ESG scores often look simple from the outside: one number, one ranking, one signal to investors. But the real story sits inside the methodology.

An EthiFinance methodology shows how ESG ratings are increasingly built around double materiality, sector weighting, controversy penalties and product-impact bonuses.

For African issuers and emerging-market firms, that changes what “good ESG performance” now means.

How ESG scores are really built

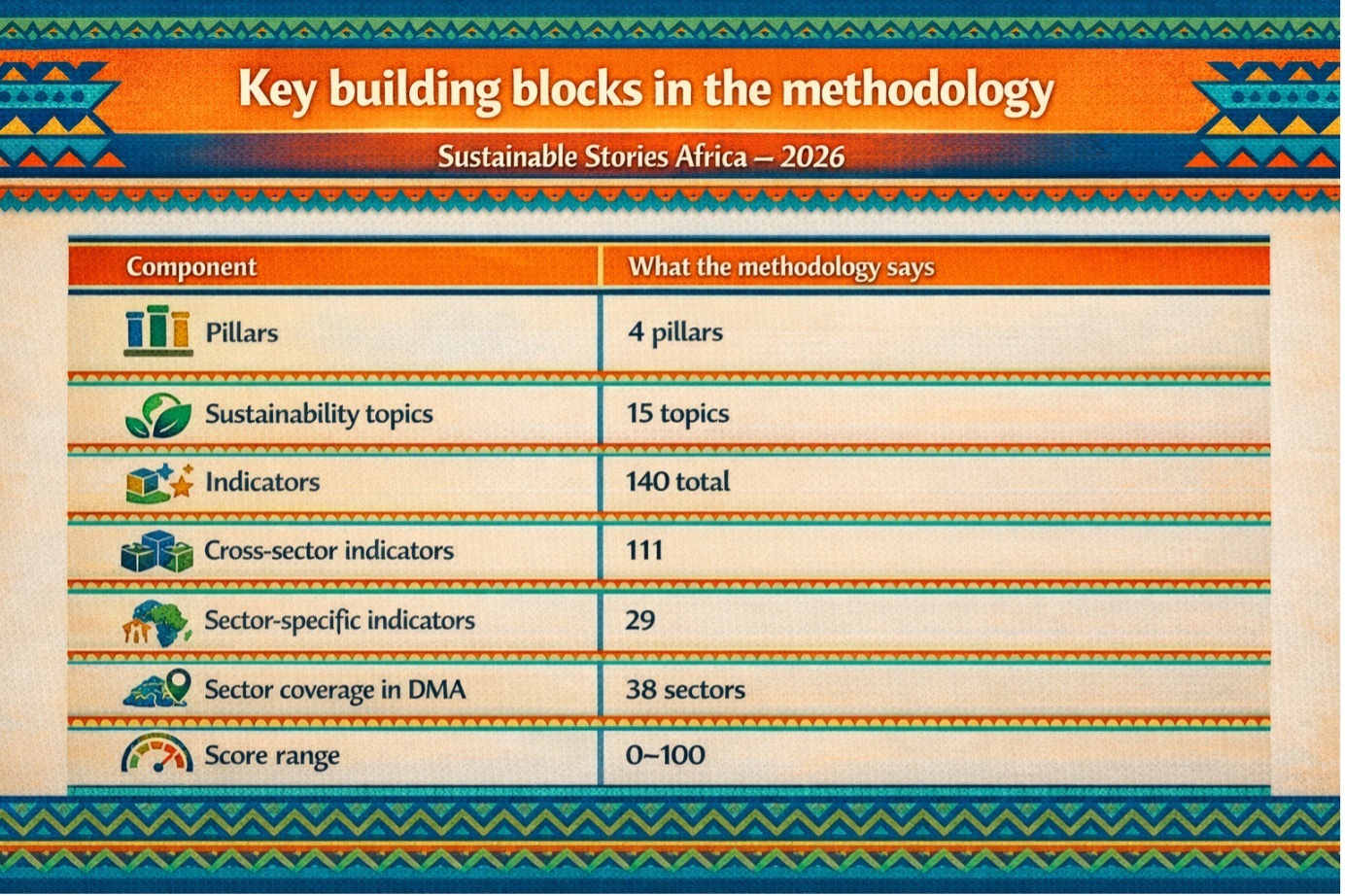

ESG ratings are becoming more technical, more data-heavy and more strategic. EthiFinance’s 2025 ESG Rating Methodology offers a clear look at that shift, setting out how one European rating agency now scores companies across four pillars, 15 sustainability topics, 140 indicators, controversy screening and a bonus for products and services that contribute positively to the UN Sustainable Development Goals.

