IFRS S2 is pushing climate disclosure beyond ambition statements and into strategy. The standard asks whether a company’s business model can remain viable as climate risks and opportunities reshape markets, assets and operations.

For African and emerging-market companies, that makes climate resilience a finance question, not just a sustainability one.

The shift matters because investors increasingly want evidence of preparedness, adaptation capacity and long-term business durability.

Climate Resilience Moves Into Finance

Climate disclosure is entering a more demanding phase. Under IFRS S2, companies are expected to explain not only what climate risks they face, but also how resilient their strategy and business model are under changing climate conditions.

The emphasis is on climate scenario analysis and climate resilience: two linked ideas that turn uncertainty into a test of governance, capital allocation and long-term viability.

That matters in African markets, where climate shocks are already colliding with growth ambitions, infrastructure gaps and tighter global capital standards.

A drought, flood, heat event or carbon-related policy shift can affect supply chains, energy costs, insurance, export access and asset values.

IFRS S2 effectively asks companies to show they understand that reality before investors price the risk for them.

The message from the explainer is clear: climate resilience is no longer an optional narrative tucked into a sustainability brochure.

It is part of financial risk transparency; it is increasingly central to how investors judge whether a business can endure, adapt and compete.

Climate Risk Becomes Financial Fact

The most important shift in IFRS S2 is conceptual but powerful. Climate-related risks and opportunities are treated as financial considerations, rather than peripheral environmental issues.

The explainer says investors need decision-useful information on how organisations are preparing because climate risks are complex, uncertain and capable of affecting business performance.

That framing changes the conversation in boardrooms. The key question on page 3 is blunt: Can your business model remain viable in a changing climate? That is a much harder test than asking whether a company has an emissions target or a sustainability policy.

It forces directors and executives to examine whether strategy, operations, and/or capital planning still hold under physical climate shocks, transition pressures and shifting market expectations.

For banks, manufacturers, food processors, telecoms operators and infrastructure firms across Africa, the relevance is immediate.

A company exposed to rising cooling costs, water stress, grid instability, fuel price volatility or export-market decarbonization rules cannot rely on backwards-looking reporting.

IFRS S2 pushes firms to look ahead and explain how they would absorb pressure, adapt operations and preserve value.

