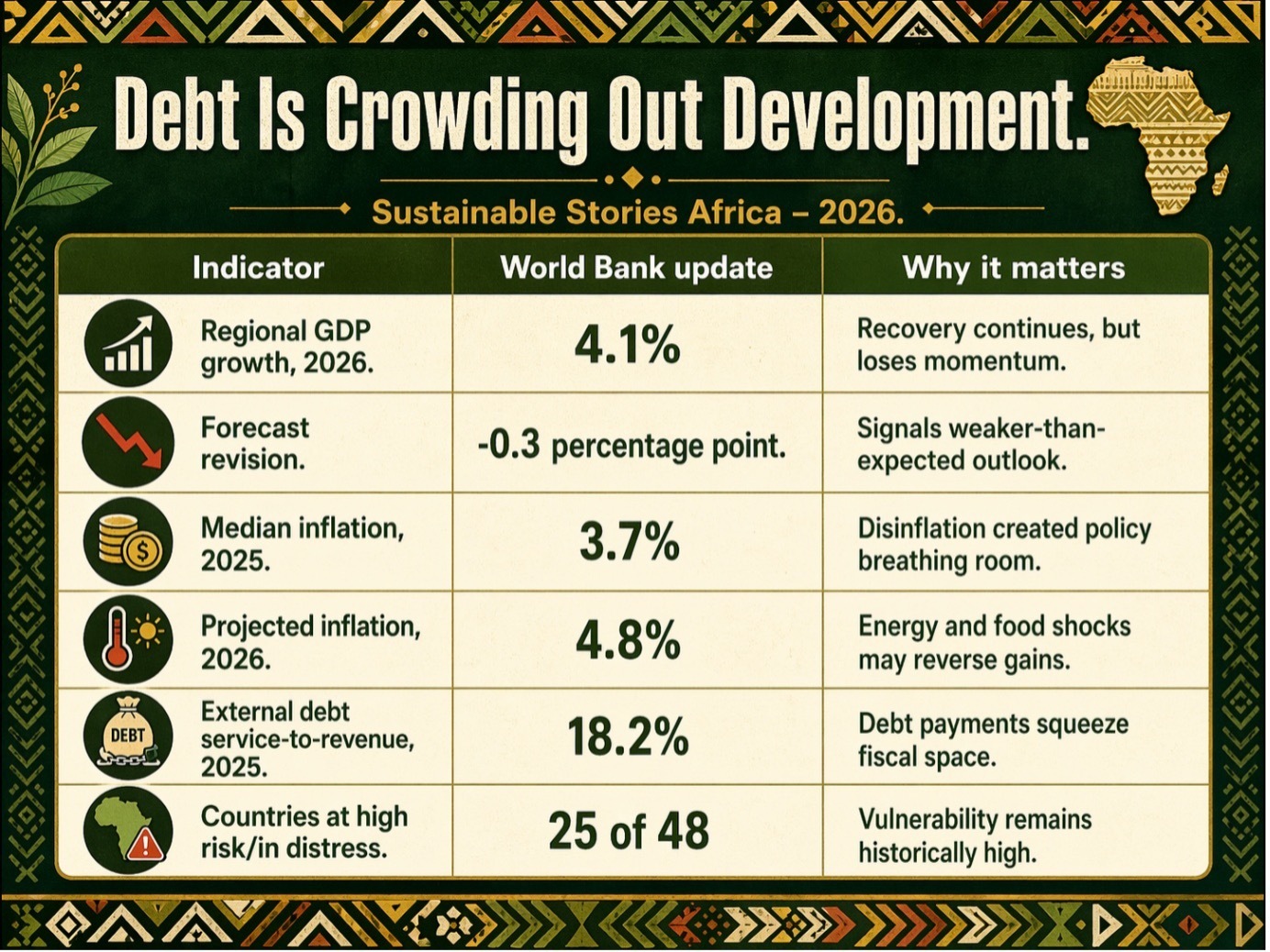

Sub-Saharan Africa’s recovery is still alive, but the World Bank says it is losing force. Growth is projected at 4.1% in 2026, unchanged from 2025 but weaker than previously expected.

The deeper question is no longer whether Africa can rebound from shocks.

It is whether governments can turn growth into jobs, productivity and industrial resilience before debt, inflation and conflict spillovers narrow the policy space further.

Recovery Slows As Risks Rise

Sub-Saharan Africa enters 2026 with a recovery that looks stable on paper but fragile in practice.

