Petrochemicals are moving from the margins of climate debate to the centre of ESG scrutiny, as plastics, fertilisers and chemical feedstocks become a new growth frontier for fossil fuel demand.

A Lund University report warns that finance, ownership ties and weak governance are locking in emissions-intensive production, with major implications for African economies seeking industrial growth without deepening climate risk.

Petrochemicals Finance Becomes Africa’s ESG Test

Petrochemicals lie within everyday life: plastic packaging, fertilisers, paints, medicines, pesticides, textiles and industrial materials.

However, behind those products is a harder climate question: can ESG funds and development finance continue to support fossil-based chemical expansion while claiming alignment with net-zero pathways?

A 2023 Lund University study argues that petrochemicals deserve far greater climate attention because the chemical industry uses more fossil-fuel-based energy than any other industry. Petrochemicals are the largest share of that sector and rely heavily on oil, gas and coal feedstocks.

For Africa and other emerging markets, the stakes are practical. Petrochemicals promise jobs, tax revenue, fertiliser supply, industrial upgrading and export earnings.

However, without stronger safeguards, they can also deepen fossil dependence, expose communities to pollution and lock public finance into long-lived carbon assets.

A Hidden Carbon Market Comes Into View

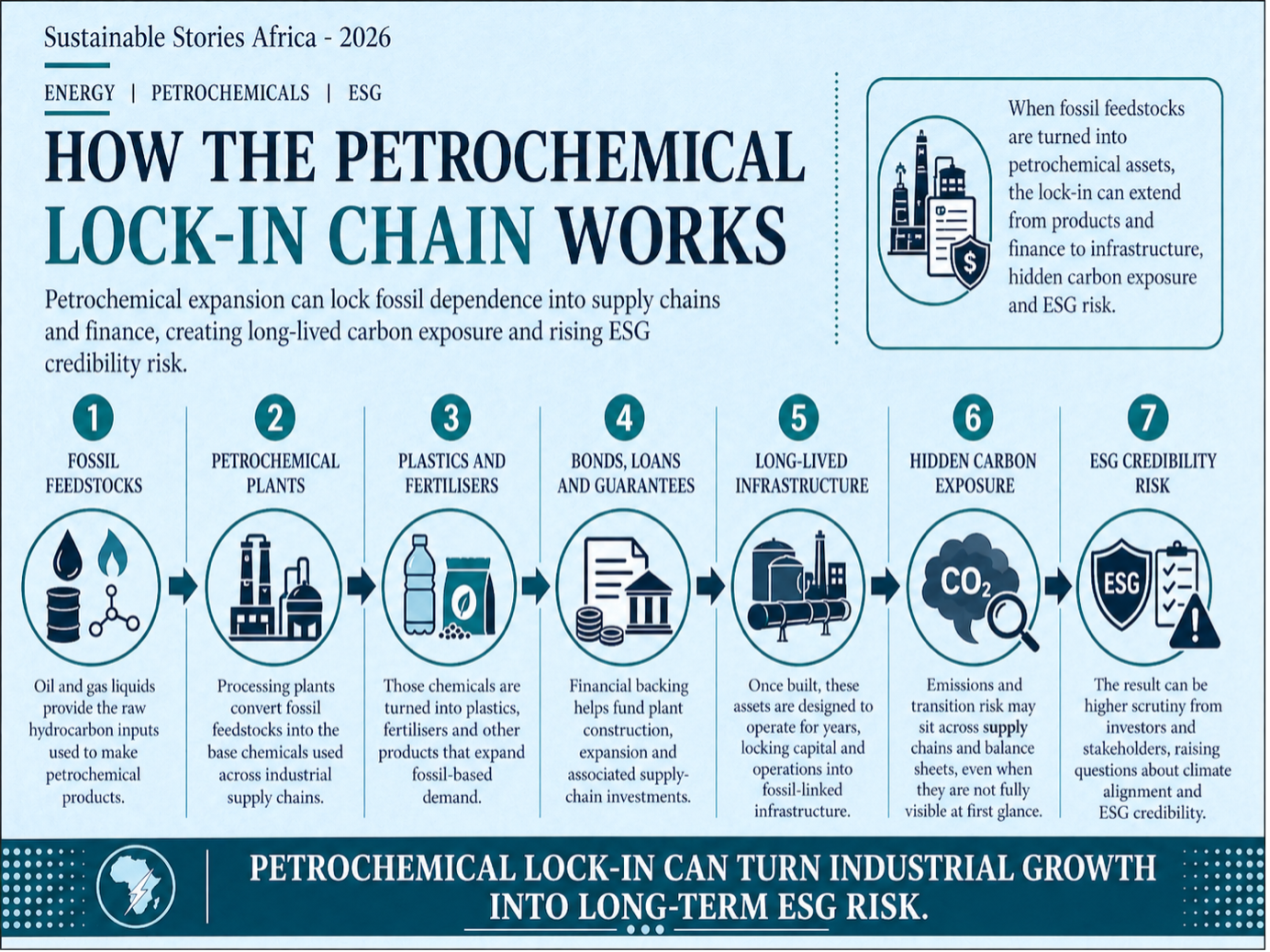

The report’s central warning is clear: petrochemicals are becoming a climate lock-in strategy for fossil fuel companies and petrostates as transport fuel demand faces long-term pressure.

It notes that plastics and other petrochemicals are forecast to become the largest driver of oil demand growth from 2025, while plastics demand could triple by 2050 without major changes in consumption.

That makes the sector an ESG blind spot. Investors often focus on oil extraction, coal power and vehicle emissions, but the chemical value chain is less visible to consumers and regulators. In practice, the carbon risk is embedded in products, plants, pipelines, bonds, loans, guarantees and state-backed industrial strategies.

