Across African impact portfolios, funds often report jobs created, women reached, and waste diverted. Those figures matter, but the tougher question is whether the evidence underneath them is strong enough to withstand scrutiny.

A verification brief argues that before managers report to investors, deploy more capital or publish ESG disclosures, they should stress-test claims, assess confidence and correct gaps. In a tighter capital environment, proof is becoming part of impact governance itself.

When Numbers Need Stronger Proof

Impact investing has spent years learning how to count. It now speaks fluently in output and outcome metrics: jobs created, women reached, enterprises supported, waste diverted, and water systems functioning. An April 2026 verification brief, How Funds Can Stress-Test Impact Claims, makes a sharper point. Counting is not the same as proving.

Its message is direct and timely. Funds should test claims before reporting to investors, deploying more capital and publishing ESG or impact disclosures. That is because a number can look impressive in a dashboard while the evidence beneath it remains incomplete, inconsistent or weak.

For African and wider Global South markets, that matters more than ever. Impact capital is expected to do two jobs at once: deliver returns and help address urgent deficits in energy access, jobs, water, waste systems and inclusion.

In that context, weakly evidenced claims do not merely create reporting risk. They can distort capital decisions, inflate confidence and weaken trust in markets where credibility is already expensive.

Dashboards Can Hide Fragility

The hook in the brief is deceptively simple: “Results are often reported as numbers.” Across African impact portfolios, those numbers typically include jobs created, women reached, waste diverted, water systems functioning, and enterprises supported. The paper does not dismiss them. It says clearly that “those numbers matter.”

The problem is what comes next. On page three, the brief asks the central governance question: how strong is the evidence behind the claim? It notes that many portfolios operate through layered delivery systems involving portfolio companies, implementation partners, field teams, reporting tools and different definitions of success. In such systems, data may change shape several times before reaching investors.

That is where urgency sits today. ESG and impact claims are increasingly used to secure capital, justify follow-on investments and support public disclosures.

However, if the underlying definitions vary from one portfolio company to another, or if evidence trails are incomplete, the polished portfolio-level figure may be more persuasive than it is reliable. A strong dashboard, in other words, can conceal weak foundations.

For African fund managers, this is not a theoretical concern. Many operate across multiple geographies, work with local partners under uneven reporting conditions, and balance the pressure to show progress with the reality of fragmented data systems.

The more complex the delivery chain, the greater the need for verification discipline.