That matters because ESG ratings increasingly shape how investors, banks and asset managers interpret corporate sustainability performance. They are not simply judging whether a company publishes a climate policy or diversity statement.

They are asking how sector-specific the risks are, how strong the governance is, whether controversies reveal a gap between policy and behaviour, and whether the business model itself contributes to sustainable development.

For African and emerging-market companies, the message is practical. Better reporting helps, but reporting alone is not enough.

The methodology suggests that strong scores now depend on governance quality, performance trends, controversy management, and the reception of a company’s products or services, which affect the wider economy and society.

One score, many judgments

The most important insight from the document is that an ESG rating is not a single opinion formed from a few headline metrics. EthiFinance says its methodology evaluates companies across four pillars:

- Environment

- Social – Own Workforce

- Social – External Stakeholders

- Governance

These are broken into 15 underlying sustainability topics and supported by 140 indicators, of which 111 are cross-sector, and 29 are sector-specific.

The final score is presented on a 0 to 100 scale, but arriving at it involves several layers of judgment.

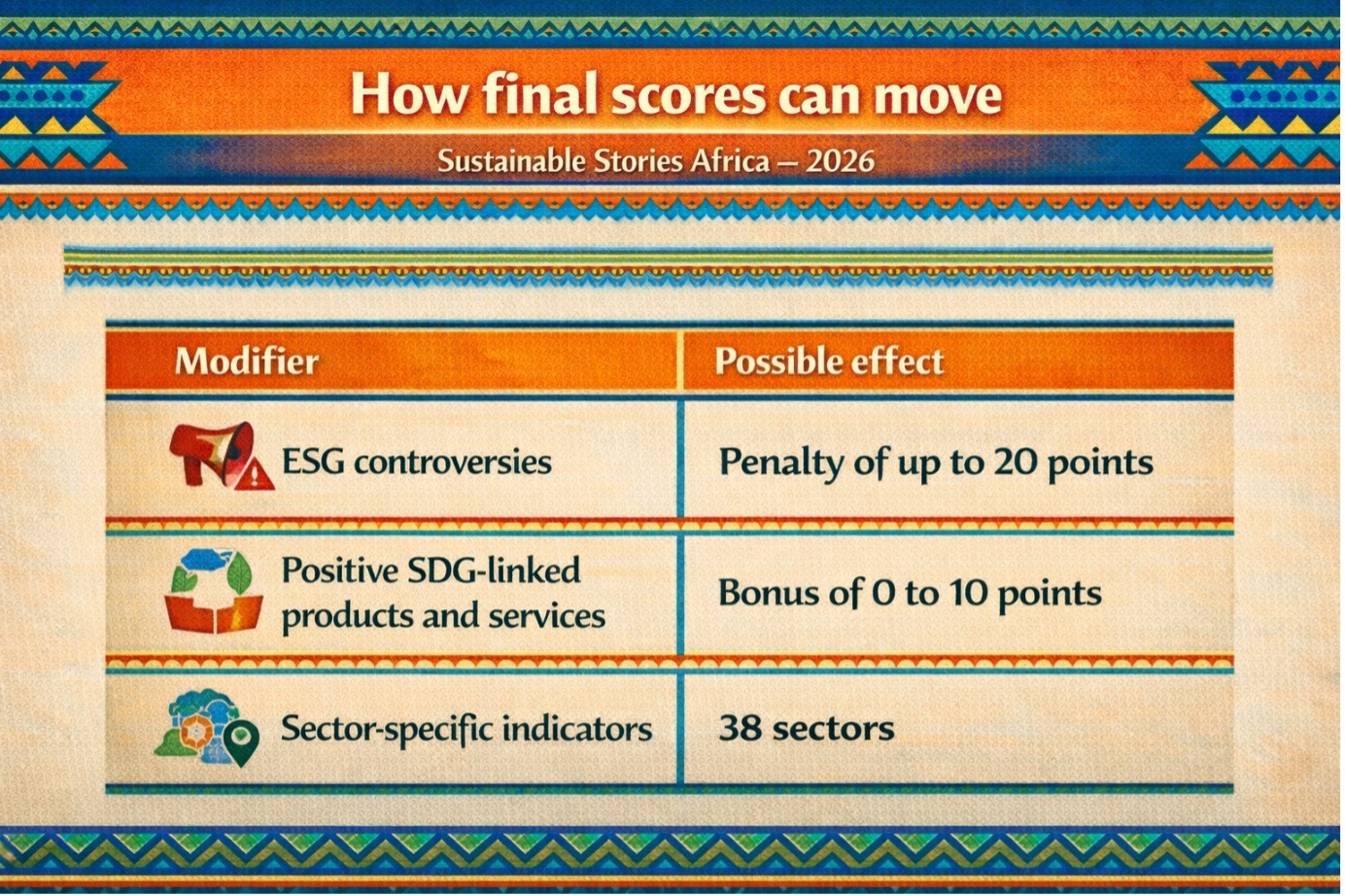

Topics are weighted through a sector-level double materiality analysis. Indicators are scored on transparency, performance and trend over time, and the result can be cut by controversy penalties or lifted by positive-impact bonuses.

That structure matters today because markets still talk about ESG scores as if they are interchangeable. They are not. A score reflects the assumptions of the methodology behind it: what gets measured, how it is weighted, what counts as material, and how misconduct or positive impact changes the result.

The model rewards structure and context

At the heart of EthiFinance’s model is double materiality. The agency says its ratings use sector-level analysis across 38 sectors, combining both impact materiality and financial materiality in line with CSRD-related thinking.

For each of the 15 sustainability topics, it identifies impacts, risks and opportunities, scores both impact and financial materiality, which are then used to assign pillar and topic weights.

This has a significant implication: the same ESG issue does not matter equally across all sectors. Climate, pollution and biodiversity may weigh much more heavily in extractives, utilities or manufacturing than in some services sectors, while governance and workforce practices may carry more weight elsewhere.

Weight ranges are revealing.

- Governance ranges from 30.96% to 59.70%, with a median of 39.39%

- Environment spans 7.24% to 41.30%.

- Social – Own Workforce ranges from 19.25% to 36.89%.

- Social – External Stakeholders, 2.72% to 6.57%

- Aggregated Social, 22.85% to 41.52%.

Together, the ranges show governance is not peripheral in ESG analysis. In many sectors, it sits at the centre.