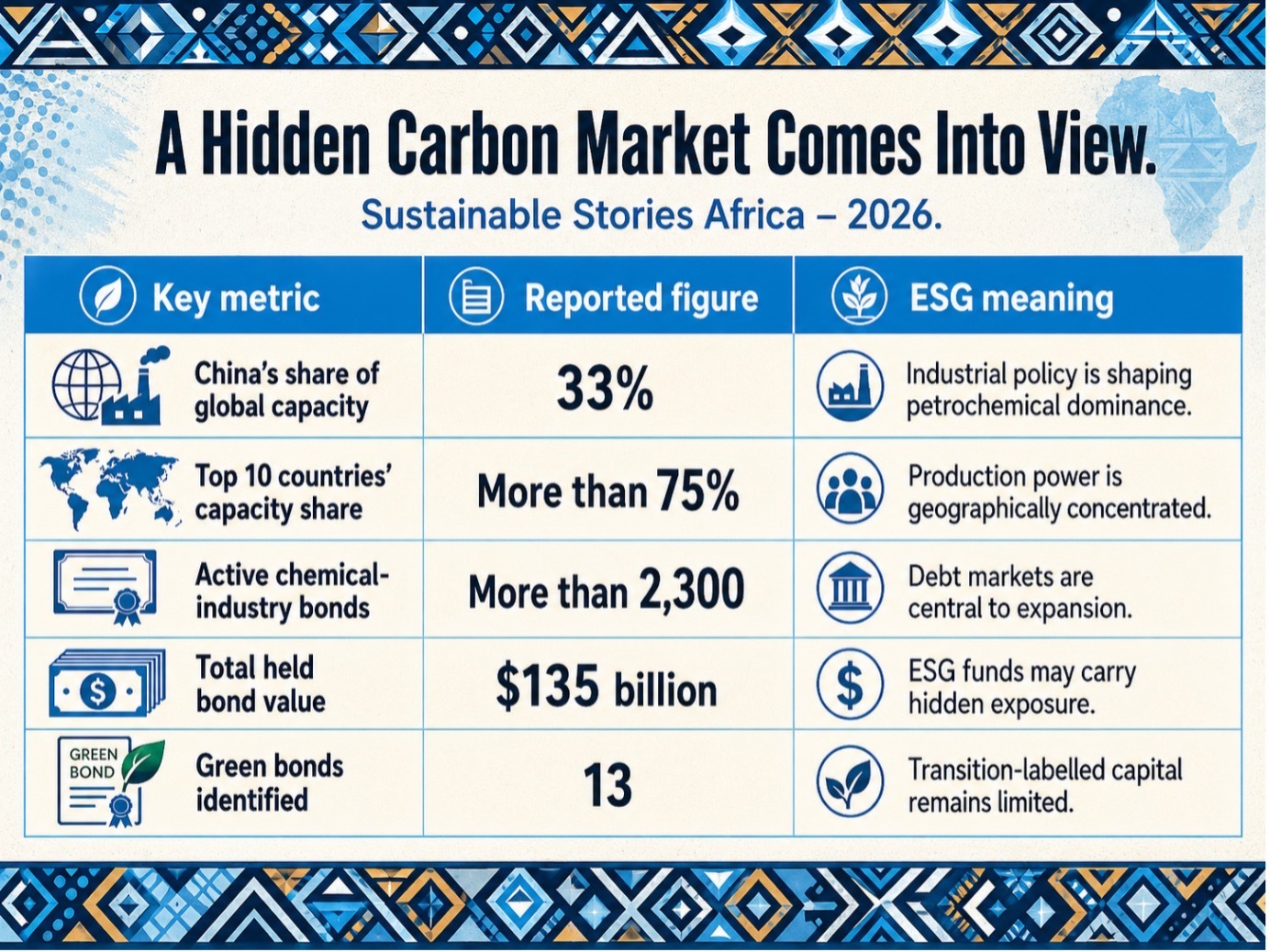

The global map is already concentrated. The report says the ten countries with the largest petrochemical production capacity account for more than 75% of global capacity, led by China at 33%, followed by the United States at 12%, with India, South Korea and Saudi Arabia each at 5%.

How Capital Locks In Fossil Chemicals

The financing story is where the report becomes most relevant for ESG funds. Lund researchers found that new petrochemical production is enabled less by stock ownership than by credits, project finance, loans, bonds and guarantees.

The study says the global chemical industry had more than 2,300 active bonds in late 2021, with a total held value of $135 billion, but only 13 were identified as green bonds.

Public finance also plays a catalytic role. The report estimates that the European Central Bank purchased petrochemical-sector bonds worth a conservative €14 – €15 billion through bond-buying programmes.

It also cites $31 billion in direct export credit agency financing for petrochemicals from 2000 to mid-2021, plus $23 billion in loan guarantees over the same period.

For Africa, Mozambique shows both the promise and the risk. The Cabo Delgado natural gas and petrochemicals cluster is described as Africa’s largest example of foreign direct investment to date, with associated gas, fertiliser and gas-to-liquid projects.

However, most LNG output is destined beyond Africa. The project received more than $8 billion in direct state financing and $6.14 billion in loan guarantees from export-credit agencies and public financiers.

South Africa also appears in the global petrochemical finance story through Sasol. The report lists Sasol among major petrochemical producers. It describes the Lake Charles chemical complex expansion in Louisiana as a $12.8 billion project that tripled Sasol’s chemical production capacity in the United States.

A Cleaner Chemicals Path Can Create Value

The positive story is not that Africa should avoid industrialisation. African industrialisation must avoid becoming a dumping ground for carbon-intensive production models that richer markets later regulate.

A cleaner petrochemicals pathway could support fertiliser security, local manufacturing, circular plastics, green hydrogen-based chemicals, lower-carbon industrial parks and better jobs.

