The circular economy is no longer just a waste story. A report argues it is a climate, resilience and competitiveness story too; however, capital is far behind the scale of the need.

With at least a $6.5 trillion funding gap to 2035, the central question is no longer whether circularity matters.

It is whether finance, policy and measurement can move quickly enough to make it bankable at scale.

Waste Is Now Capital Question

The circular economy has moved well beyond the old framing of recycling as an environmental afterthought. In Scaling circular finance: No time to waste, Standard Chartered presents circularity as a systems-level economic transition that can reduce dependence on raw materials, lower emissions, improve resilience and create new investment opportunities across major sectors and geographies.

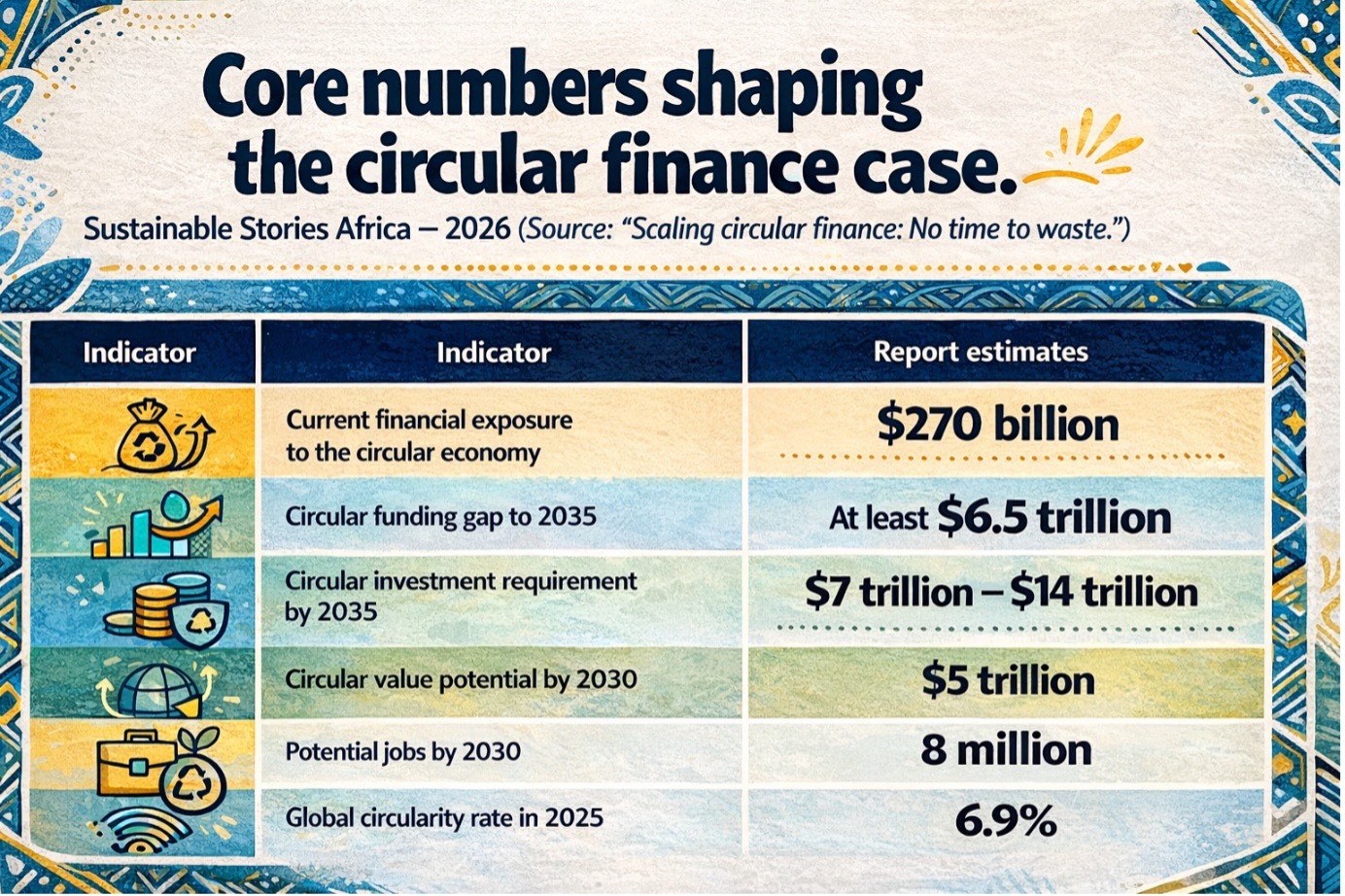

More than 70 governments are already implementing policies and regulations to support it, while the report estimates that over $270 billion of assets have been deployed toward circular solutions and infrastructure.

