The EU has simplified the Corporate Sustainability Reporting Directive, sharply narrowing mandatory reporting scope and delaying obligations for many companies.

However, the reform does not remove sustainability pressure; it changes who must report, when they must report, and how much data they may ask from smaller firms in their value chains.

For African exporters, subsidiaries, lenders and large corporates tied to European markets, the message is clear: formal compliance may now hit fewer companies, but investor, customer and supply-chain expectations are likely to remain high.

Europe redraws the reporting map

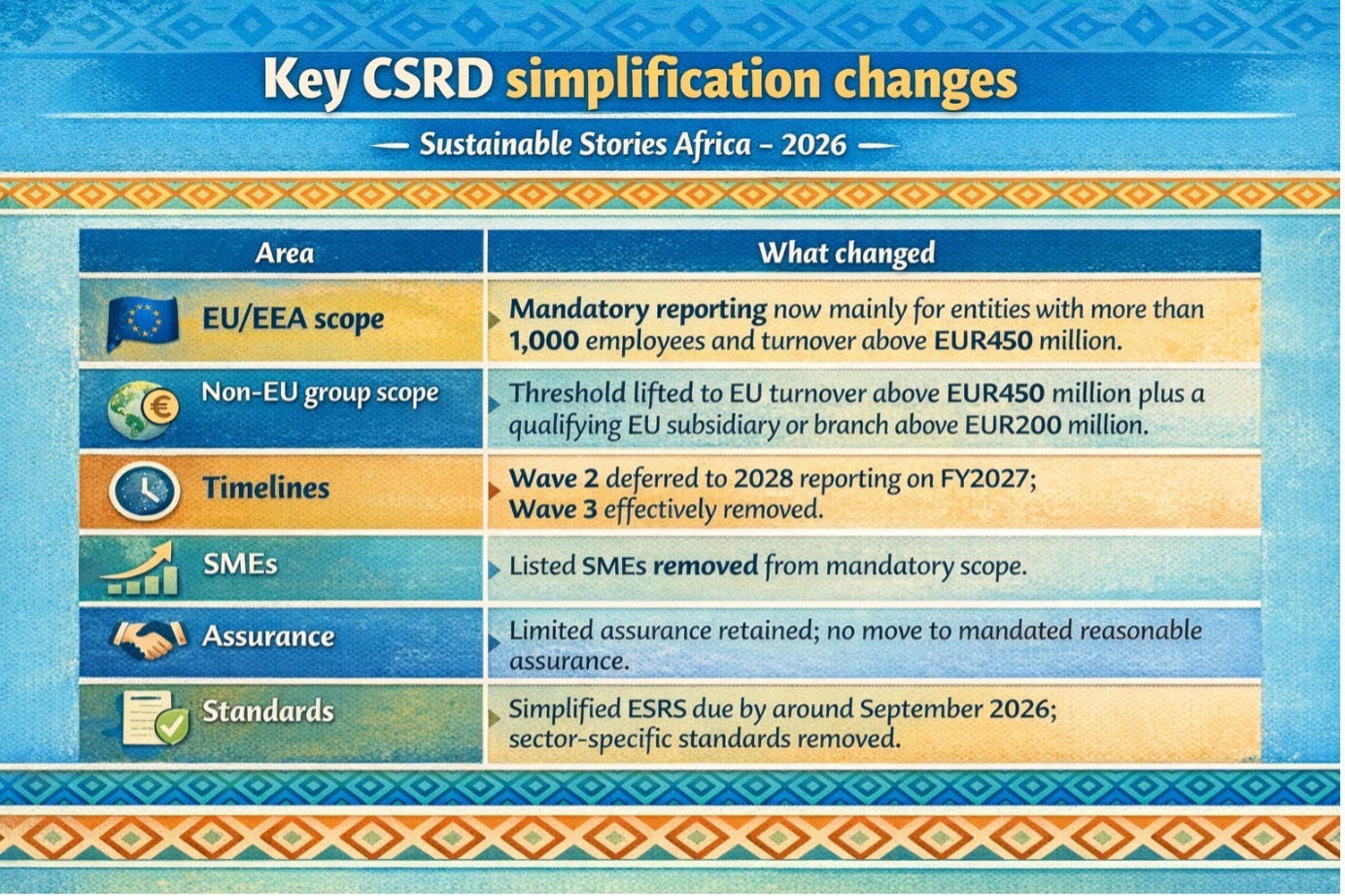

The EU’s revised CSRD regime marks one of the biggest recalibrations yet in sustainability disclosure policy. Under Directive 2026/470, which entered into force on 18 March 2026, mandatory CSRD reporting is now limited mainly to companies with more than 1,000 employees and a turnover of EUR450 million, while Member States have until 19 March 2027 to transpose the new rules into national law.

