Africa’s financial systems are entering a new era of climate accountability, driven by global sustainability standards and rising regulatory expectations.

However, progress remains uneven, with disclosure maturity varying sharply across markets.

As climate risks intensify, the central question is whether African institutions move from fragmented compliance to credible, decision-useful sustainability reporting that drives real resilience and capital flows?

Closing Africa’s Climate Disclosure Gap

Africa’s climate story is no longer just about vulnerability; it is increasingly about visibility.

Across financial markets, regulators, insurers, and corporates are beginning to confront a new reality: climate risk must be measured, disclosed, and managed as a core financial variable.

The release of the February 2026 Milliman report marks a critical inflexion point, offering one of the most comprehensive snapshots of how eight African markets are navigating climate-related risk management and sustainability disclosures.

At stake is more than compliance. For African economies, alignment with global disclosure frameworks will determine access to capital, investor confidence, and long-term resilience in a climate-constrained world.

A Continent at a Disclosure Crossroads

Africa’s climate disclosure landscape is advancing, but unevenly and urgently.

Despite the introduction of global frameworks such as IFRS S1 and S2, no African market has attained full mandatory compliance across the board.

However, momentum is undeniable: countries such as Nigeria, Kenya, and Ghana are actively rolling out phased adoption timelines, while regulators increasingly frame climate governance as a fiduciary responsibility.

A defining insight from the report is stark: climate risk management is increasingly important in regulatory participation, but implementation remains fragmented and largely voluntary across the continent.

This creates a paradox. Africa is among the most climate-exposed regions globally; however, its financial systems are still building the institutional architecture required to quantify and disclose these risks effectively.

Mapping Africa’s Climate Disclosure Reality

The report reveals a multi-speed adoption landscape:

