Carbon capture, utilisation and storage are attracting more money, more projects and wider geographic interest than ever before.

However, the International Energy Agency says the real bottleneck is no longer whether CCUS matters for decarbonisation.

It is whether projects can become bankable enough to attract private capital at scale.

That question matters for African and other emerging markets because public finance alone will not be enough.

Without viable business models, clearer regulation and better risk-sharing, CCUS may remain concentrated in a handful of advanced jurisdictions.

Carbon Finance Meets Climate Reality

The latest IEA report on Financing CCUS at Scale comes at a critical moment for climate and industrial policy. Investment is rising, projects are multiplying, and governments are committing record levels of support.

However, the agency’s central message is sobering: CCUS will not scale on momentum alone. It needs financing structures that can absorb new kinds of risk, reward long-term performance and give lenders confidence across the full capture, transport and storage chain.

That challenge is especially relevant for emerging economies. Many of them have hard-to-abate industries, growing energy demand and, in some cases, geological storage potential or depleted oil and gas fields that could support permanent CO2 storage.

However, they often lack the policy certainty, development funding and project-preparation capacity needed to crowd in commercial capital early.

The IEA notes that emerging and developing economies account for roughly two-thirds of cumulative CO2 captured to 2050 in its Net Zero Emissions scenario, making their participation essential rather than optional.

The result is a familiar development tension: the climate case for deployment is strengthening, but the financing case still needs work.

More Projects, Bigger Funding Gap

The numbers are striking.

