The oil market has entered one of its most fragile moments in decades, with the IEA warning that supply, prices, refining and petrochemical demand have all been shaken by the Middle East conflict.

For Africa, the shock is not distant. It touches fuel prices, LPG access, aviation, imports, public budgets and the case for faster energy resilience.

Oil Shock Tests Africa’s Energy Resilience

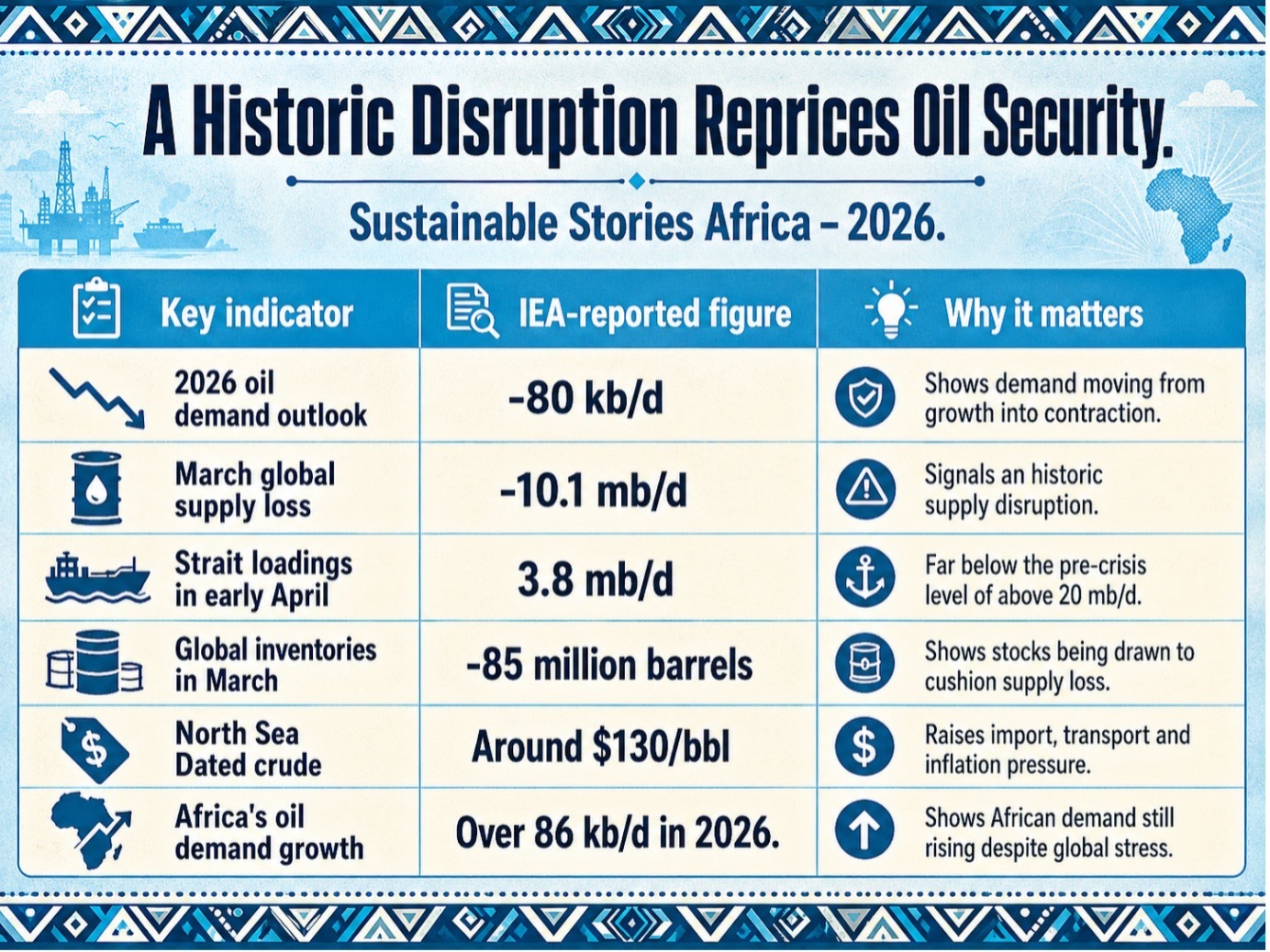

The International Energy Agency’s 14 April 2026 Oil Market Report presents a dramatic reset of the global oil outlook: demand is now expected to contract by 80,000 barrels per day in 2026, rather than grow, after conflict in the Middle East disrupted production, shipping and refining flows.