The World Bank’s April 2026 Africa Economic Update projects regional growth at 4.1% in 2026, unchanged from 2025, but revised down by 0.3 percentage points from its October 2025 forecast.

That downgrade matters because the region’s challenge is not only growth, but the quality of growth.

Across African markets, households are still managing food and fuel costs, firms are navigating high financing costs, and governments are balancing fiscal consolidation with increasing social needs.

The report’s central message is clear: Africa’s recovery from successive shocks is losing momentum, while its long-term growth model remains constrained by low investment, weak productivity and limited job creation.

The policy answer, the World Bank argues, is not a return to old-style protectionism, but smarter, ecosystem-based industrial policy.

Shocks Are Testing Africa’s Recovery

The strongest warning in the World Bank’s Spring 2026 update is that Africa is now facing overlapping macroeconomic and structural risks.

Geopolitical spillovers from the Middle East, high debt service burdens and deep-seated structural weaknesses are eroding growth prospects and stalling job creation.

The most immediate channel is trade.

The report says the conflict in the Middle East has disrupted energy markets and shipping through the Strait of Hormuz, pushing up Brent crude, liquefied natural gas and fertiliser prices.

That matters for Africa because energy and fertiliser shocks can quickly become food-price shocks, especially in economies where farming seasons depend on imported inputs.

For households, the transmission is painfully familiar: higher fuel costs raise transport costs; higher fertiliser costs raise food production costs; higher food prices reduce purchasing power.

For central banks, the risk is that inflation pressures return just as some countries were beginning to see room for monetary easing.

The report notes that before the shock, inflation was already slowing across much of the region.

Median inflation fell from 4.4% in 2024 to 3.7% in 2025, while about 70% of Sub-Saharan African economies recorded an inflation slowdown in 2025.

However, inflation is projected to rise again to 4.8% in 2026, largely due to the anticipated effects of the conflicts in the Middle East.

Debt Is Crowding Out Development

The debt picture is improving in one sense and worsening in another. Governments are narrowing primary deficits, with the regional primary deficit projected to fall from 0.7% of GDP in 2025 to a balance in 2026.

More than 60% of countries are expected to improve their primary balances between 2024 and 2026.

However, the fiscal story is not only about deficits. It is about interest payments.

The World Bank says net interest costs remain high enough to keep overall deficits elevated, with interest payments exceeding public spending on health or education in four out of five African countries.

External debt service pressure is also rising. Public external debt service-to-revenue is projected to increase from 15.4% in 2024 to about 18.2% in 2025, while principal repayments are expected to jump from $37 billion in 2024 to $59.2 billion in 2025.

Repayments are then projected to remain elevated at between $47 billion and $50 billion annually over 2026 – 28.

Industrial Policy Can Rebuild Momentum

The opportunity in the report lies in its industrial policy argument.

The World Bank is not calling for industrial policy as a slogan. It calls for a disciplined growth strategy that matches policy tools with country capability.

The report says Africa’s medium-term prospects are constrained by chronically low investment rates, with no countries exceeding the 25% of GDP threshold associated with long-term growth.

It also links weak productivity to limited capital deepening, insufficient skills development and slow diffusion of technology into production.

The job challenge gives this debate urgency. More than 620 million people are expected to enter Africa’s labour force by 2050.

Without stronger growth in agribusiness, health, value-added manufacturing, tourism and energy infrastructure, many new workers will continue to enter low-productivity informal jobs.

This is where the sustainability lens becomes practical. An industrial policy that lowers business costs, expands clean and reliable energy, strengthens skills, improves logistics and mobilises private capital can connect ESG priorities to productivity.

It can make climate-aligned infrastructure, local value addition and job creation part of the same development pathway.