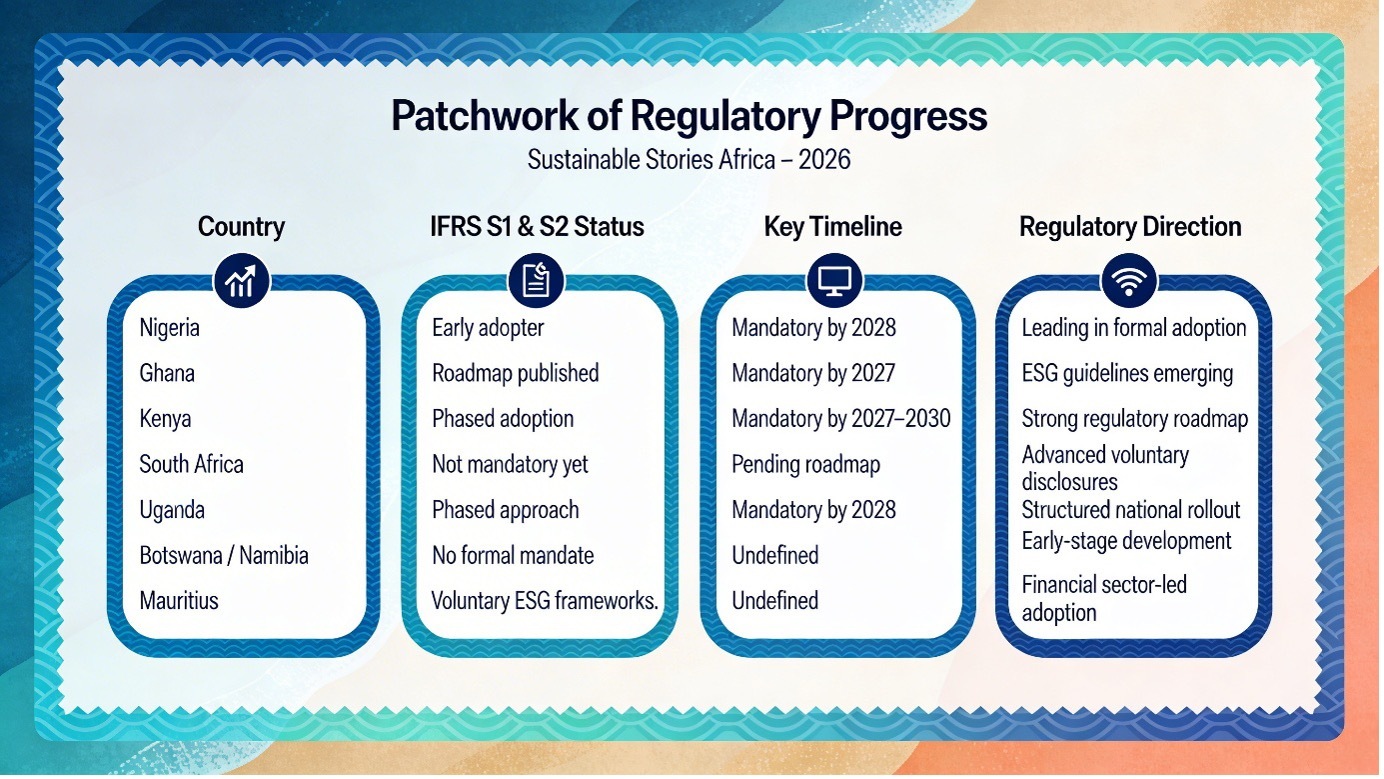

Patchwork of Regulatory Progress

Country | IFRS S1 & S2 Status | Key Timeline | Regulatory Direction |

|---|---|---|---|

Nigeria | Early adopter | Mandatory by 2028 | Leading in formal adoption |

Ghana | Roadmap published | Mandatory by 2027 | ESG guidelines emerging |

Kenya | Phased adoption | Mandatory by 2027–2030 | Strong regulatory roadmap |

South Africa | Not mandatory yet | Pending roadmap | Advanced voluntary disclosures |

Uganda | Phased approach | Mandatory by 2028 | Structured national rollout |

Botswana / Namibia | No formal mandate | Undefined | Early-stage development |

Mauritius | Voluntary ESG frameworks | Undefined | Financial sector-led adoption |

Nigeria is the first African country to formally adopt IFRS S1 and S2, with a phased roadmap culminating in mandatory compliance by 2028. However, early adoption remains limited, with only a handful of institutions leading.

Banking Leads, Insurance Lags

Across markets, climate regulation is more advanced in banking than in insurance. Central banks in Kenya, Ghana, and South Africa have introduced climate risk frameworks, while insurance regulation remains largely focused on disclosure.

This imbalance reflects a broader structural issue: climate risk is still being treated as a compliance exercise rather than an integrated enterprise risk function across sectors.

The Data Deficit Problem

A major constraint emerges clearly: data readiness.

In Ghana, for example:

- 80% of firms report gaps in governance, data systems, and emissions tracking

- Only 29% actively manage physical climate risks

- Only 22% assess asset vulnerability

These gaps underscore a critical bottleneck; without reliable data, disclosures risk becoming symbolic rather than decision-useful.

Leaders vs. Laggards

The report identifies a clear divide in disclosure maturity:

- South Africa: Most advanced, with comprehensive TCFD-aligned reporting

- Kenya: Emerging leader with structured reporting frameworks

- Nigeria and others: Early stage, with minimal climate metrics disclosure

Notably, many Nigerian insurers still do not publish climate-related disclosures, despite regulatory progress.

What Effective Climate Disclosure Unlocks

If Africa closes its disclosure gap, the upside is significant and tangible.

- Capital Access and Investor Confidence – Global investors increasingly rely on standardised ESG disclosures. Alignment with IFRS S1 and S2 can:

- Lower perceived investment risk

- Unlock climate finance flows

- Improve sovereign and corporate credit profiles

- Stronger Risk Management - Embedding climate risk into governance structures enhances:

- Scenario planning

- Stress testing

- Long-term asset valuation

As the report notes, sustainability disclosures are not just reporting tools; they are risk management frameworks built around governance, strategy, risk processes, and metrics.

- Competitive Advantage for Early Movers – Institutions that lead on disclosures gain:

- First-mover credibility

- Regulatory readiness

- Market differentiation

South African insurers already demonstrate this advantage through detailed climate reporting aligned with global standards.

- Systemic Resilience – At a macro level, better disclosures support:

- Financial system stability

- Climate adaptation planning

- Policy alignment with net-zero goals

What Must Happen Next

To move from fragmented progress to systemic transformation, four priorities emerge:

- Shift from Voluntary to Mandatory Frameworks – Regulators must accelerate timelines for mandatory adoption of IFRS S1 and S2, to ensure consistency across markets.

- Build Data Infrastructure and Capacity – Governments and regulators should:

- Invest in climate data systems

- Support emissions tracking frameworks

- Develop national taxonomies

- Strengthen Board-Level Accountability – Climate governance must be embedded at the highest level. As Nigeria’s Financial Reporting Council emphasises, climate oversight is now a core fiduciary duty.

- Integrate Climate into Financial Decision-Making – Institutions must move beyond disclosure toward:

- Climate-adjusted capital allocation

- Risk-based pricing

- Transition planning

- Leverage Global Partnerships – Collaborations such as the IFC–IFRS partnership are critical in providing:

- Technical guidance

- Training

- Implementation support across emerging markets

Path Forward – From Disclosure to Decision-Usefulness

Africa’s climate disclosure journey is gaining momentum, but credibility will depend on consistency, data integrity, and regulatory enforcement.

Moving from voluntary frameworks to mandatory, decision-useful reporting is now essential.

The next phase requires coordinated action, stronger institutions, clearer standards, and deeper integration of climate risk into financial systems. Done right, this transition positions Africa not just as a climate-vulnerable region, but as a credible, investable sustainability frontier.