A new ESG handbook backed by the AIRE Centre, Sustineri Partners and UNDP argues that sustainable business is no longer just about reputation.

It is becoming a practical framework for managing risk, attracting capital and staying relevant as regulation, investor pressure, and consumer expectations converge.

For African and other emerging markets, the lesson is immediate.

Businesses that still treat ESG as public relations may soon discover that reporting, supply chains, trade access and financing are being reshaped by harder market rules.

Sustainability Is Becoming Core Business

The handbook Building a Sustainable Future: ESG Business Handbook presents ESG as a business operating model rather than a side initiative.

Produced for businesses in Bosnia and Herzegovina, it is designed as a practical guide for implementing environmental, social and governance standards, assessing performance, defining action plans and linking business strategy with the Sustainable Development Goals

Its broader significance, however, reaches beyond the Western Balkans. The document captures a global shift many African firms are now facing: companies are increasingly expected not only to perform well but to “do good” and “do no harm.”

That shift matters because the pressures are no longer abstract. Investors, consumers, regulators and supply-chain partners are all asking tougher questions about carbon exposure, labour practices, governance quality and transparency.

The handbook notes that ESG factors can no longer be treated as a “nice to have.” In some markets, they are already mandatory, while in others, they are rapidly becoming a precondition for financing, contracts and market access.

For African businesses, especially exporters, manufacturers, banks and mid-sized firms plugged into global value chains, that message comes with particular force.

The practical question is no longer whether ESG matters. It is about whether companies can build the systems, data and governance needed to respond before outside pressure turns into a lost opportunity.

Capital Is Following ESG Signals

The handbook’s strongest hook is financial. It says that more than 80% of investors review a company’s ESG standards when considering potential investments.

It also cites research showing that global ESG assets rose from $35 trillion in 2020 to $41 trillion in 2022 and may have exceeded $50 trillion by 2025, potentially accounting for more than one-third of global assets.

Another statistic is equally telling: 54% of investors believe better ESG practices lead to stronger returns over time.

This is why the handbook frames ESG less as philanthropy than as market infrastructure. Companies that integrate it well are more likely to identify and mitigate environmental, social and governance risks, respond to stakeholder expectations and innovate faster.

Those that lag may find themselves locked out of cheaper finance, premium customers and more resilient partnerships.

That logic is becoming familiar in Africa, too. Sustainability disclosure, transition finance, labelled debt, and supply-chain due diligence are no longer purely European internal matters.

They increasingly shape which companies are considered investable, bankable and export-ready.

The Rules Are Getting Harder

The handbook shows how ESG has evolved from voluntary corporate social responsibility into a more regulated and measurable framework.

Unlike older CSR reporting, often centred on broad goodwill activity, ESG is built around defined goals, metrics and outcomes that are harder to manipulate or greenwash.

Europe is driving much of that shift. The CSRD requires large companies, including certain non-EU firms, to disclose ESG information annually. The Corporate Sustainability Due Diligence framework pushes companies to address harms across their operations and value chains.

CBAM entered its transition phase on October 1, 2023, ahead of payment adjustments in 2026.

The handbook also highlights the ISSB, created in 2021, as part of the push for global disclosure standards. For emerging markets, the warning is clear: even SMEs outside the formal scope may still feel pressure through supply chains, financiers and customers.

It also links ESG to the SDGs, arguing that the goals define the destination while ESG provides the method. Research cited estimates $12 trillion in opportunities by 2030, 380 million new jobs, and says 78% of customers favour SDG-aligned companies today.