That is a meaningful reversal from the original design of CSRD, which was built to bring in large companies, listed SMEs and some non-EU groups in phased waves.

The new framework narrows the mandatory net, preserves limited assurance, promises simplified ESRS, removes sector-specific standards, and introduces new protections for smaller businesses in reporting chains.

For Africa and other emerging markets, this matters not because Brussels has suddenly lost interest in sustainability, but because the EU is trying to reduce compliance costs without abandoning transparency.

That balance will shape how European buyers, financiers and multinational groups deal with suppliers and subsidiaries far beyond Europe.

Fewer companies, same direction

The headline number is the scope cut. EY notes that the European Commission had already estimated an up to 80% reduction in the number of reporting entities under its earlier simplification proposal, and says the final text, with thresholds raised further, implies an even greater reduction.

That means many companies that once expected to fall into the CSRD scope will now sit outside it. The listed SMEs are removed from the mandatory scope. Wave 3 is effectively de-scoped.

Wave 2 companies still in scope will now report effective 2028 on their FY2027 data after the earlier “Stop-the-Clock” delay.

However, the strategic direction has not reversed. The revised regime still keeps double materiality for in-scope companies, still requires limited assurance, still expects digital reporting infrastructure to emerge, and still leaves a clear route for voluntary reporting standards for entities with 1,000 employees or fewer.

What exactly has changed

The original CSRD was designed to improve sustainability reporting across the EU, requiring companies to disclose environmental, social and governance impacts using the ESRS, apply double materiality, obtain limited assurance and report across the value chain.

The new directive keeps that architecture, but trims and rearranges it.

There are also value-chain protections. The directive introduces a “value chain cap” that limits what in-scope companies can request from businesses with up to 1,000 employees.

Those smaller firms can refuse requests that go beyond what the Commission’s future voluntary standard will specify.

That matters for African suppliers. Even if they are not directly in scope, they may still face data requests from larger European customers. The difference now is that those requests should, in theory, become more proportionate.

The EU has also widened confidentiality reliefs. Companies may omit certain information if disclosure would seriously prejudice their commercial position, or if the information qualifies as trade secrets, classified material, or protected information under law.

Desire: Why simplification could still help

There is a constructive reading of the reform. A narrower regime could make reporting more credible for the companies that remain in scope by focusing compliance efforts on larger entities with greater capacity, stronger systems and broader market relevance. EY says the simplification agenda is meant to improve competitiveness by reducing administrative burden while still preserving transparency and trust.

If done well, that could help in three ways. First, it may reduce reporting fatigue and excessive data gathering. Second, it could make sustainability reporting more decision-useful by trimming lower-value data points. Third, it may create space for more practical voluntary reporting among mid-sized companies that still need market credibility.

That last point is especially relevant for African firms. A company may no longer be legally required to report under EU law and still decide that voluntary reporting is commercially smart.

EY explicitly warns that investor, customer and financing expectations are likely to remain strong even for out-of-scope companies.

So, the simplification is real, but so is the unfinished work.

What African companies should do now

The practical takeaway is not to relax, but to reclassify readiness

- First, companies with EU exposure should reassess whether they remain legally in scope under the new thresholds, including non-EU parent groups with large EU revenue exposure.

- Second, they should distinguish between legal obligations and market expectations.

- Third, they should prepare for a two-track world: mandatory reporting for fewer very large firms, and voluntary but still influential reporting for many others.

EY’s guidance is blunt. Companies should:

- Assess scope

- Track national transposition risk

- Engage customers higher up the value chain

- Align with voluntary standards and best practices

- Maintain double materiality where still required

- Strengthen governance and data integrity

- Future-proof sustainability strategy.

For African exporters, banks, insurers, telecoms groups and manufacturers, that means asking practical questions now.

- Are European customers likely to ask for emissions, labour, or supply-chain data anyway?

- Can internal systems support credible responses? Is governance strong enough for assurance-readiness?

If the answer is no, the compliance relief in Brussels may offer only temporary comfort.

One more complication remains: Member State transposition. EY notes that as of March 2026, five EU Member States, Germany, Luxembourg, the Netherlands, Portugal and Spain, had still not transposed the original CSRD.

That raises the risk of continued fragmentation as countries implement the revised directive in different ways.

Path forward – EU CSRD Eases; However, Expectations Persist

The EU has made CSRD smaller, not irrelevant. Fewer companies will face mandatory reporting, but large-market buyers, lenders and investors are still likely to demand structured sustainability data across global value chains.

African businesses should use the breathing room wisely:

- Reassess scope

- Strengthen ESG data systems

- Prepare for voluntary reporting

- Watch EU transposition closely

In the new regime, the winners may be the firms that treat simplification as a planning window, rather than a permission slip to stop preparing.