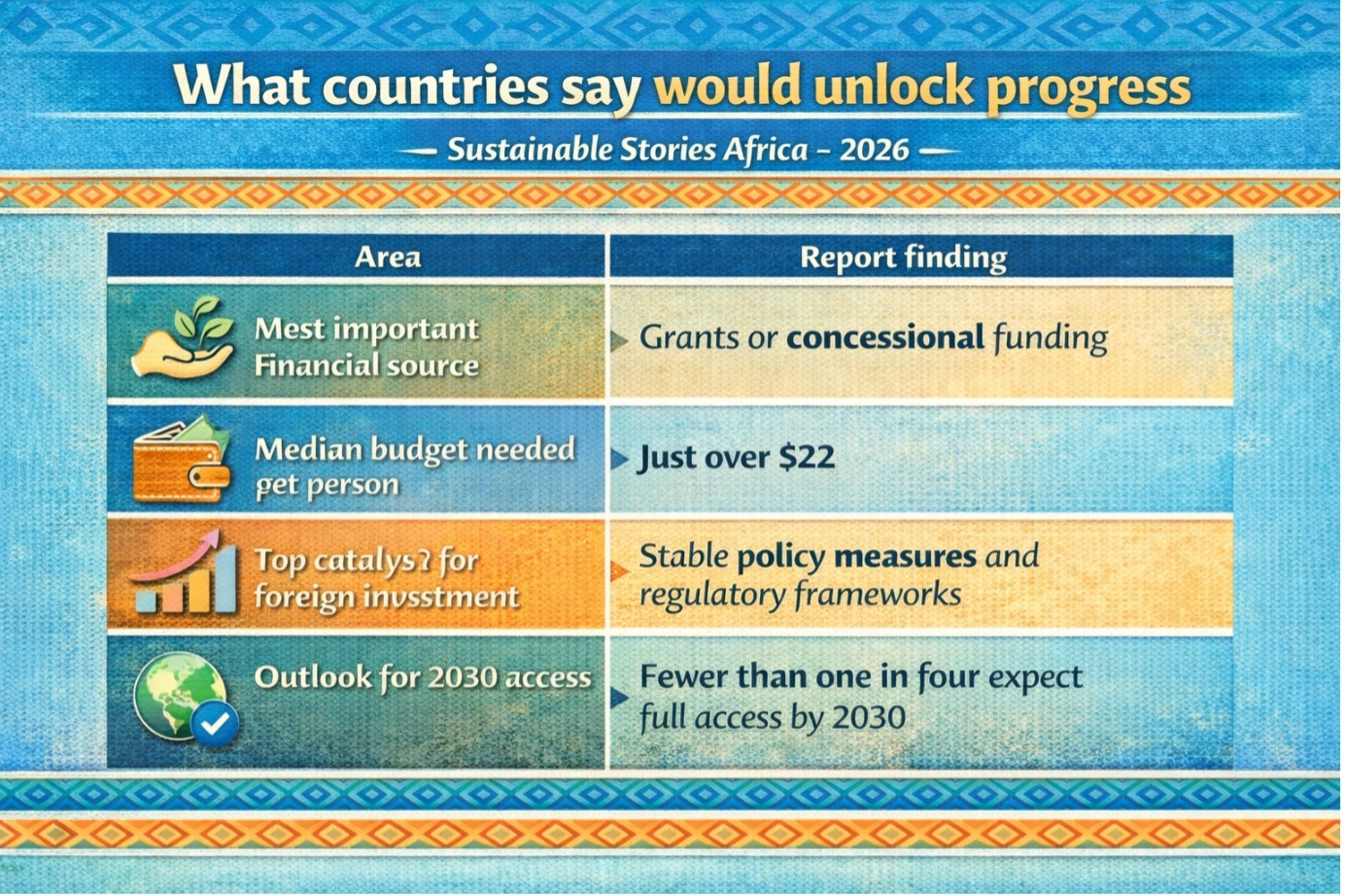

Governments ranked grants or concessional funding as the most important type of finance for achieving full access to clean cooking, ahead of carbon finance, local-currency finance, international-currency finance and taxes.

In IRENA’s survey responses, grants or concessional funding accounted for 28% of the top three types of finance needed, while carbon finance accounted for 24%.

They also put a price, albeit a rough one, on the challenge. Among nine countries that provided data, the median investment needed per person to achieve full access to clean cooking was just over $22; however, needs varied widely, from above $3 to $154 per person.

Respondents said the best way to catalyse foreign investment was not money alone, but also policy.

Policy measures accounted for 34% of suggested interventions, ahead of concessional financing at 32%.

Specific calls included tax incentives, grants, results-based finance, de-risking tools, supportive regulation, infrastructure development and better supply chains.

That aligns with an expanded market truth: investors do not only chase opportunity; they chase predictability.

The opportunity if finance improves

The upside is substantial. Better finance tracking can help governments make a stronger case for clean cooking as an investable, multi-sector priority spanning health, gender, climate, forests, household welfare and industrial policy.

IRENA argues that reliable primary data are essential for better decisions, and that clearer definitions could eventually help OECD DAC and financial institutions tag clean cooking interventions more consistently.

For African markets, the opportunity is especially tangible. The report notes that more than 70% of Africans without access to clean cooking live in countries that have strengthened policy frameworks since 2024, with 40 new policies implemented after the Summit on Clean Cooking in Africa.

That means clean cooking is no longer a neglected side issue. It is increasingly being treated as infrastructure, market design and development policy rolled into one.

Why the 2030 goal still looks distant

Still, the mood in the data is cautious. Fewer than one in four government respondents expect their countries to achieve full access by 2030. Most expect to get there only after 2040, and approximately a third place the milestone beyond 2050.

Confidence is weak: among 23 countries that responded on confidence levels, only seven were optimistic about achieving full access by 2030, seven were doubtful, and nine said they did not know.

That is the clearest warning in the report. Clean cooking has more political visibility than before, but not yet enough bankable momentum.

Path forward – Clean Cooking Gap Needs Policy Finance Alignment

Closing the clean cooking gap will require three moves at once: clearer definitions, stronger domestic policy frameworks and more catalytic concessional finance.

Governments are signalling that finance alone is not enough; investors also need regulatory certainty, workable subsidy design and better delivery systems.

For African markets, the lesson is practical. Track money, reduce policy ambiguity, and use grants and concessional finance to pull in commercial capital.

Without that shift, universal access will remain a summit promise rather than a household reality.