Scenario Analysis Tests Strategic Reality

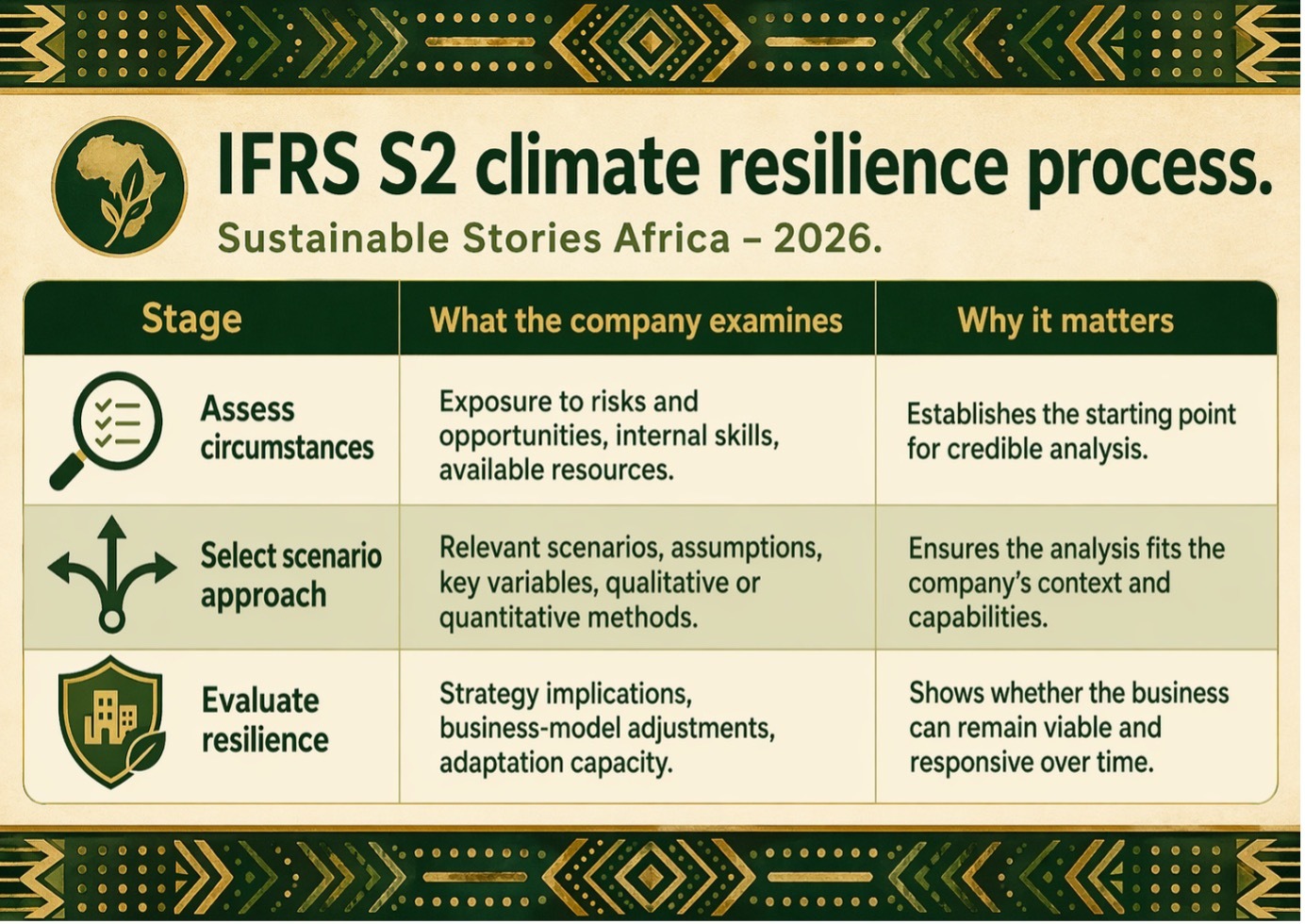

The explainer defines climate resilience as a company’s ability to manage climate-related risks and opportunities across strategy and operations.

Under IFRS S2, that means not only responding to physical and transition risks, but also adapting business models, capturing opportunities and adjusting decisions across the short, medium and long term.

In this framing, resilience is not a static disclosure concept. It is a test of whether a business can remain viable and responsive under climate pressure.

Scenario analysis is the tool that turns that assessment into practice.

On page 4, the explainer describes it as a process that identifies and assesses a range of possible future outcomes.

Companies use it to examine how climate risks could affect strategy, where financial exposure sits, how severe physical disruption may become and what adaptation will be required.

The document outlines a three-stage process: assess the company’s circumstances, analyse relevant scenarios and variables, then adapt strategy, business models and operations.

That makes the standard especially relevant for African and Global South firms already facing heat, flooding, logistics disruption, currency pressure and rising energy costs.

Scenario analysis translates those lived stresses into structured disclosure, showing how manufacturers, agribusinesses and banks may be exposed and where resilience measures are most urgently needed in the coming planning cycles ahead.

Better Disclosure Can Unlock Trust

The value of IFRS S2 is not simply compliance.

Better climate resilience disclosure can improve the preparedness of investors, lenders, and boards of directors. The document says companies must disclose the results of their resilience assessment, the implications for strategy and business model, significant uncertainties considered, key assumptions and inputs used, and their capacity to adapt over time.

They must also explain how the scenario analysis was conducted, when it was performed, and the reporting period considered.

That transparency can unlock more than better reporting. It can strengthen strategic discipline. A company that knows which assumptions underpin its resilience is better placed to redesign supply chains, protect assets, diversify energy sources or revise capital expenditure. It can also communicate more credibly with investors who increasingly want comparable, decision-useful disclosure instead of generic climate language.

For African markets, this matters because stronger disclosure can narrow the trust gap that often raises the cost of capital.

Businesses that can show a clear line between climate risk, operational response and financial resilience are likely to appear better governed than their peers, despite their reporting in vague terms.

Boards Must Move Beyond Narrative

The explainer also carries a practical warning. Climate resilience is typically assessed annually, scenario analysis evolves as circumstances change, and companies should update their analysis with strategic planning cycles

It adds that the approach should be proportionate to company capabilities and that scenario analysis may not require annual updates, even though resilience must be reassessed as business conditions evolve.

That means companies do not need to wait for perfect models or vast technical teams before starting. They do, however, need governance discipline.

- Boards should treat climate resilience as a recurring strategic exercise tied to planning, risk management and disclosure controls.

- Finance teams, sustainability teams and operations leaders need to work from the same assumptions.

- Regulators and standard-setters, meanwhile, should help local markets build capacity so that IFRS S2 adoption does not become a box-ticking exercise that excludes smaller issuers or weaker institutions.

The deeper shift is cultural. IFRS S2 compelling companies to prove that climate thinking is embedded in how they run the business, not just in how they write the report.

Path Forward – Resilience Must Become Routine

African companies now need to move from broad climate narratives to structured resilience assessments tied to strategy, operations and investor disclosure.

The priority is to build proportionate scenario analysis that reflects real exposures and real adaptation options.

What is being advocated is straightforward: assess, analyse, and adapt consistently.

When done well, IFRS S2 can help markets price climate risk more clearly, reward stronger governance and push ESG reporting closer to the operational realities businesses already face.