Many companies still measure only a fraction of their emissions, leaving supply-chain, product and project-level impacts outside serious scrutiny.

A new corporate carbon accounting explainer argues that a credible net-zero strategy now requires three layers of measurement: organisational inventories, product carbon footprints and project-level accounting.

For African companies, the shift is becoming a market-access, investor-confidence and compliance issue.

Carbon Accounting Becomes Business Infrastructure

Corporate carbon accounting is no longer a technical exercise reserved for sustainability teams. It is becoming the evidence layer behind trade access, investor trust, product claims, carbon-credit integrity and net-zero credibility.

The uploaded explainer, Corporate Carbon Accounting, frames the challenge sharply: “Most companies only measure 10% of their carbon footprint.” It then sets out three levels of greenhouse-gas accounting that companies need to understand: organisational inventory, product carbon footprint, and project-level accounting.

For African and emerging-market companies, the stakes are rising. Exporters face carbon-border and product-claim rules. Manufacturers must understand energy, materials and logistics emissions. Banks and investors increasingly ask for verified emissions data.

Companies making net-zero claims can no longer rely on partial Scope 1 and Scope 2 reporting while ignoring the value-chain emissions that often dominate their real climate footprint.

Partial Measurement Weakens Net-Zero Claims

The central warning is simple: a company cannot manage what it does not measure, and it cannot credibly claim net zero if most of its emissions remain outside the boundary.

The explainer identifies Level 1 carbon accounting as the organisational inventory: measuring what a company emits across all scopes.

- Scope 1 covers direct emissions from sources a company owns or controls, such as boilers, company vehicles, generators and refrigerant leaks.

- Scope 2 covers purchased electricity, steam, heating or cooling.

- Scope 3 captures the wider value chain, including suppliers, logistics, employee commuting, product use and end-of-life impacts.

That third category is where many corporate claims become fragile. The explainer notes that Scope 3 typically accounts for 70% to 90% of a company’s total carbon footprint. It also flags a common error: reporting only Scope 1 and Scope 2 while claiming “net zero.”

For a Nigerian food processor, this could mean that diesel used at the factory is measured, but emissions from fertiliser, packaging, transport and product waste are missed.

For a cement distributor, office electricity may be reported, while embedded emissions in materials remain invisible. For a retailer, store operations may look efficient while imported products, logistics and disposal carry the real carbon load.