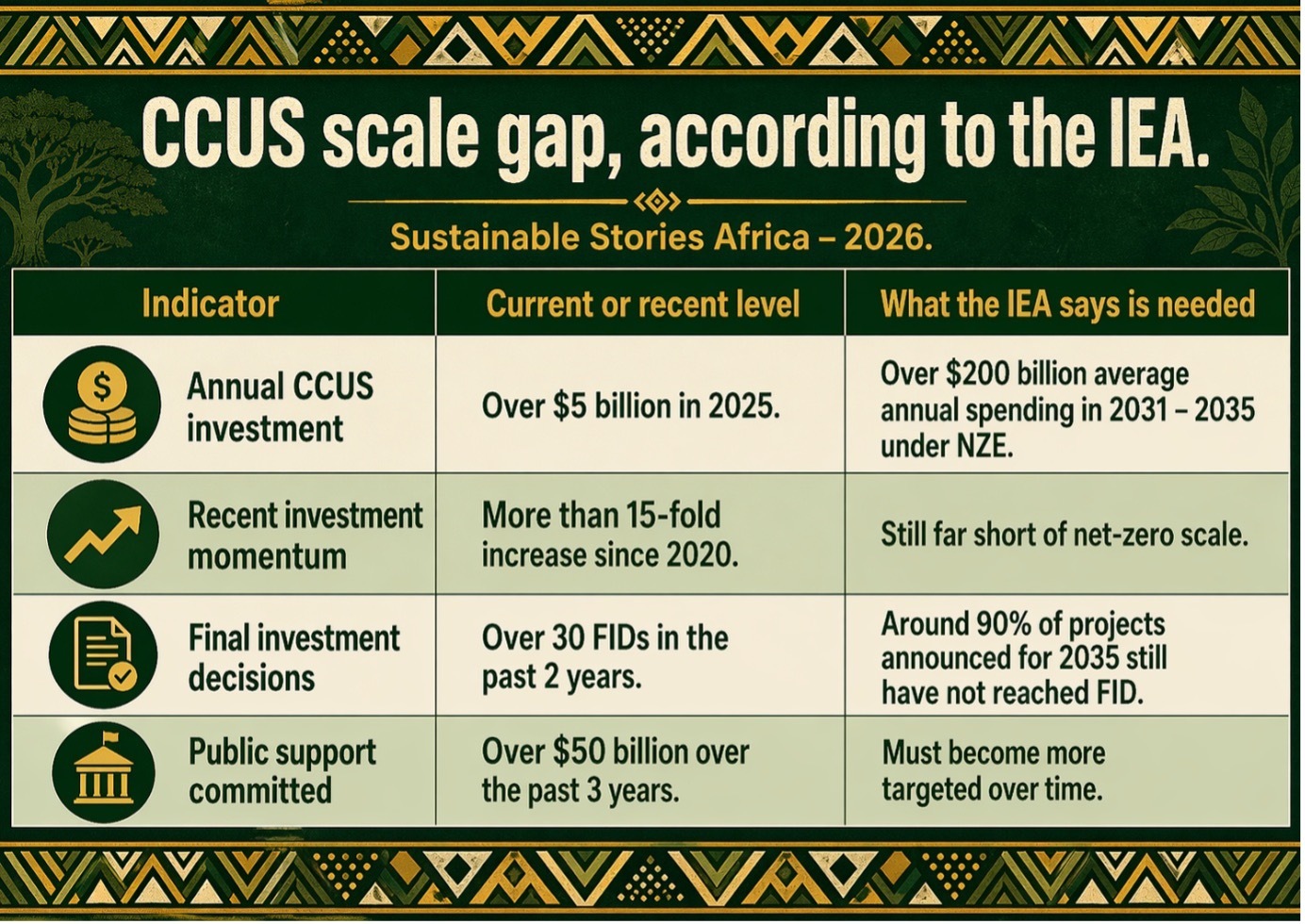

The IEA says more than 30 final investment decisions have been agreed in the past two years, with activity, especially visible in Europe and North America, across transport and storage, industry and power.

Global annual investment has increased more than 15-fold since 2020, reaching over $5 billion in 2025. Public support has also surged, with governments earmarking more than $50 billion for CCUS projects over the past three years.

However, the scale gap remains enormous. The report says average annual CCUS spending would need to rise to more than $200 billion between 2031 and 2035 in the IEA’s Net Zero Emissions pathway.

Operational capture capacity, currently between 50 and 60 million tonnes per year, is still far below what would be needed for a net-zero-compatible buildout.

By 2035, the agency’s net-zero scenario envisages 2.3 gigatonnes of capture capacity, rising to 6.1 gigatonnes by 2050.

The contradiction is the story: interest is real, but bankability remains fragile.

