The International Energy Agency’s Gas Market Report, Q2 - 2026, shows how a single chokepoint can redraw the economics of energy security, from Asia’s LNG buyers to Africa’s gas exporters and power systems.

The report’s central warning is clear: lower prices and new supply are starting to ease global markets; however, the Middle East conflict has revived volatility, rationing, fuel-switching and long-term supply uncertainty.

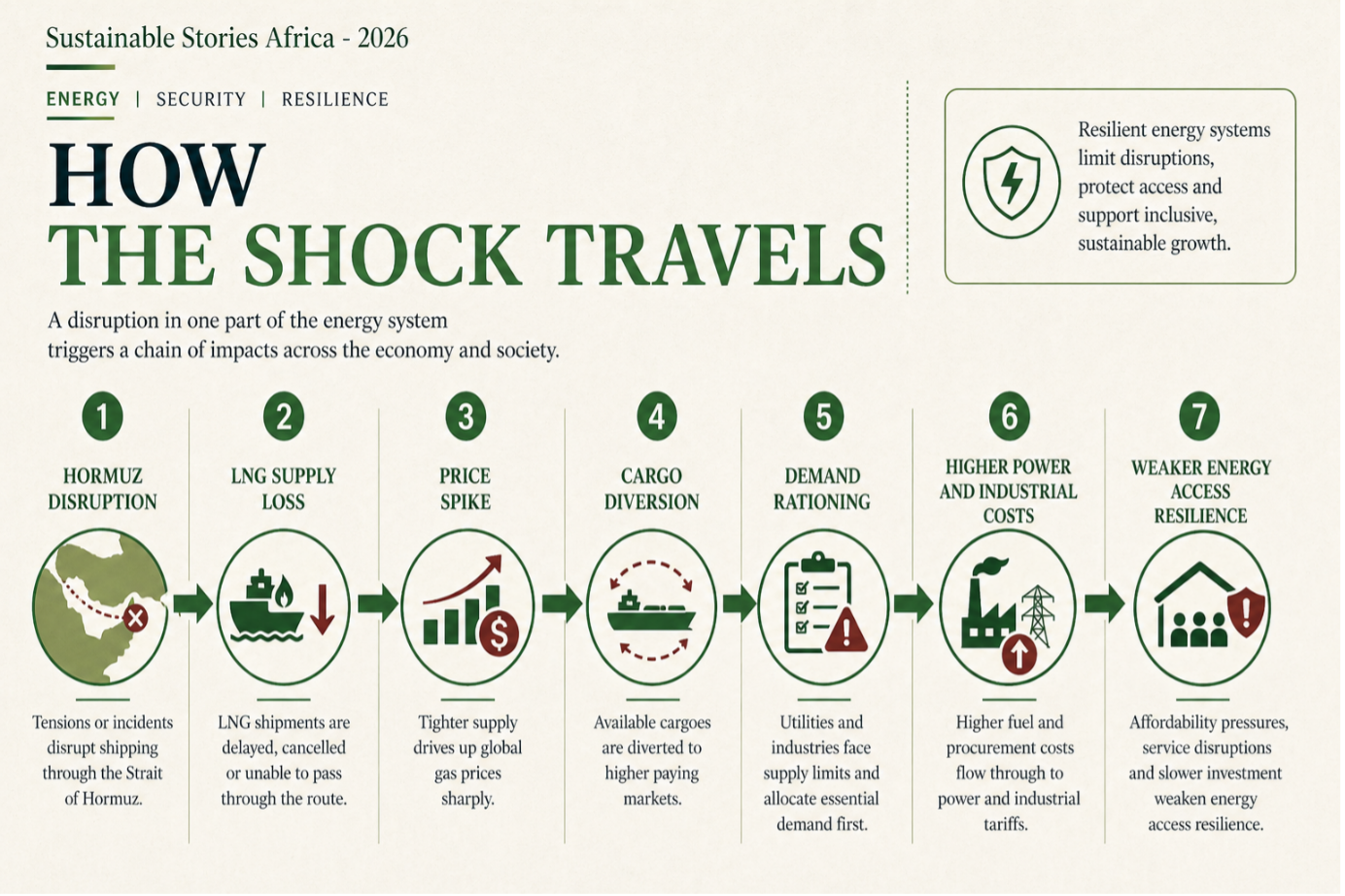

Gas Shock Tests Modern Energy Security

The global gas market entered 2026 with signs of relief. LNG supply was rising, prices were softening, and buyers in Asia and Europe were beginning to see the benefits of new liquefaction capacity.

Then the Strait of Hormuz crisis changed the story.

The IEA says the effective closure of the strait removed approximately 20% of global LNG supply from the market, disrupted short-term fundamentals, and altered the medium-term outlook for natural gas.

The shock pushed Asian and European gas prices to their highest levels since the 2022/23 energy crisis and forced governments and companies to adjust demand.

For African markets, the lesson is not simply about gas prices. It is about vulnerability. A disruption thousands of kilometres away can raise import costs, shift cargo flows, weaken industrial supply, and complicate the politics of the energy transition.