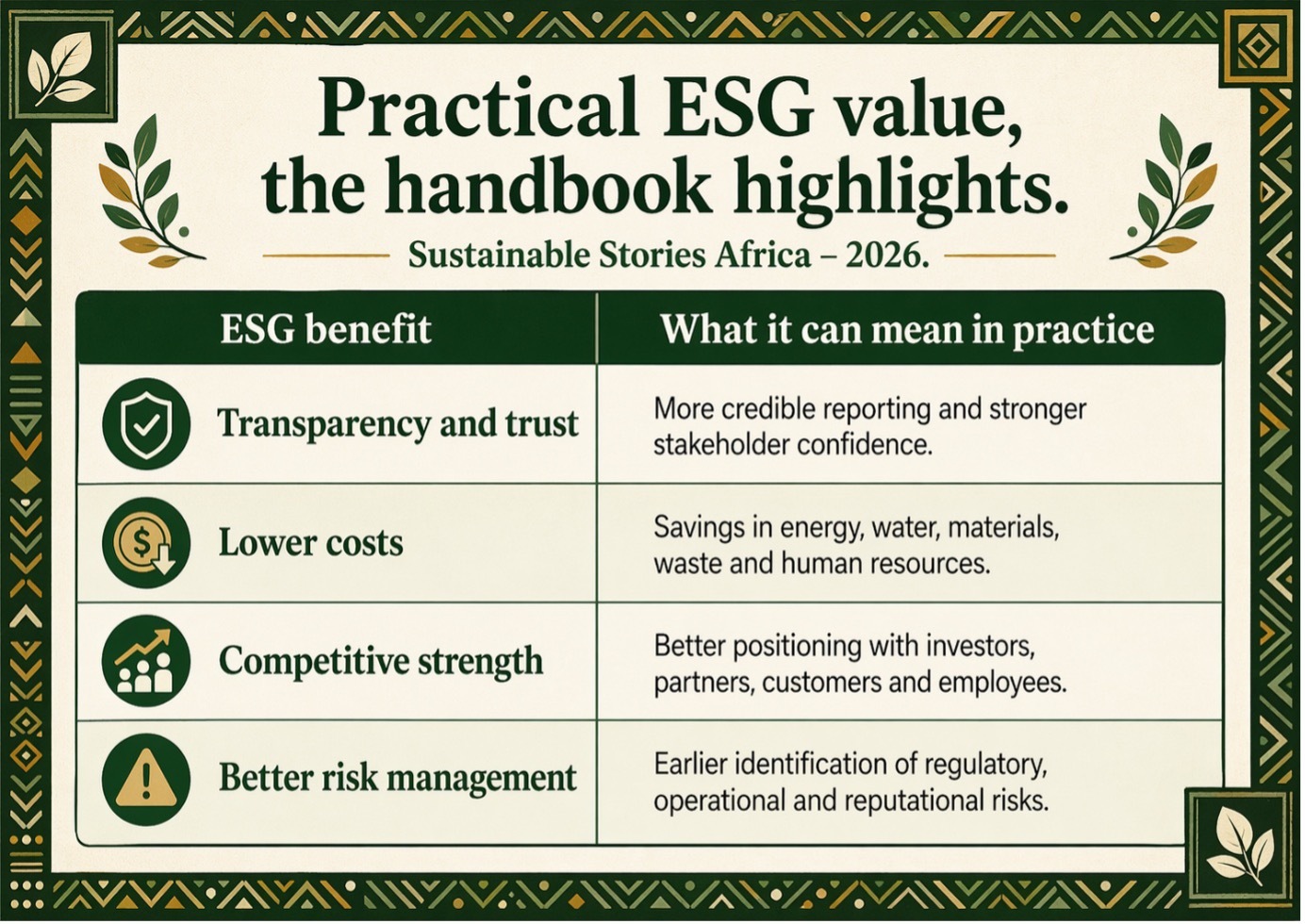

What Good ESG Can Unlock

The document is at its most persuasive when it moves from theory to business outcomes. It says a strong ESG programme can improve transparency and trust, reduce costs, strengthen competitive advantage and improve risk management.

Better disclosure can build credibility with investors, customers, employees and partners; operational changes can reduce costs related to energy, water, materials and waste; and a more structured approach to sustainability can help firms identify both vulnerabilities and untapped opportunities.

The case studies help ground that argument. Kakanj Cement, one of the handbook’s featured companies, is presented as proof that even a carbon-intensive industry can meaningfully move on to ESG.

The company won UNDP SDG Business Pioneer awards, built its reporting systems over the years, and had already been reporting to required standards since 2003, leaving it better prepared for CBAM-era disclosure.

The handbook also notes that its dust emissions are now below 10 mg/m3, compared with a European limit of 30 mg/m3, and that it has held ISO 14001 environmental certification since December 2003.

It links that progress to data discipline, training, community dialogue, biodiversity measures and gender representation in leadership.

That is useful for African readers because it shows that ESG progress does not begin with perfect regulation.

It often begins with management systems, training, reporting routines and a decision to treat transparency as a strategic asset.

Start With Materiality, Then Move

The handbook argues that an effective ESG strategy begins with materiality.

Companies must identify the issues most relevant to their operations and stakeholders, gather internal and external input, prioritise them, align them with their business strategy and report progress over time.

Practical steps include conducting gap analyses, setting ESG goals and indicators, identifying risks and opportunities, and building reporting systems that support annual disclosure.

Its broader message is that ESG does not require perfection from the outset. What matters is starting with what is material, measuring it, governing it and improving over time.

For African firms, this means understanding where investor expectations, trade rules and reporting standards are heading.

Increasingly, ESG readiness is becoming a signal of management quality, rewarding companies that can track risk, performance and disclosure more credibly.

Path Forward – Build Systems Before Pressure Peaks

The handbook is effectively advocating an early-mover strategy.

Companies should strengthen materiality assessment, governance, reporting and target-setting before regulatory and market pressure further increase.

ESG should be treated as a management discipline tied to strategy, capital and resilience, not as a communications exercise.

For African businesses, the immediate task is to localise that lesson: understand the standards shaping export markets, investor behaviour and supply chains, then build internal systems that can respond with evidence.