Indicators mix policies, implementation and outcomes, including waste volumes, training hours, absenteeism, human rights commitments, chair-CEO separation, anti-corruption controls and supplier mapping

What better rating system can unlock

A more granular ESG methodology can reward companies that move beyond public relations into real management systems, measurable performance and strategic alignment.

It also helps distinguish between firms that both publish sustainability reports, but differ sharply in governance quality, operational delivery and controversy exposure.

The product-impact bonus is especially notable. EthiFinance assigns a score between 0 and 10, where products and services contribute positively to the first 16 UN SDGs, linking sustainability value to the business model, rather than only internal controls.

For African firms, that matters. Smaller businesses in renewables, healthcare, circularity, agri-efficiency and digital inclusion may prove sustainability relevance despite limited scale.

This is where methodology becomes strategy. A company may strengthen its rating not only by disclosing more but by improving conduct, reducing controversy risk and proving that its revenue model contributes to real-world solutions.

What companies need to do differently

Missing ESG data is not estimated. EthiFinance treats gaps as weak transparency; as such, silence can reduce a rating, with scores based on reported data updated each year.

For African and other emerging-market issuers, that changes the stakes. ESG disclosure is no longer optional; non-disclosure becomes a measurable weakness rather than a neutral omission.

The controversy framework raises the bar further. ESG events with reputational, legal or financial consequences are assessed for company impact, stakeholder impact and responsibility. Severe or repeated cases attract penalties of up to 20 points.

That means companies must improve disclosure, systems, outcomes and conduct together. Management needs stronger data collection, fewer transparency gaps, three-year tracking, tighter supplier oversight and earlier prevention of controversies.

There is also a size nuance. Using former NFRD thresholds, 500 employees plus either €40 million turnover or €20 million total assets, larger firms must show improvement. In comparison, smaller firms are judged mainly on transparency, with some indicators treated as bonuses.

Path forward – ESG Ratings Shift Toward Real Performance

ESG ratings are moving away from simple disclosure checklists toward systems that mix sector materiality, performance trends, controversy testing and business-model impact.

For African companies, that means the path to better ratings now runs through data quality, governance discipline and credible strategy, not branding alone.

The next step is practical:

- Know your sector weights

- Report consistently

- Manage controversy risk early

- Show how your products create value beyond compliance.

In the new era of ESG ratings, methodology is no longer a background detail. It is the market signal itself.