The clean-energy transition is creating a new industrial question: what happens when millions of electric vehicle batteries reach the end of their first life?

A new European Patent Office and International Energy Agency study shows battery circularity is no longer a waste issue alone. It is becoming a race for patents, supply security, emissions reduction and strategic advantage — with major implications for Africa.

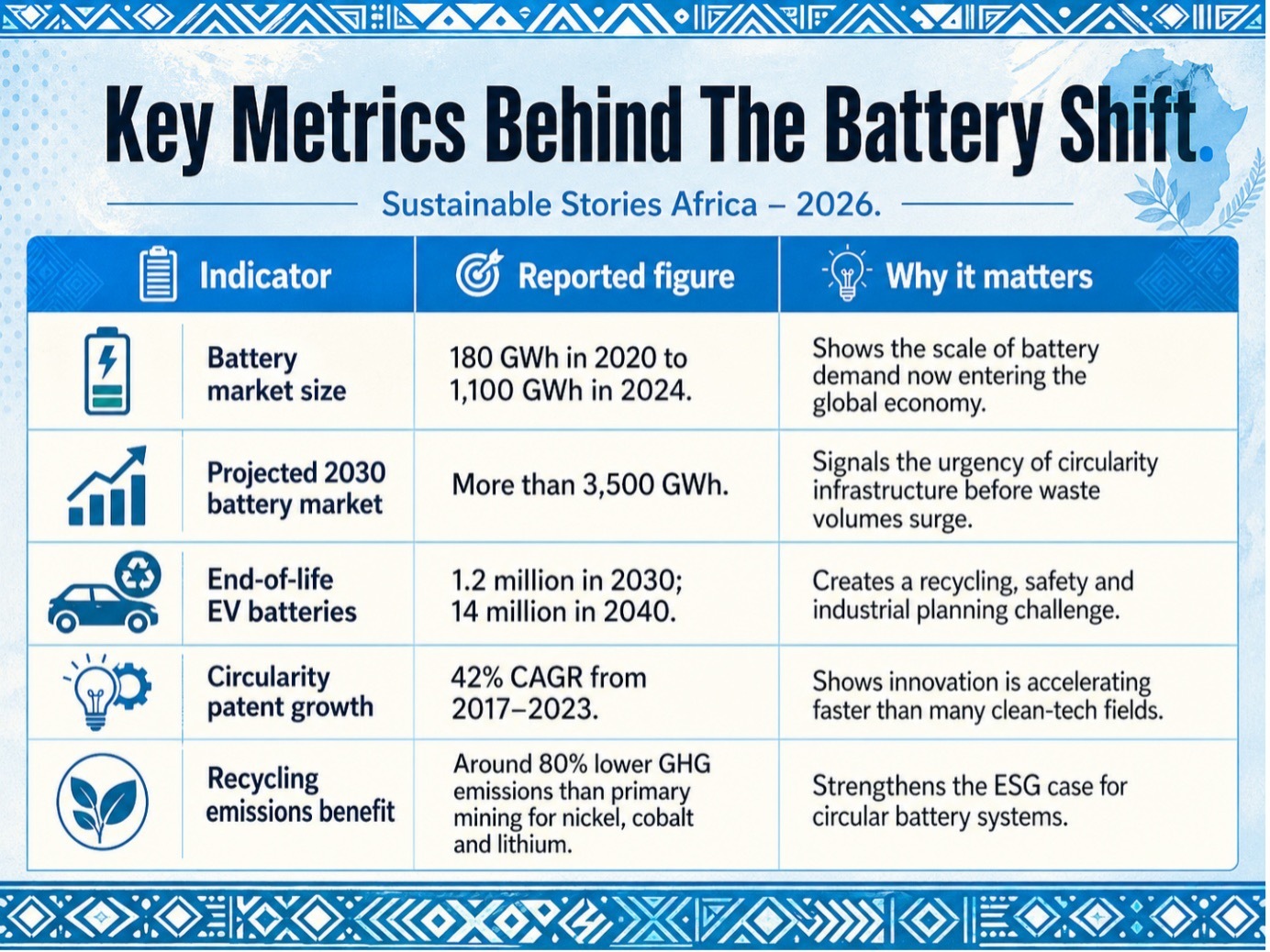

Battery Waste Becomes A Strategic Resource

A fast-growing battery economy is forcing governments, manufacturers and investors to rethink one of the least glamorous parts of the energy transition: waste.

The latest EPO-IEA study on battery circularity shows that lithium-ion batteries are moving from an innovation story about electric vehicles to a governance story about minerals, recycling, patents and industrial resilience.

The numbers are stark. The market for lithium-ion and other modern batteries rose from about 180 GWh in 2020 to 1,100 GWh in 2024 and is projected to exceed 3,500 GWh by 2030.

