Fashion’s climate challenge is no longer only about greener fabrics or conscious consumers. Aii and Fashion for Good estimate that decarbonising the apparel supply chain will require about $1.04 trillion in investment.

The opportunity is vast, but the risk is uneven. For African and emerging-market manufacturers, the question is whether climate finance will reach factories, workers and suppliers before global rules reshape competitiveness.

Fashion’s Climate Bill Comes Due

The global fashion industry now faces a financing test as large as its climate footprint. A report by the Apparel Impact Institute and Fashion for Good estimates that the sector needs $1.04 trillion to fund the existing and innovative solutions required to put fashion on a net-zero pathway by 2050.

The report places fashion’s annual greenhouse gas emissions at about 1.025 gigatonnes of CO₂ equivalent, approximately 2% of global emissions, with the heaviest impacts concentrated in raw materials and processing.

It also identifies a combined emissions-reduction potential of 2.5 gigatonnes of CO₂ equivalent across solution categories.

For African and other emerging markets, the story is bigger than fashion.

It is about whether suppliers in lower-margin production economies can access the capital needed to decarbonise before procurement standards, carbon disclosure rules, and green trade preferences harden into new barriers.

Fashion Meets Its Finance Moment

A trillion-dollar figure can sound abstract until it is traced back to a textile mill, a dyeing facility, a cotton field or a rooftop without solar panels. That is where fashion’s climate transition will succeed or fail.

The report’s central message is blunt: the industry cannot reach net zero through brand pledges alone.

The largest share of emissions lies deep within supply chains, especially in Scope 3, where brands depend on independent manufacturers, raw-material producers, processors and logistics networks.

Among fashion brands with approved science-based targets, the report notes that 96% of emissions come from Scope 3, with upstream activities accounting for most of that burden.

That matters for Africa because the continent is a source of raw materials and a potential frontier for manufacturing growth. Cotton, leather, textiles, logistics, renewable energy and industrial policy all sit within the opportunity.

However, unless finance moves beyond headquarters and reaches production assets, suppliers may be asked to carry the climate transition without the balance-sheet strength to pay for it.