It also creates openings for African exporters, especially where projects are already producing, but only if reliability, infrastructure and domestic safeguards improve.

A Market Rebalanced Before It Snapped

Before the crisis, global LNG trade was expanding strongly. The IEA estimates that LNG supply increased by about 12%, or 29 billion cubic metres, year-on-year between October and February, supported by new projects in North America and Africa.

The Plaquemines LNG plant in Louisiana alone accounted for almost half of the incremental LNG supply over that period.

That extra supply helped reduce prices. In Europe, TTF prices fell 24% year-on-year in the first two months of 2026, while Asian Platts JKM prices declined 27%.

However, March reversed that easing. Global LNG production fell 8%, or 4 bcm, year-on-year, as loadings from Qatar and the United Arab Emirates dropped by 9.5 bcm.

The price reaction was immediate. European TTF month-ahead prices averaged $18/MBtu in March, while Platts JKM traded close to $21/MBtu.

Volatility rose sharply: TTF month-ahead volatility hit 160%, while JKM volatility climbed close to 300%.

Africa Sees Risk And Opportunity

Africa appears in the report both as a contributor to new supply and as a region exposed to wider market volatility.

The continent added to the LNG supply upside, led by Tortue FLNG off Senegal and Mauritania, which started operations in the second quarter of 2025 and contributed about 2 bcm of incremental supply during the winter. Congo’s Nguya FLNG also added cargoes after starting up in early 2026.

Nigeria LNG also strengthened output, increasing production by about 2 bcm year-on-year, or 10%, to its highest level since winter 2020/21. Overall, African LNG exports rose by 14%, or 3.5 bcm.

However, the opportunity is uneven. Egypt, which had become a net importer in the second half of 2024, exported eight cargoes during the winter while also importing record volumes of LNG.

Algeria’s exports declined by close to 1 bcm. For policymakers, this reinforces a hard reality: export ambition means little without feedgas security, domestic supply planning and credible infrastructure maintenance.

The report also notes that Egypt increased LNG imports by 180% year-on-year in March and the first 20 days of April to compensate for regional shortfalls linked to the conflict, further tightening global market fundamentals.

Demand Pain Moves Through Importers

The demand-side story is just as important as the supply shock. The IEA says natural gas demand fell in key LNG import markets in March due to higher prices, weather factors and policy measures.

Several Asian countries introduced fuel switching and demand-side controls to reduce gas use.

India shows what that looks like in practice. LNG sourced through the Strait of Hormuz accounted for almost 30% of India’s primary gas supply and nearly 60% of total LNG imports in 2025.

In response, India issued a Natural Gas Supply Regulation Order, prioritising households, transport and fertiliser plants while cutting some deliveries to other industrial and commercial consumers by 10% to 30%.

For Africa, the warning is direct. Gas-to-power strategies, fertiliser production, industrial parks and clean cooking policies can all become fragile if supply contracts, storage systems and domestic allocation rules are weak.

High global LNG prices do not stay within trading screens; they reach power tariffs, food systems, factory margins and household budgets.

Better Contracts Can Protect Transition

The IEA’s clearest policy message is that energy security now requires a stronger global gas supply architecture.

It says the crisis highlights the need for continued investment across gas and LNG value chains, as well as electricity and other energy sources, to support supply security and balanced growth.

It also points to the value of diversified long-term contracts in reducing short-term price volatility for both buyers and sellers.

For African governments, this is not an argument for gas without transition discipline. It is an argument for planning.

Gas can support power reliability, fertiliser production, cleaner industrial heat and grid flexibility as renewables grow. However, it must be governed through transparent procurement, methane controls, domestic supply obligations, realistic tariff design and stronger regional power pools.

For investors, Africa’s opportunity is credibility. Buyers will reward projects that can deliver reliable volumes, meet environmental standards, and avoid repeated feedgas or security disruptions.

Producers that combine export capacity with domestic energy value will have a stronger development case than those that treat LNG purely as a foreign-exchange asset.

Governments Must Build Shock Absorbers

The next phase of gas policy should be about resilience, not rhetoric.

- Governments need clearer rules for prioritising gas supply during crises, stronger storage and backup planning, and better coordination among the power, industry and agriculture ministries.

- Regulators should stress-test gas-to-power systems against import disruptions, price spikes and delayed cargoes.

- Businesses also need to move. Large industrial users should diversify fuel options without locking into high-emission pathways.

- Utilities should pair gas flexibility with renewables, storage, grid upgrades and demand response.

- Financiers should assess not only project returns, but also systemic exposure: who pays when imported gas becomes scarce or unaffordable?

Africa’s strongest position will come from balanced energy portfolios: domestic gas where viable, renewables where fastest, regional interconnections where efficient, and contracts that protect consumers from global shocks.

Path Forward – Requires Resilient Gas Planning

Africa should treat the IEA report as an early warning. Gas can support development, but only if supply security, affordability and climate safeguards are designed together.

The priority is practical: diversify supply, strengthen contracts, reduce methane, protect households and critical industries, and use gas as a bridge to a cleaner, more reliable energy system, not as a substitute for the transition.