A new study of Cameroon’s industrial sector shows that companies are increasingly publishing environmental information, but much of it remains descriptive, positive and difficult to compare.

For African markets, the finding raises a wider question: can voluntary ESG reporting build trust without stronger standards, monetary data and independent assurance?

Disclosure Without Data Limits Accountability

Cameroon’s industrial companies are beginning to tell a clearer environmental story; however, the evidence suggests that the stories remain incomplete.

A 2026 peer-reviewed study, Environmental Disclosure in Cameroon’s Industrial Sector: Insights from Case Studies, examined 12 sustainability reports from four industrial enterprises between 2018 and 2021.

It found that companies consistently disclosed environmental themes such as emissions, materials, waste, water, biodiversity and compliance, but the information was mostly positive, mostly narrative and rarely linked to monetary values.

For policymakers, investors, communities and regulators across the OHADA zone, the message is clear: environmental disclosure is no longer optional in practice, but it still lacks the standardisation it requires to make reporting useful.

Industrial Growth Needs Environmental Accountability

Industrialisation remains central to Cameroon’s economic development, including Agro-food processing, cement, brewing and building materials.

However, factories also produce emissions, wastewater, waste streams, energy demand and local environmental risks.

That is why environmental disclosure matters. It gives communities, regulators, investors and lenders a way to understand how companies affect natural resources and what they are doing to reduce harm.

The study defines environmental disclosure as a corporate practice that enables firms to demonstrate accountability by reporting the impact of their activities on the environmental actions taken to mitigate negative externalities.

The issue is not whether companies are speaking. It is whether they are saying enough, in a form that can be verified, compared and acted upon.

Study Reveals Clear Reporting Imbalance

The study reviewed sustainability reports from Boisson du Cameroun/SABC, SOCAPALM, CIMENCAM and Dangote Cement, covering the brewery, agro-food and building materials sectors.

These firms were selected because they published CSR or sustainability reports consistently and referenced international frameworks such as the Global Reporting Initiative and the United Nations Global Compact.

The research used content analysis to examine three core questions:

- Which environmental themes do companies disclose

- What type of information do they provide

- Whether disclosures were qualitative, quantitative or monetary.

The results show a market in transition. Environmental reporting exists. Some companies provide details on water use, biodiversity protection, waste recovery, emissions and environmental compliance.

However, the reporting structure remains uneven, with limited integration of financial or cost-based information.

That matters for ESG governance because narrative claims alone cannot show whether environmental performance is improving, whether risks are material, or whether communities are being protected.