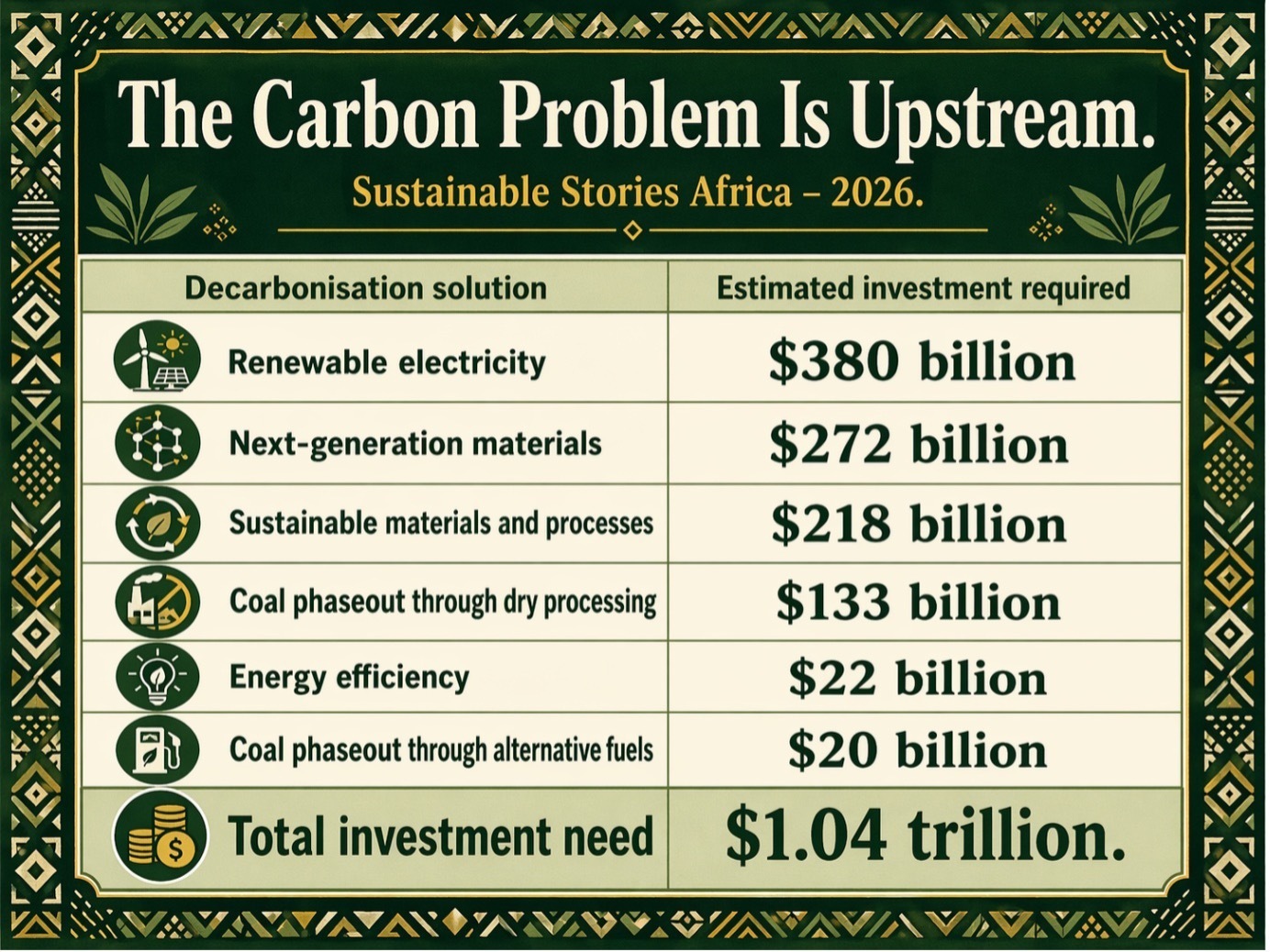

The Carbon Problem Is Upstream

The report divides fashion’s supply chain into tiers and shows why decarbonisation must move beyond retail stores and corporate offices.

- Tier 2 material production, including fabric production and finishing, accounts for 52% of emissions.

- Tier 4 raw material extraction accounts for 24%.

- Tier 3 raw material processing contributes 15%.

- Tier 1 finished product assembly contributes 9%.

This is the practical challenge for ESG governance: the easiest emissions to report are not always the most important emissions to reduce.

Scope 1 and 2 emissions are under more direct brand control, but the bigger carbon story sits in supplier facilities, thermal energy systems, wet processing, fibre choices and material efficiency.

The largest financing need is renewable electricity, at $380 billion.

The report says switching production to renewable electricity across the fashion supply chain could abate about 27% of all emissions.

Sustainable materials and processes require $218 billion, while next-generation materials, including textile recycling, bio-based materials and plant-based alternatives, require $272 billion.

The most immediate win may be energy efficiency.

The report describes it as a “low-hanging fruit” because it can cut energy use, lower operating costs, and deliver attractive returns.

Programmes such as Clean by Design have delivered average reductions of 10% to 20% in energy, water and chemical use, showing how practical upgrades can produce both climate and cost benefits.

Cleaner Factories Can Create Value

The prize is not only emissions reduction. It is industrial competitiveness.

For emerging-market manufacturers, decarbonisation can mean lower energy bills, improved buyer relationships, better access to international markets and greater resilience against future regulation.

A factory that invests in solar, energy-efficient boilers, heat recovery, compressed-air optimisation, or wastewater reuse is not merely “going green”. It is reducing operating volatility.

The report’s financing map shows why this transition must be shared.

- Bank debt, bonds and loan funds are expected to provide the largest share of capital, at $528 billion.

- Venture capital and private equity are expected to provide $181 billion,

- Sustainability premiums $149 billion

- Brands and manufacturers $134 billion

- Governments, development banks and philanthropy $50 billion.

This distribution matters because manufacturers cannot reasonably absorb the full cost of a transition demanded by brands, regulators and consumers.

The report quotes Punit Lalbhai, Executive Director of Arvind Limited, as saying that where energy use or manufacturing methods must change completely, “the manufacturer cannot take on the entire cost burden and project risk.”

That insight is particularly relevant for African supply chains, where smaller manufacturers often face high borrowing costs, currency risk, weak collateral positions and limited access to long-term capital.

If climate finance is structured only for large, creditworthy companies, the transition will deepen inequality inside the supply chain.

Finance Must Reach Real Factories

The report identifies nine barriers that are responsible for the financing gap.

- Industry fragmentation

- Weak pricing of environmental externalities

- Limited investor awareness

- Poor creditworthiness of production facilities

- Difficulty deploying capital into emerging markets

- Small project sizes.

- Weak innovation track records

- Long capital-intensive innovation cycles

- Misaligned incentives between brands and suppliers.

For African markets, three barriers stand out.

- First, manufacturers often lack long-term order visibility. Banks hesitate to finance multi-year projects because suppliers cannot prove that buyer volumes will continue beyond 12 months.

- Second, emerging-market finance faces approval delays, policy uncertainty and currency risk.

- Third, many projects are too small for institutional investors unless aggregated through platforms, funds or pooled procurement structures.

The required actions are therefore institutional, not cosmetic.

- Governments can provide loan guarantees, green banks, tax credits, feed-in tariffs and policy frameworks that reward low-carbon production.

- Philanthropy can use catalytic capital to de-risk early-stage projects.

- Manufacturers need capital improvement plans that rank projects by both emissions’ reduction and financial return.

- Brands must offer volume guarantees, co-investment, supplier support and clearer long-term demand signals.

- Banks and development finance institutions also have a direct role. They can fund local banks in local currency, aggregate small projects, prioritise underserved production regions and design transition-finance products for coal phaseout, renewable electricity and efficiency upgrades.

Path Forward – Make Climate Finance Reach Suppliers

Fashion’s trillion-dollar transition will be judged by whether capital reaches the mills, farms, dye houses and factories where emissions are produced.

African markets should position textile, cotton, leather and renewable-energy strategies around supplier decarbonisation, not only export promotion.

The priority is practical: blend public, private and philanthropic finance; protect manufacturers from unfair cost transfer; and link ESG compliance to bankable industrial upgrading.

That is how fashion’s climate bill becomes a development opportunity.