However, the report headline is not about momentum. It is a scale mismatch. Despite rising policy attention, corporate engagement and innovation. The report estimates a circular funding gap of at least $6.5 trillion for the sectors assessed by 2035.

Total circular investment requirements are put at roughly $7 trillion to $14 trillion by 2035, while current financial exposure remains small by comparison.

For African and other emerging markets, that gap is especially consequential. The report repeatedly links circular finance to infrastructure, waste systems, materials security, emissions reductions and development outcomes, making the case that circularity is not peripheral to sustainability.

It is becoming central to how economies manage growth under resource pressure.

A Trillion-Dollar Gap Widens

Circularity’s appeal in the report lies in the gap between promise and practice. Circular strategies could generate around $5 trillion in value and help create 8 million jobs by 2030; however, mainstream adoption is lagging. The world is only about 6.9% circular in 2025, down from 9.1% in 2018, as virgin material use outpaces reuse.

The costs of staying linear are climbing. Raw material extraction may need to be 60% higher in 2060 than in 2020 under business-as-usual, with total waste generation projected to rise 80% by 2050 and waste management potentially costing $6.7 trillion by mid-century.

The report frames circularity as financial risk management: a hedge against supply volatility, waste costs and carbon exposure.

For hard-to-abate sectors such as steel, cement, concrete and plastics, combining circular strategies with decarbonisation could cut emissions by more than 25%, reduce abatement costs by 45% and lower energy demand by 20%, as the chart on page 11 vividly illustrates.

Why Emerging Markets Matter Most

The report’s central message for African readers is that the Global South is not a passive beneficiary of circularity but the frontline where circular finance will either succeed or stall.

It frames waste management and recycling as core development challenges, noting that many countries still lack the collection, sorting and recovery systems needed to prevent pollution and capture value.

In its business-as-usual scenario, total waste across sampled countries rises to 3.3 trillion tonnes by 2050, with uncontrolled waste more than doubling to 1.5 trillion tonnes, or 45% of the total.

Sub-Saharan Africa is hit hardest, with municipal collection rates as low as 36% and recycling at just 3%, compared with 56% in Europe, and open dumping linked to severe health harms.

Under a circular scenario, waste generation falls to 1.7 trillion tonnes by 2050, as all regions reach 100% collection and zero uncontrolled waste, recycling increases to 70% in Europe and 50% in the Global South, and the global circular waste sector could generate benefits of $912 billion.

What Better Capital Could Unlock

The upside case in the report is compelling because it goes beyond emissions. Circular solutions are framed as resilience tools. They reduce dependence on virgin raw materials, lower exposure to price volatility, improve supply security for critical materials, and create new markets in reuse, repair, remanufacturing, resale and recycling.

For developing countries, there is also a financing innovation story. The report suggests that avoided emissions could become a funding source if circular solutions can demonstrate credible carbon avoidance. In the waste chapter alone, the value of avoided emissions is estimated at USD82 billion, with Africa accounting for USD28 billion, South Asia USD20 billion, and East Asia and Pacific USD15 billion. That is a notable signal: some of the strongest monetisable climate benefits may emerge in regions that are still underfinanced.

The report also points to early market proof. Sustainability-linked bonds and loans tied to circular economy, waste and water projects have reached almost USD119 billion since 2016. Public market interest is also growing, with the number of listed circular economy equity funds rising from fewer than five in 2019 to almost 40 in 2025, alongside nearly 50 broader funds that include circular end markets such as waste, recycling and clean water.

Action: Four Levers For Investment Scale

The report’s policy and market prescription is organised around four levers.

First, stakeholders need to recognise circular economy investments as fundamental to climate and nature targets. That would widen access to green bonds, sustainability-linked loans, climate funds and blended finance by making circular strategies legible within mainstream decarbonisation frameworks. Second, markets need agreement on definitions, principles, measurement and reporting, since the lack of globally accepted standards still makes capital allocation difficult.

Third, circularity needs to be integrated into finance risk models. The report argues that lenders and investors need tools to estimate both circular and non-circular exposure, and to price risks and opportunities accordingly. Fourth, international regulation and policy need more harmonisation so investors and corporates face lower complexity, better economies of scale and more viable cross-border secondary materials markets.

For Africa, one message stands out sharply: international funding will remain essential. The report notes that only 23% of climate finance in Sub-Saharan Africa is domestically sourced, compared with far higher shares in mature markets, suggesting that circular projects will also rely heavily on foreign and public capital until domestic capital markets deepen.

Path Forward – Through Bankable Circularity

The report’s central argument is that circularity will not scale on environmental logic alone.

It needs standards, risk tools, policy coordination and blended capital structures that make projects investable across both mature and emerging markets.

For African markets, the priority is even clearer: build waste and recycling systems, connect circularity to climate and development finance, and lower investor risk fast enough to crowd in larger pools of capital.