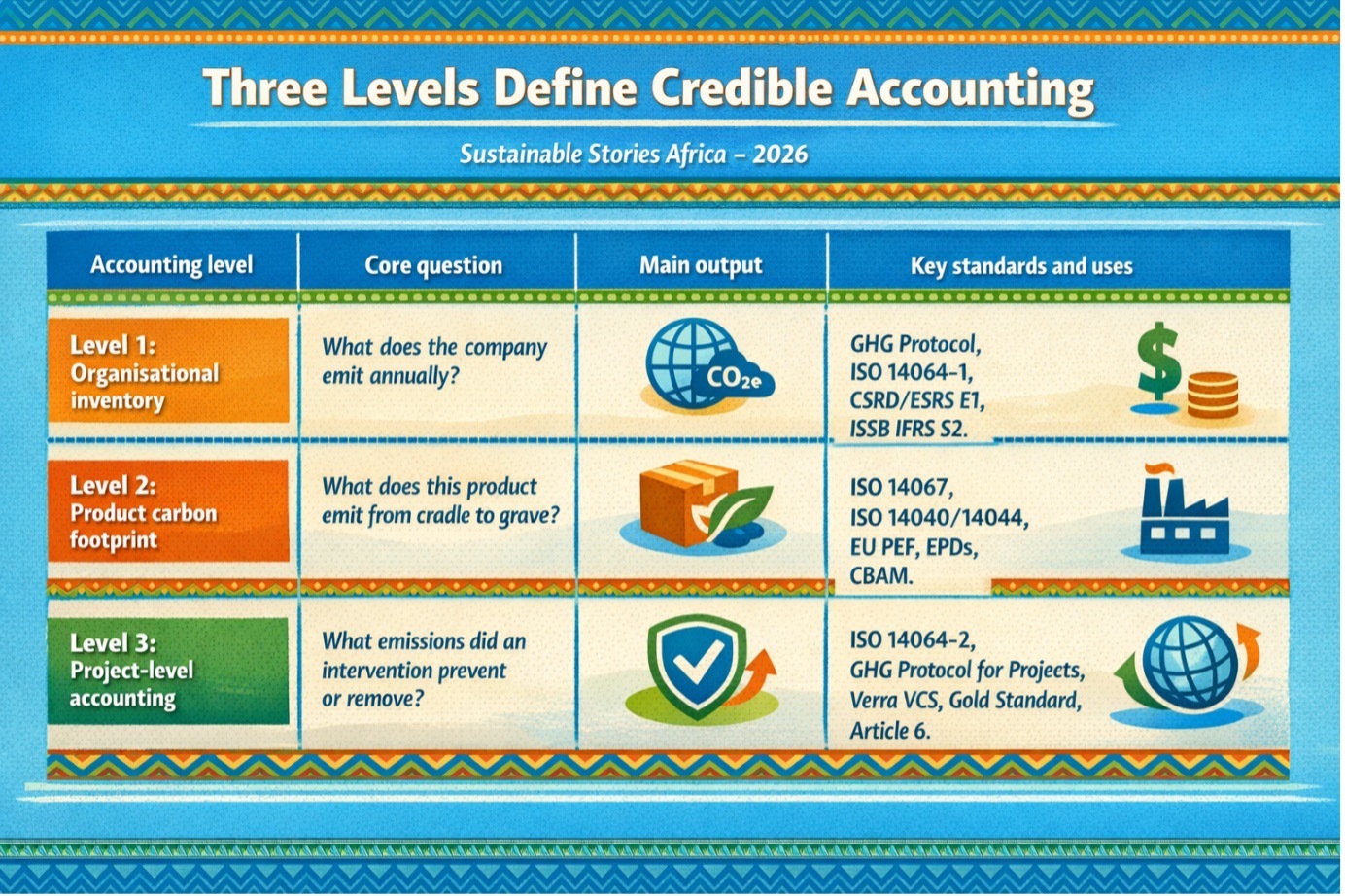

Three Levels Define Credible Accounting

The explainer’s strongest value is its layered structure. It shows that carbon accounting is not one thing. It is a system of measurement designed for different decisions.

- Level 1 sets the corporate baseline for climate action. Without an annual GHG inventory, companies cannot set reduction targets, track performance, or build a credible, science-based transition plan. The inventory is the essential first step and can be verified under ISO 14064-3 and disclosed through CDP, CSRD or GRI 305.

- Level 2 focuses on product emissions across four lifecycle stages: raw materials, manufacturing, use and end-of-life. For energy-using products, the use phase can often account for 80% of lifetime emissions.

That is a crucial insight for African manufacturers and exporters. The carbon footprint of a packaged food item, cement bag, aluminium product, textile, appliance or fertiliser product may not be determined only by factory emissions.

It may depend on inputs, processing energy, transport, consumer use and disposal.

Better Measurement Can Protect Markets

The opportunity is that better carbon accounting can protect companies from greenwashing risk while opening access to finance, procurement and export markets.

Product carbon footprinting is particularly important because it converts climate reporting from corporate averages into product-level evidence.

The explainer highlights the importance of the functional unit, which defines exactly what is being measured, for example, one kilogram of packaged pasta, one kilometre of passenger travel or one wash cycle.

It warns that two products with different functional units cannot be directly compared, and that this is where greenwashing can hide.

For African companies, this matters because international buyers are becoming more demanding.

A retailer or industrial buyer may no longer accept broad “low carbon” claims. They may ask for product-level data, verified methodologies, supplier traceability and proof that emissions factors are robust.

The explainer also links product accounting to external market rules and standards, including ISO 14067, ISO 14040/14044, the EU Product Environmental Footprint method, Environmental Product Declarations and the EU Carbon Border Adjustment Mechanism for embedded carbon in exports such as steel, cement and aluminium.

This creates a competitive divide. Companies that build measurement systems early can respond to buyers, financiers and regulators with confidence.

Those that delay may face higher compliance costs, weaker export positioning and greater suspicion around their climate claims.