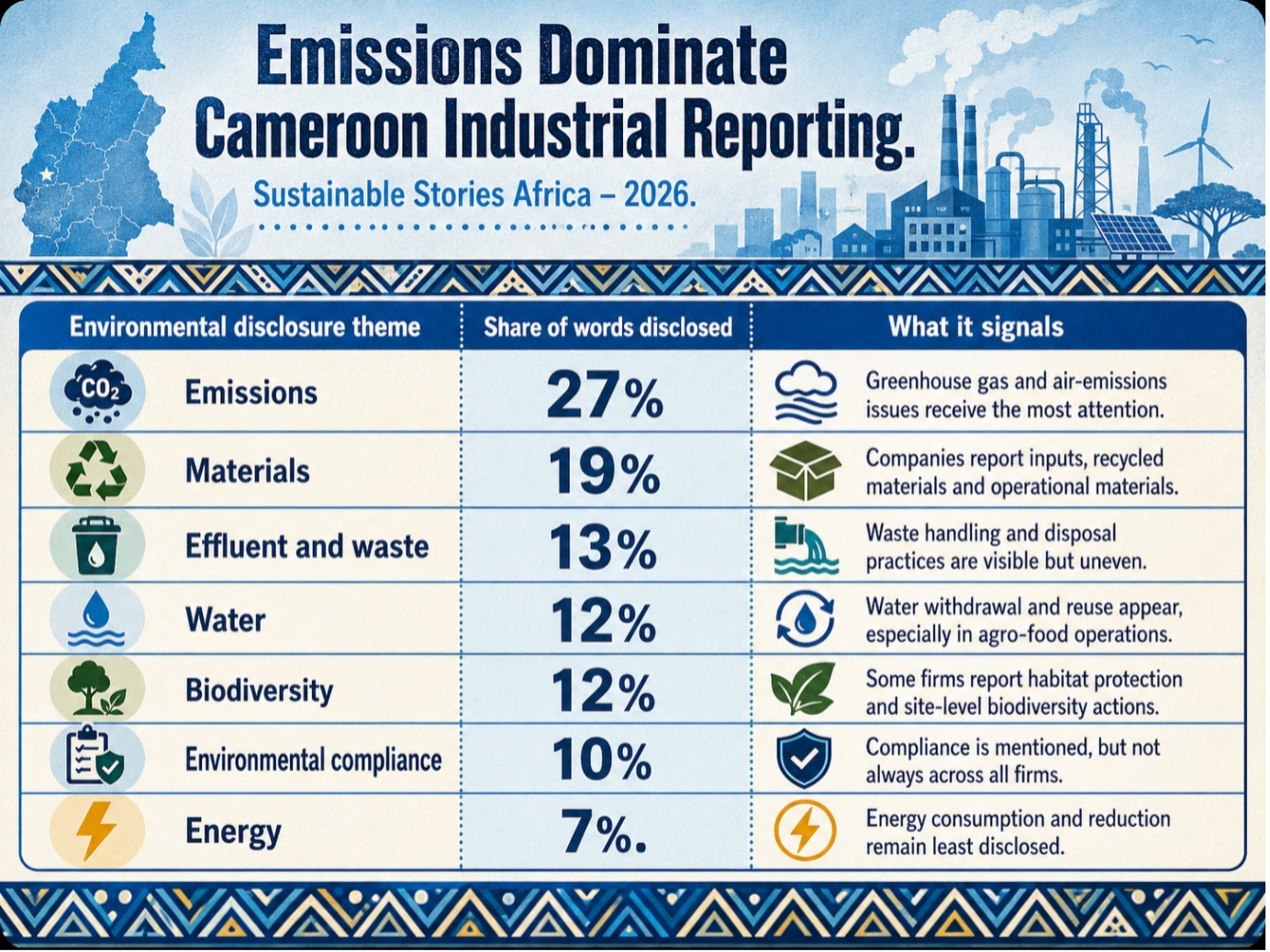

The most disclosed theme was emissions, accounting for 27% of environmental disclosure by word count. This was followed by materials at 19%, effluent and waste at 13%, water and biodiversity at 12% each, environmental compliance at 10%, and energy at 7%.

This is a revealing pattern. Companies appear more willing to discuss visible environmental pressures such as emissions, waste and materials.

However, they provide less information on energy consumption, energy intensity, cleaner energy transitions and energy reduction, even though energy is central to climate strategy, industrial competitiveness and cost control.

For African manufacturers facing rising energy costs and pressure to decarbonise supply chains, that omission is not minor.

It limits investors' and regulators' abilities to assess whether companies are preparing for a lower-carbon economy.

Positive Narratives Outweigh Harder Truths

The study found that 90.23% of the environmental information disclosed was positive, compared with only 9.77% negative. In practical terms, companies were far more likely to report commitments, improvements, compliance statements and environmental initiatives than incidents, penalties, shortcomings or unresolved environmental impacts.

That pattern is not unique to Cameroon. Corporate sustainability reports globally often lean toward reputation-building.

However, in a market where disclosure is still developing, excessive positivity can weaken trust.

A company may say it is committed to reducing emissions. But stakeholders also need to know the baseline, the annual performance trend, the cost of mitigation, whether targets were missed, whether communities complained, and whether regulators imposed sanctions.

The study also found that environmental information was overwhelmingly qualitative. 93.85% of disclosure was descriptive, while only 6.15% was non-monetary quantitative. Monetary environmental information was largely absent.

That is the core accountability gap. Without numbers, reporting is communication. With comparable metrics, reporting becomes governance.

What Better Disclosure Could Unlock

Better environmental reporting can do more than satisfy regulators. It can reduce financing costs, improve operational efficiency, protect communities and help African firms meet emerging global sustainability expectations.

- For companies, stronger disclosure can clarify where energy is being wasted, where water stress is rising, where waste can become a circular-economy input, and where emissions reductions can protect export competitiveness.

- For communities, it can answer basic questions: what is being released into the air, how water is being used, whether waste is safely handled, and whether companies are complying with environmental laws.

- For investors and banks, it creates a basis for risk pricing. A lender cannot properly assess climate or environmental exposure if sustainability reports contain only broad claims. A development finance institution cannot credibly support the green industry if performance data is not measurable.

- For regulators, standardised reporting can turn fragmented company disclosures into a national evidence base for industrial policy, pollution control and green-growth planning.

OHADA And Regulators Need Clearer Standards

The study’s recommendation is especially important for the OHADA zone. It argues that the current reporting environment needs a distinct accounting framework for social and environmental information, similar to the existing OHADA framework for financial information.

It also suggests that elements of IFRS S1 and IFRS S2 could be integrated into existing financial reporting rules.

The regulatory logic is straightforward. If environmental data remains voluntary, fragmented and mostly narrative, companies can choose what to highlight and what to omit.

If it becomes structured, comparable and assurance-ready, stakeholders can evaluate performance more fairly.

This does not mean burdening companies with paperwork. It means building a reporting system that supports better management decisions, stronger investment confidence and more credible sustainability claims.

Path Forward – For Industrial ESG

Cameroon’s industrial sector now needs a shift from environmental storytelling to environmental accounting.

That means clear standards, measurable indicators, monetary data and stronger assurance.

For African markets, the lesson is wider: ESG credibility depends on evidence. Companies should report not only what they are proud of but also what they are improving, what they are spending, and what still needs to change.