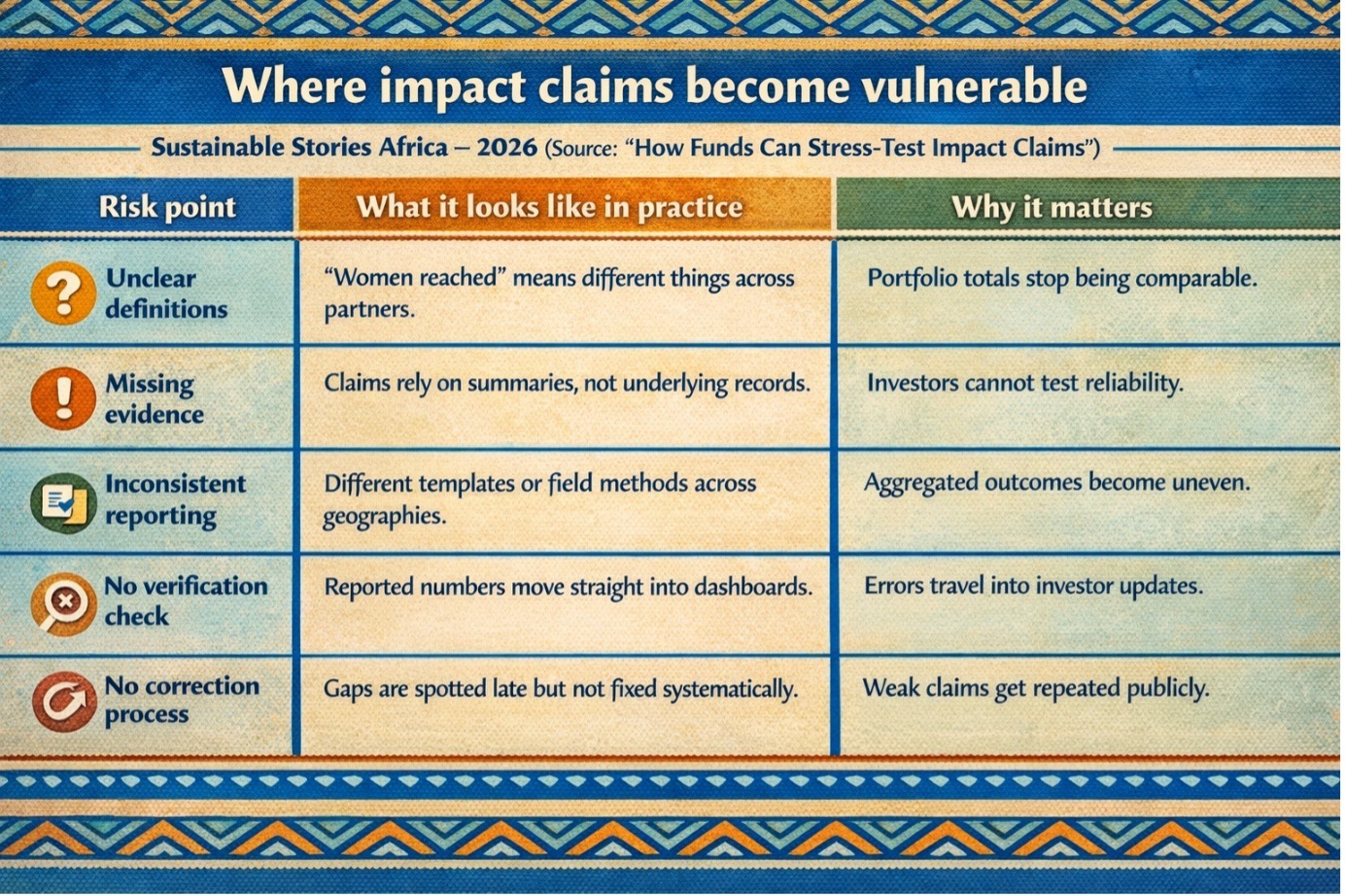

Where Hidden Reporting Risk Builds

The brief is especially valuable because it identifies where risk accumulates. On page four, it says hidden risk starts to build when a claim still has unclear definitions, missing or incomplete evidence, inconsistent partner reporting, no verification check and no correction process.

That list captures several common weaknesses in impact reporting:

This is where the story shifts from compliance to corporate integrity. Impact funds are not just reporting results; they are making representations to investors about social, environmental and development performance.

If those claims are not stress-tested, the fund may overstate certainty, understate execution risk, or unintentionally reward reporting convenience over real-world change.

In African markets, the stakes are wider.

- Communities may be counted but not meaningfully served. Investors may allocate fresh capital based on fragile evidence.

- Regulators and standard setters may respond by hardening expectations around disclosures.

- The impact industry itself risks inviting the same criticism that has trailed parts of ESG reporting globally: too much narrative, too little verification.

What Better Verification Could Unlock

The most constructive part of the brief is that it does not present verification as a brake on capital. On page five, it states plainly that this is “not about slowing reporting down.” It is about making sure a claim is ready to be “trusted, repeated, and defended.”

Better verification can improve more than just disclosure quality. It can sharpen outcome definitions, reveal weak reporting systems early, improve portfolio learning and make future capital deployment more disciplined.

- For investors, it strengthens confidence that reported results reflect real performance.

- For fund managers, it offers a durable base for credibility in a fundraising environment that is becoming more selective.

- For portfolio companies and implementation partners, it clarifies what good evidence actually looks like.

There is also a deeper benefit for African markets. When funds can show that their claims have been tested and corrected before disclosure, they help build an ecosystem where impact is not only promised but evidenced.

That raises the quality bar for the whole market.

The brief also notes that portfolio verification pilots are now open, suggesting that some managers are already moving from theory to implementation.

What Funds Must Do Now

The practical implication is clear. Funds should not wait until the annual reporting season to ask whether a claim is credible. Verification needs to happen before investor reporting, before fresh capital is deployed and before ESG or impact disclosures are published.

That means three immediate shifts.

- First, funds need common definitions across portfolio companies, implementation partners and field teams.

- Second, they need a verification checkpoint that tests whether reported results are supported by underlying evidence.

- Third, they need a correction process so weak claims are repaired before they become repeated facts in dashboards, annual reports and capital discussions.

For investors and limited partners, the signal is equally important. Questions should move beyond “What did the fund achieve?” to “How did the fund verify the claim?”

In a more mature impact market, evidence quality will increasingly shape confidence, valuation and follow-on support.

Path Forward – Through Verifiable Impact

The shift being advocated is straightforward: verify first, report second.

Claims of stress-testing, scoring confidence and closing gaps can help funds protect trust, improve decision-making and strengthen the credibility of impact capital in African markets.

What comes next is not more rhetoric, but better discipline. As impact reporting grows more consequential, funds that can defend their numbers will be better placed to attract capital, support communities credibly and show that impact governance is not a branding exercise, but a measurable operating standard.