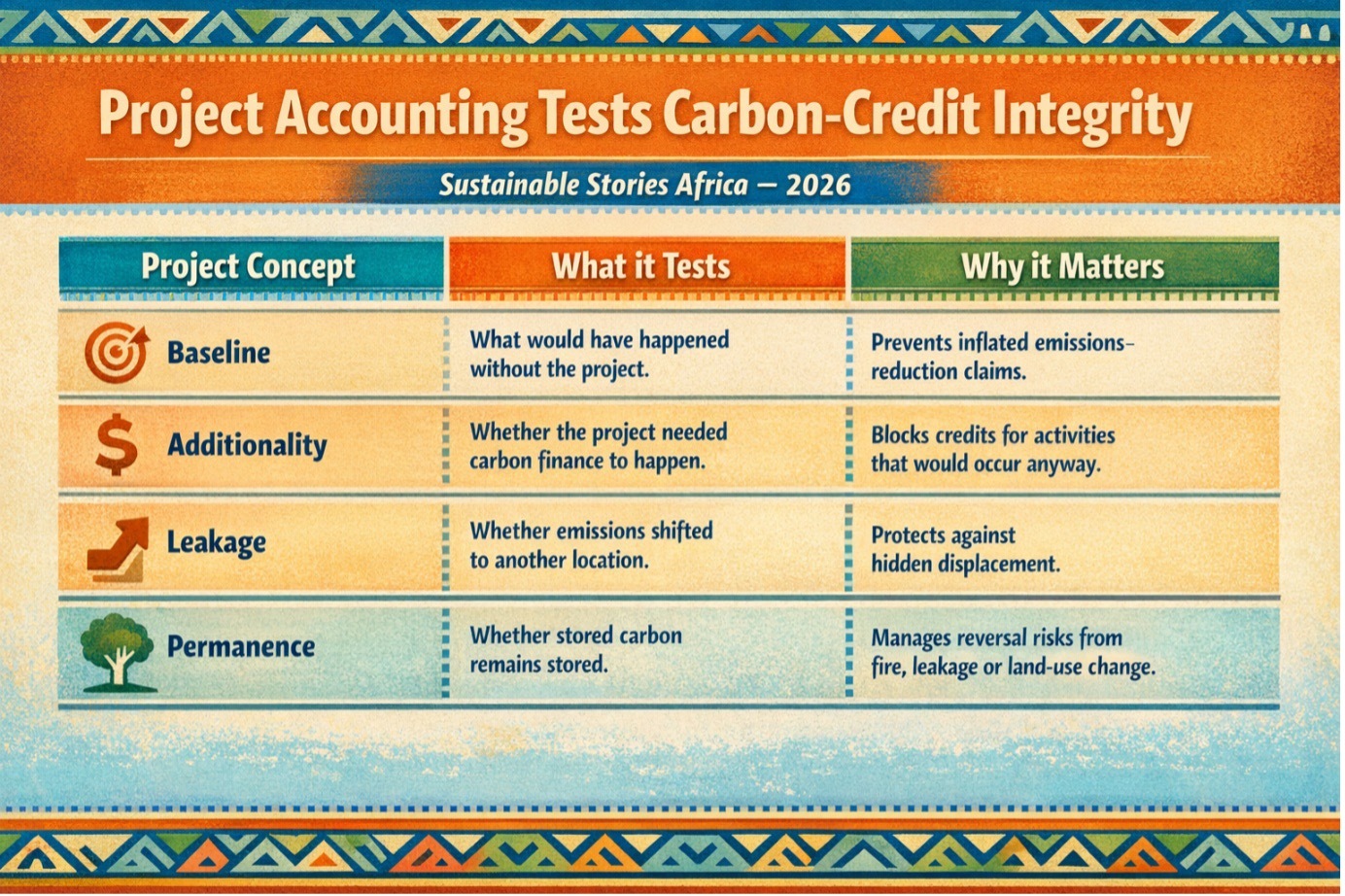

Project Accounting Tests Carbon-Credit Integrity

- The third level, project-level accounting, is where climate action meets carbon markets. It asks a different question: compared with what would have happened, how much greenhouse gas did a project prevent or remove?

The explainer identifies four concepts every project must address:

- Baseline

- Additionality

- Leakage

- Permanence.

Baseline is the counterfactual, what would have happened without the project.

Additionality asks whether the project would have happened anyway.

Leakage tests whether emissions were pushed elsewhere.

Permanence asks whether stored carbon will remain locked away.

These concepts are especially relevant for Africa’s carbon-market ambitions. Renewable energy, clean cooking, forest protection, mangrove restoration, regenerative agriculture and waste-to-energy projects can all generate climate value. But without rigorous baselines, monitoring and verification, they risk producing weak credits rather than real reductions.

The explainer warns that all credible net-zero strategies rely on high-quality project credits to address residual emissions that cannot yet be eliminated.

However, it also notes that credit quality has become a core sustainability skill, citing concerns about non-additional REDD+ credits.

The practical action is clear. Companies should first build organisational inventories, then assess product footprints where market access or product claims require it, and only then use project credits for residual emissions.

Carbon credits should not substitute for direct reductions. They should complement verified decarbonisation.

Path Forward – Measure First, Then Decarbonise

African companies should treat carbon accounting as business infrastructure: build full Scope 1, 2 and 3 inventories, measure product footprints, and apply rigorous project-accounting rules before making claims.

The next phase of ESG will reward companies that can prove emissions performance with reliable data. Carbon strategy must move from slogans to baselines, functional units, verification and credible reductions.