CCUS Needs Revenue, Not Just Engineering

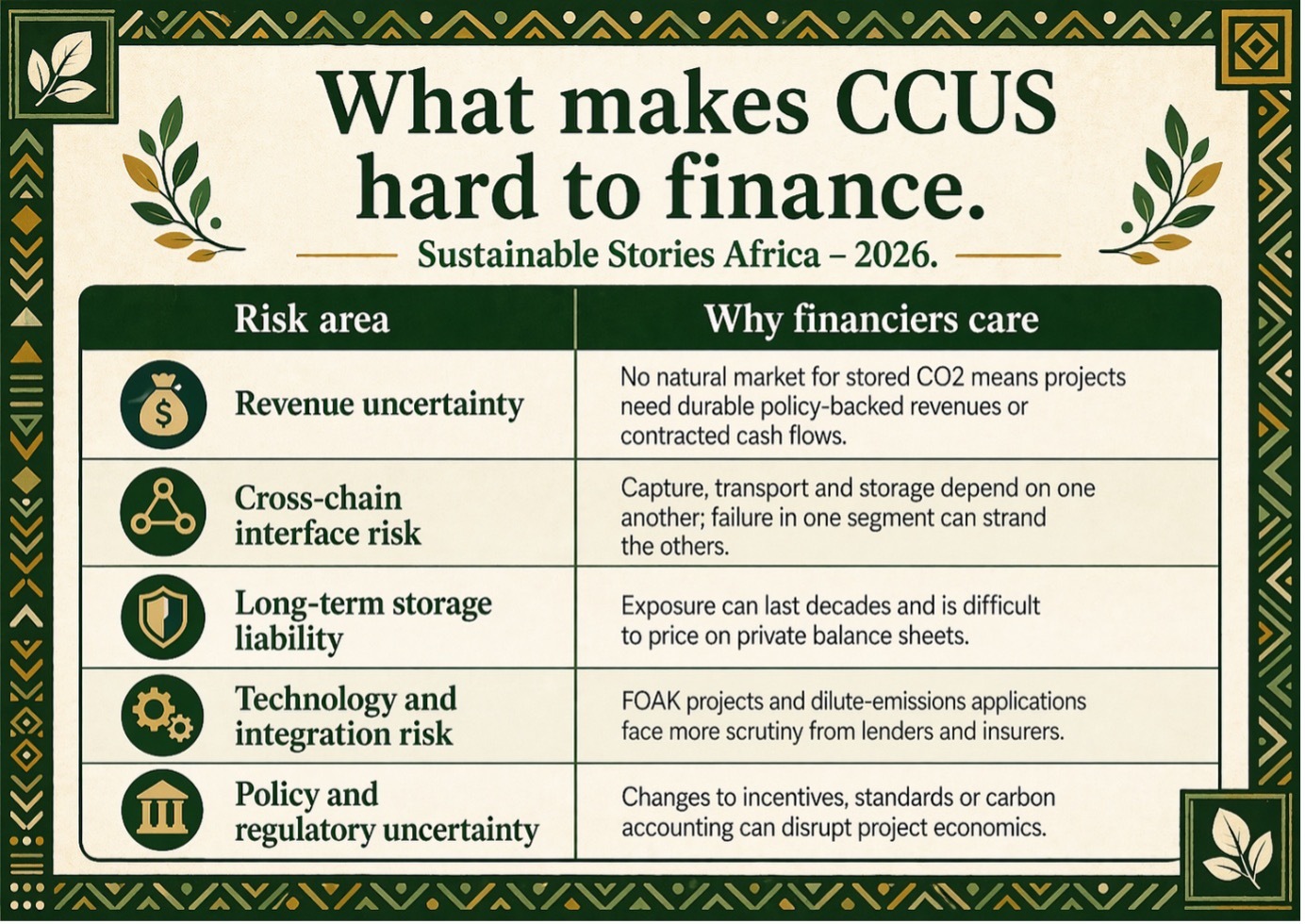

The International Energy Agency’s central insight is that CCUS does not behave like most clean energy technologies. Unlike solar, wind or batteries, it does not create a widely traded product with a natural revenue stream. Stored has little intrinsic market value.

That makes commercial viability, rather than technical possibility, the core challenge. The IEA says the sector is moving away from enhanced oil recovery towards dedicated storage in saline aquifers and depleted oil and gas fields, where no equivalent market exists.

As a result, dedicated storage could rise from approximately 20% of operating storage capacity today to more than 90% by 2035. That shift increases dependence on policy incentives, low-emissions product premiums, carbon removal credits and longer-term public support.

The financing logic is changing. CCUS now needs new business models, capital sources and clearer risk allocation across capture, transport and storage. If capture volumes fall, transport assets may be underused; if storage liability remains unclear, lenders may raise borrowing costs or stay away.

The report’s risk map highlights revenue uncertainty, policy uncertainty, long-term storage liability and coordination problems. More than $15 billion in commercial debt has been raised in the past two years, mainly in Europe and North America, but infrastructure funds, pension funds and insurers remain selective.

What Better Financing Could Unlock

If current constraints are addressed, the International Energy Agency says CCUS could play an important role in cutting emissions from hard-to-abate sectors such as cement, steel, chemicals, hydrogen and some power applications, where alternatives remain costly or limited.

It could also support carbon removals through BECCS and direct air capture with storage, while opening transition pathways for countries with suitable geology and legacy oil and gas expertise.

For emerging markets, the opportunity extends beyond emissions reduction to new industrial value chains, stronger export competitiveness and expanded roles for development finance institutions.

This is especially relevant for Africa. The IEA explicitly recommends increased development funding to align storage potential for , arguing that weak geological data remains a major barrier.

Without bankable storage assessments, project pipelines are unlikely to become financeable at scale.

Seven Shifts That Must Happen

The IEA’s recommendations are practical and policy-heavy.

- Governments, it says, must support bankable business models through stable carbon pricing, targeted tools such as contracts for difference or tax credits, and risk-sharing frameworks that address liabilities private markets cannot absorb alone.

- Legal and regulatory frameworks must become clearer and more durable, particularly around third-party access, carbon accounting and long-term storage liability.

- The agency also calls for harmonised definitions and standards, improved data-sharing and early collaboration among developers, financiers and insurers, more development funding for storage assessment, and recognition of CCUS within sustainable finance taxonomies and transition finance frameworks.

- That last point is particularly important because it could widen access to green and sustainability-linked bonds and broaden the investor base over time.

- The message to African policymakers and financiers is therefore quite specific: do not treat CCUS as a single technology question.

- Treat it as a system question involving geology, regulation, public finance, industrial policy and investor confidence.

Path Forward – Build Bankability First

The IEA is effectively arguing for a sequencing strategy: first, make CCUS projects bankable, then expect private capital to scale them.

That means stronger policy certainty, better risk allocation, storage-resource development and finance rules that recognise transition technologies where they are credible and durable.

For African markets, the opportunity lies not in copying mature markets line for line, but in building the enabling conditions early.

If that foundation is missing, CCUS will remain a global talking point. If it is built well, it could become part of a broader industrial decarbonisation strategy.