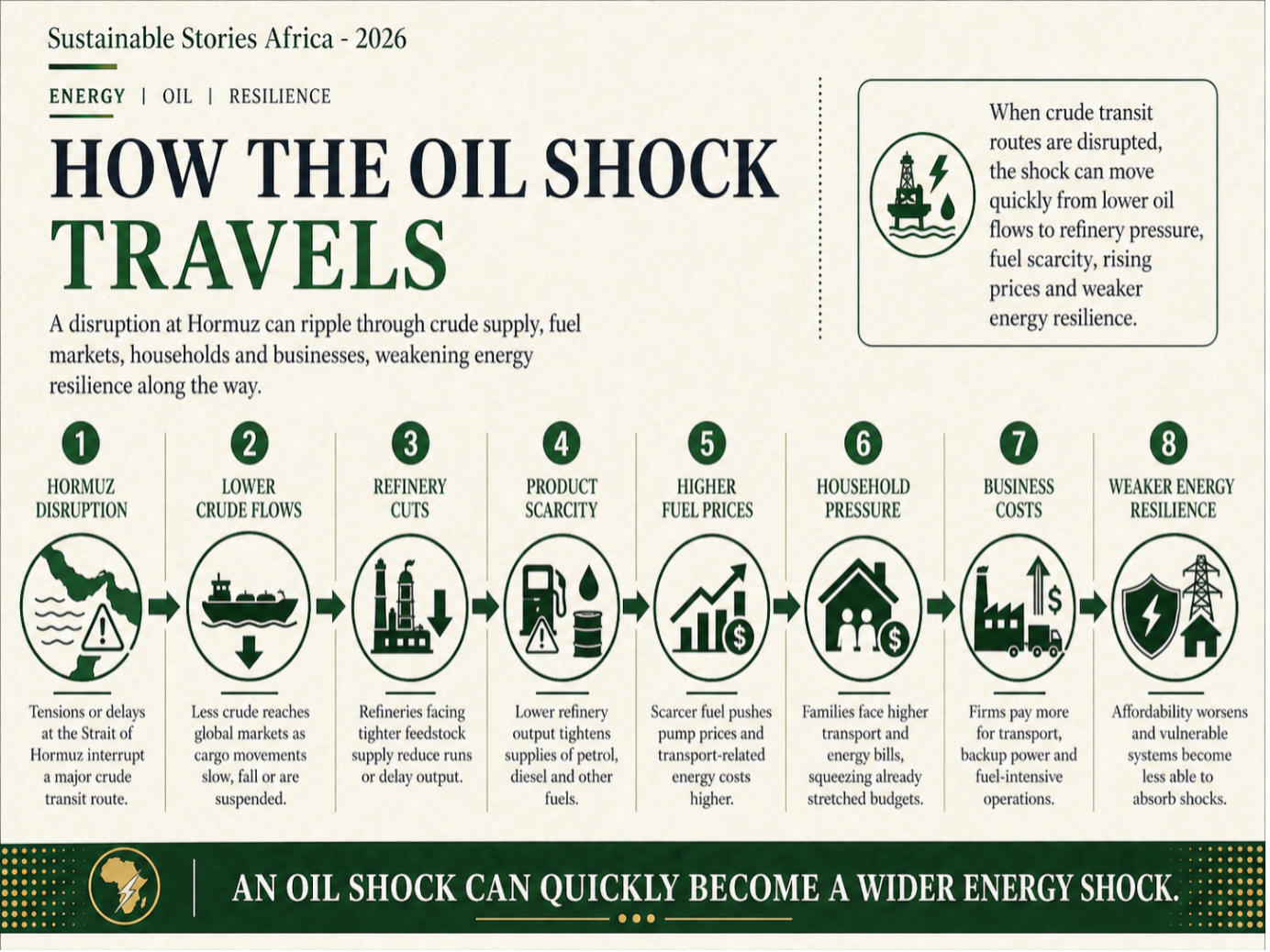

The shock is centred on the Strait of Hormuz, one of the world’s most important oil transit routes. The IEA says shipments through the Strait were severely restricted in early April, with crude, natural gas liquids and refined product loadings averaging around 3.8 million barrels per day, compared with more than 20 million barrels per day in February before the crisis.

For African markets, the story is both macroeconomic and personal. It is about foreign exchange pressure, diesel for logistics, jet fuel for travel, LPG for cooking, plastics and packaging supply chains, and the fiscal cost of shielding households from price spikes.