By then, around 1.2 million EV batteries could reach the end of life globally, rising to 14 million by 2040 and 50 million by 2050.

For Africa, the issue is immediate. The continent is already central to critical minerals opportunities, including cobalt, graphite, manganese and lithium.

However, the next competitive edge may not only come from extraction. It may come from collection systems, recycling standards, battery diagnostics, regional processing and a circular economy that keeps more value within African markets.

A Faster Race Than Battery Manufacturing

Battery circularity is now growing faster as an innovation field than battery production itself. According to the EPO-IEA analysis, international patent families linked to battery circularity recorded a 42% compound annual growth rate between 2017 and 2023, compared with 16% for rechargeable battery production and 2% across all technical fields.

That acceleration matters because patents are early signals of where companies believe future value will lie. Battery economy is no longer only about who can mine lithium, refine cobalt or manufacture cells.

It is also about who can safely collect used batteries, identify their chemistry, dismantle packs, recover metals, repair cells, repurpose units and return materials to the supply chain.

The study frames circularity as a response to two linked risks: waste and concentration. Spent batteries can cause fire, toxic gas and contamination risks if mishandled. On the other hand, recycling transition minerals, including nickel, cobalt and lithium, can produce about 80% lower greenhouse gas emissions than primary materials.

Where The Patent Race Is Moving

Asia, and particularly China, is leading the battery circularity race. The report says Asian applicants accounted for 63% of international patent families in the field in 2023.

Brunp, the battery recycling subsidiary of CATL, has overtaken earlier leaders from Japan and Korea, filing more than twice as many international patent families in 2020 – 2023 as Toyota, the second-largest filer over the last two decades.

China’s broader dominance is even more important for policymakers. Its share of international patent families in battery circularity rose from 5% in 2013 to 29% in 2023. In the five years to 2023, Chinese national patents represent approximately 70% of all national and international applications in the field.

This intersects directly with Africa’s mineral future. The Democratic Republic of Congo mined around two-thirds of global cobalt production in 2024, while China accounted for almost 80% of cobalt refining and approximately 70% of refined lithium production.

For African markets, the lesson is clear: mineral ownership does not automatically translate into industrial power.

Without refining, recycling, standards, patents, manufacturing partnerships and logistics capacity, countries can remain suppliers of raw inputs while higher-value circularity technologies are built elsewhere.

Why Circularity Could Shift African Leverage

Battery circularity could give African economies a second chance to capture value in the clean-energy transition.

Instead of exporting minerals and importing finished technologies, countries can build systems around battery repair, testing, second-life use, safe transport, end-of-life collection and material recovery.

This matters for access to energy, too. Repurposed batteries can support mini-grids, telecom towers, solar home systems, cold storage and commercial backup power.

In markets where electricity reliability still shapes business survival, second-life batteries could become an affordable bridge between renewable generation and resilient local power.

The ESG case is equally strong. Circularity reduces pressure on primary extraction, lowers emissions, limits hazardous disposal and can improve traceability. The IEA projects that recycling could reduce primary supply requirements by around 40% lower for copper and cobalt and around 25% lower for lithium and nickel by 2050 in the Announced Pledges Scenario.

The opportunity is not automatic. Informal e-waste handling, weak environmental enforcement and limited technical capacity could turn battery waste into another public health burden.

However, with the right rules, circularity can support jobs, cleaner cities, safer waste systems and stronger industrial participation.

What Governments And Markets Must Build

- African governments should treat battery circularity as industrial policy, not just waste management. That means setting clear rules for collection, transport, storage, testing and recycling before battery volumes overwhelm existing systems.

- Regulators need extended producer responsibility frameworks that make manufacturers, importers and fleet operators accountable for end-of-life batteries.

- Customs agencies and standards bodies should track battery imports, chemistry, ownership and disposal pathways.

- Energy ministries should plan for second-life batteries in distributed renewable systems, while environment ministries set safety rules for dismantling and recycling.

- Investors also have a role. The continent needs patient capital for battery diagnostics, recycling pilots, logistics networks, safe storage facilities and partnerships with global technology owners.

The EPO-IEA study notes that scaling recycling requires clear targets, better collection systems, design-for-disassembly, advanced recovery technologies and supportive policy and investment frameworks.

- For companies, the message is practical: the circular battery market will reward those who can prove quality, safety and traceability.

- For citizens, it means batteries should not disappear into informal dumpsites.

They should move through accountable systems that protect communities and return value to the economy.

Path Forward – Building Africa’s Circular Battery Future Now

Africa should build battery circularity early: standards first, collection systems next, then regional recycling and second-life markets linked to clean energy access.

The priority is not to copy today’s industrial leaders, but to close the value gap. If Africa combines minerals, policy, finance and innovation, battery waste can become a new source of climate resilience, industrial jobs and ESG credibility.