For countries seeking value addition from gas and minerals, the opportunity is to attach strict transition conditions to new projects: credible emissions accounting, methane controls, pollution safeguards, community protection, renewable power procurement and clear pathways away from fossil feedstocks.

This is also a competitiveness issue. As buyers, lenders, and regulators tighten sustainability requirements, plants built without transition-readiness may become stranded assets.

ESG funds that fail to examine petrochemical exposure could discover that “industrial diversification” in a portfolio is also hidden fossil expansion.

What Governments And ESG Investors Must Do

The report’s recommendations are blunt.

- Governments should restrict further expansion of fossil-based petrochemical capacity, mandate transition plans for existing companies and use state ownership to push chemical firms towards transformation.

- Financial institutions face an equally direct test. The study argues that public and private banks, insurers, development finance institutions and asset managers should stop financing fossil-based and emissions-intensive petrochemical production. It specifically calls for public financial institutions to implement moratoria or bans on such projects across loans, bonds and guarantees.

- ESG-focused investors should track hidden carbon flows in chemical and plastics value chains.

For African regulators, that means three practical shifts.

- First, classify petrochemicals as a climate-relevant sector in national transition plans.

- Second, require full disclosure of project finance, emissions, feedstocks, offtake markets and community impacts.

- Third, ensure development banks do not finance industrial projects that lack credible low-carbon conversion pathways.

Path Forward – Align Finance With Real Transition

Africa needs an industrial policy that rewards value addition without importing yesterday’s carbon risks.

Petrochemical projects should face clear climate, finance and community tests before public money, guarantees, or ESG-labelled capital supports them.

The priority is transparency: disclose the money, emissions, markets and transition plans behind every major project.

ESG credibility will depend not on labels, but on whether finance moves chemical value chains away from fossil dependence.