A Historic Disruption Reprices Oil Security

The IEA calls the March supply shock the largest disruption in history.

Global oil supply fell by 10.1 million barrels per day to 97 million barrels per day, while OPEC production dropped by 9.4 million barrels per day month-on-month to 42.4 million barrels per day.

Non-OPEC supply also declined by 770,000 barrels per day to 54.7 million barrels per day.

Prices moved with the urgency of a market searching for barrels.

The report says physical crude prices rose to around $150 per barrel, while middle distillate prices in Singapore reached all-time highs above $290 per barrel.

North Sea Dated crude was trading around $130 per barrel at the time of writing, about $60 above pre-conflict levels.

The key uncertainty is whether flows through Hormuz normalise. In the IEA’s base case, shipments gradually resume from May, allowing oil production and refinery activity to recover through the third quarter.

In a protracted case, disruptions continue, demand falls sharply, and the world would need deeper demand-reduction measures to balance the market.

Petrochemicals, Planes, and Households Feel Pressure

The first wave of demand destruction has not come mainly from drivers. It has come from petrochemical feedstocks, aviation and LPG-linked markets.

The IEA says LPG, ethane and naphtha account for the bulk of April’s demand drop, falling by 1.8 million barrels per day as supply chains to Asia were thrown into disarray.

Petrochemicals sit at the centre of this disruption because a relatively small group of large producers depends heavily on traded feedstocks.

Middle Eastern petrochemical production has been hit by reduced feedstock, plant damage, and the disruption of overseas markets. Across Asia, a reduction of 10% to 30% have affected steam crackers, aromatics plants and propane dehydrogenation facilities.

This matters for African economies even when the plants are far away. Plastics, packaging, textiles, construction materials and fertiliser supply chains all carry petrochemical exposure.

When feedstocks tighten, costs travel across borders through imported goods, manufacturing inputs and logistics.

The report also identifies pressure on households and businesses that use LPG, with non-OECD countries in South and Southeast Asia, Africa and Latin America introducing demand-saving measures.

Countries listed include Egypt, Ethiopia, Mauritius and South Sudan, as well as Asian and Latin American economies.

Resilience Can Turn Crisis Into Reform

The positive lesson is not that Africa can escape oil shocks overnight. It is that countries can reduce exposure over time through better storage, smarter subsidies, cleaner transport, stronger public transit, local refining discipline, diversified cooking fuels and faster deployment of renewables.

Africa’s oil demand is still expected to rise by 86,000 barrels per day in 2026 to 4.83 million barrels per day, even as global demand contracts. That growth reflects expanding economies, transport needs, urbanisation and energy access gaps.

However, it also means countries remain vulnerable when oil prices surge and currencies weaken.

The IEA report shows how energy security is now a whole-economy issue. Refiners are struggling with disrupted crude supplies. Global crude runs are expected to decline by an average of 1 million barrels per day in 2026.

Inventories are being drawn down, with global observed stocks falling by 85 million barrels in March, while stocks outside the Middle East Gulf drop by 205 million barrels as Hormuz flows were choked off.

What Policymakers And Markets Must Do

African governments should treat this oil shock as a planning signal.

- The first priority is targeted consumer protection: support should focus on public transport, food logistics, hospitals, schools and low-income households rather than broad fuel subsidies that drain budgets and benefit higher-income consumers.

- The second priority is strategic preparedness. Countries need better fuel stock policies, transparent import planning, emergency procurement rules and clearer communication when shortages emerge.

The IEA notes that emergency stock releases are providing relief, including the largest coordinated stock release in IEA history, with member countries making emergency oil stocks available through government-controlled reserves and lowered industry stockholding obligations.

- The third priority is demand-side resilience. Governments can reduce pressure through public transport expansion, efficient freight systems, teleworking rules during crises, fuel-efficiency standards and accelerated clean cooking alternatives.

These measures are not just climate policies; they are cost-of-living and economic stability policies.

For investors and companies, the message is equally clear: oil volatility is now a core business risk. Airlines, logistics firms, manufacturers, food distributors and petrochemical importers need hedging strategies, diversified suppliers and stronger energy-efficiency plans.

Path Forward – Build Oil Resilience Beyond Emergency Response

Africa should use this shock to strengthen energy security before the next crisis arrives. Strategic stocks, targeted subsidies, efficient transport and diversified cooking fuels must become standard policy, not temporary reaction.

The deeper path is structural: reduce oil dependence where alternatives already work, protect vulnerable households and build cleaner, more resilient energy systems. The oil market is warning governments that affordability and sustainability now move together.