Build Ecosystems Before Incentives

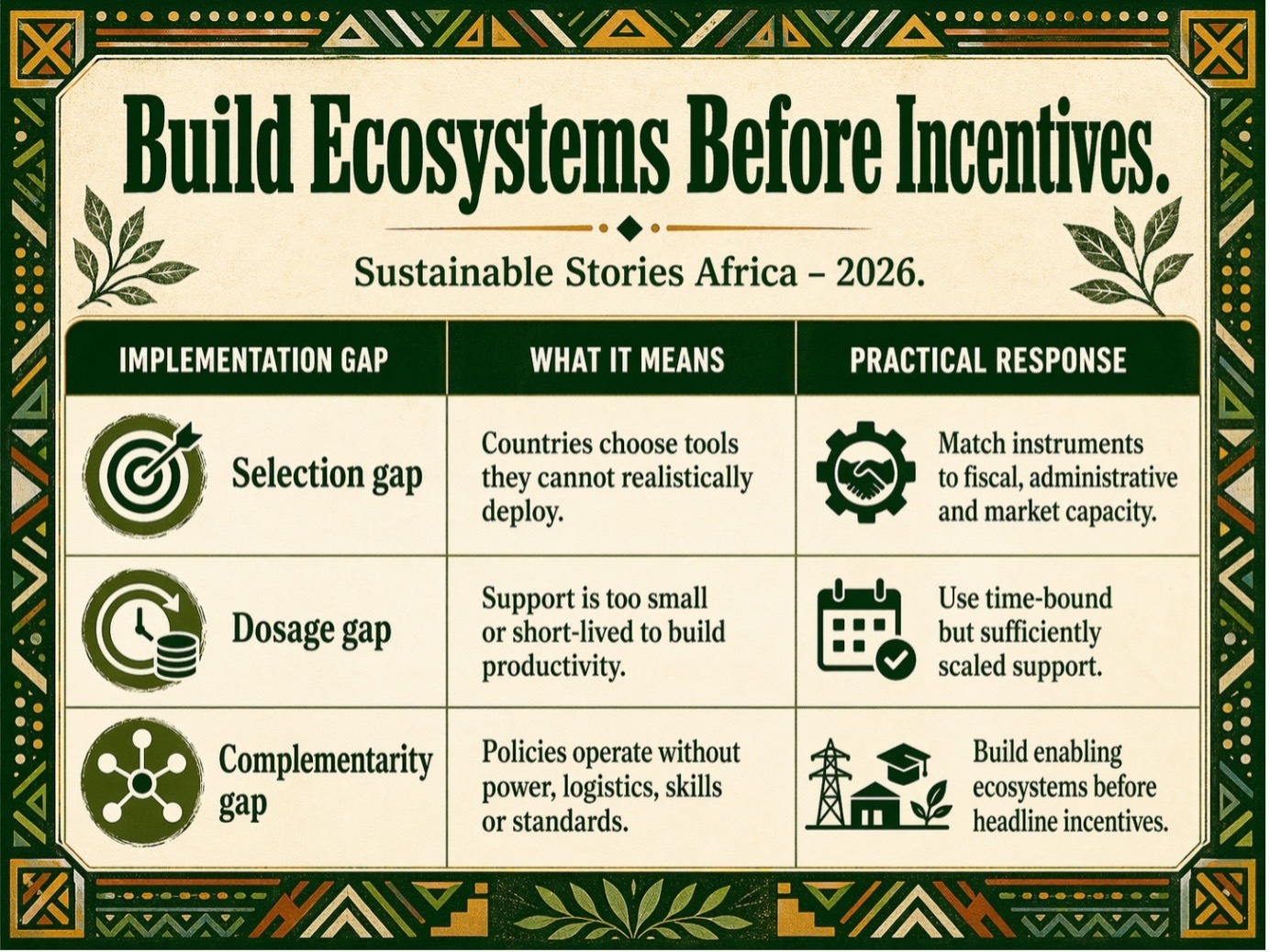

The World Bank’s strongest policy warning is that African industrial policy often fails because ambition is not matched with implementation architecture.

Many national plans identify priority sectors, but fewer link them to financing, responsible agencies, measurable milestones, performance conditions and credible exit rules.

The report identifies three gaps that weaken industrial policy outcomes:

- For governments, the immediate task is to move from announcements to delivery systems. That means strengthening public institutions, improving procurement discipline, building quality infrastructure, supporting export readiness and using regional markets to expand scale.

- For financiers, the report points to the need for long-term capital, especially in infrastructure, industrial parks, renewable energy, logistics and productive small-business ecosystems.

- For regulators, it means designing rules that reward learning, productivity and compliance rather than protecting incumbents indefinitely.

Path Forward – Turn Recovery Into Transformation

Africa’s 2026 growth story is no longer just about rebounding from shocks. It is about converting modest recovery into jobs, productivity and institutional resilience.

The priority is clear: protect vulnerable households from food and fuel shocks, manage debt more transparently, and build industrial ecosystems that can attract investment, raise productivity and support credible ESG-aligned growth across African markets.