Singapore’s sustainability reporting model shows how ESG disclosure can move from glossy statements to board-level governance, measurable targets, and investor-ready data.

For African markets, the lesson is practical: sustainability reporting only builds trust when companies identify material risks, measure performance, explain shortfalls, and publish information that investors, regulators, workers, and communities can actually use.

Singapore’s Disclosure Lessons For African Markets

Singapore’s sustainability reporting framework is emerging as a useful reference point for African regulators and companies trying to make ESG disclosure more credible, comparable, and commercially relevant.

At the centre is the Singapore Exchange Singapore Sustainability Reporting Made Simple 4approach, which is a simple expectation: listed companies should explain the environmental, social, and governance issues that matter to their business, show how boards oversee them, set targets, report performance, and disclose the frameworks used.

The model is not just about compliance. It is about turning sustainability from a communications exercise into a governance and risk-management discipline.

For African economies seeking deeper capital markets, cheaper long-term finance, and stronger corporate accountability, the Singapore playbook offers a timely lesson: ESG reporting works best when it is clear, measurable, board-owned, and connected to real market risks.

Reporting Is Becoming Market Infrastructure

ESG reporting now sits beside financial reporting as a tool for understanding long-term value. The document explains that while financial statements look backwards, sustainability reporting helps investors assess future-facing risks and opportunities, including climate exposure, energy efficiency, workplace safety, governance quality, and stakeholder trust.

That distinction matters for Africa. Across the continent, companies face rising scrutiny from banks, development finance institutions, export partners, regulators, and communities. A manufacturer in Lagos, a mining company in Zambia, a bank in Nairobi, or an agribusiness in Côte d’Ivoire increasingly needs more than profit numbers to prove resilience.

Investors want to know whether power disruptions are being managed, whether emissions are measured, whether water risk affects operations, whether boards understand climate exposure, and whether anti-corruption systems are credible.

Singapore’s model shows that disclosure becomes useful when it answers those questions with structure, not slogans.

What Singapore Requires Companies To Disclose

Singapore’s framework, as simplified in the document, is anchored on SGX Listing Rules 711A and 711B.

- Rule 711A requires Mainboard issuers to prepare annual sustainability reports.

- Rule 711B sets out the core content: material ESG factors, climate-related disclosures, policies and practices, performance data, targets, reporting frameworks, and a board statement.

The framework also follows a “comply or explain” logic. Where a company does not report a required component, it should explain what it does instead and why.

That principle is important for African markets because it allows flexibility while still demanding accountability.

For African regulators, the lesson is not to copy the Singapore line for line. It is to build disclosure systems that are flexible enough to emphasise local realities but strict enough to prevent vague ESG claims.

Better Disclosure Can Unlock Capital

The opportunity is significant. Strong sustainability reporting can help African companies reduce the trust gap that often raises the cost of capital. When investors cannot compare ESG data, they price uncertainty.

When companies disclose consistent, assured, and decision-useful information, they make risk easier to evaluate.

Singapore’s guide emphasises materiality: companies should identify the ESG issues that could significantly affect business value, performance, and stakeholders.

It gives examples including energy use, greenhouse gas emissions, water management, health and safety, labour practices, anti-corruption, board composition, and ethics.

That is especially relevant in African markets where sustainability risks are often operational realities.

Diesel dependence affects margins. Flooding disrupts logistics. Poor safety systems increase liability. Weak governance raises financing risk.

Labour instability affects productivity. ESG reporting, done properly, becomes a map of business resilience.

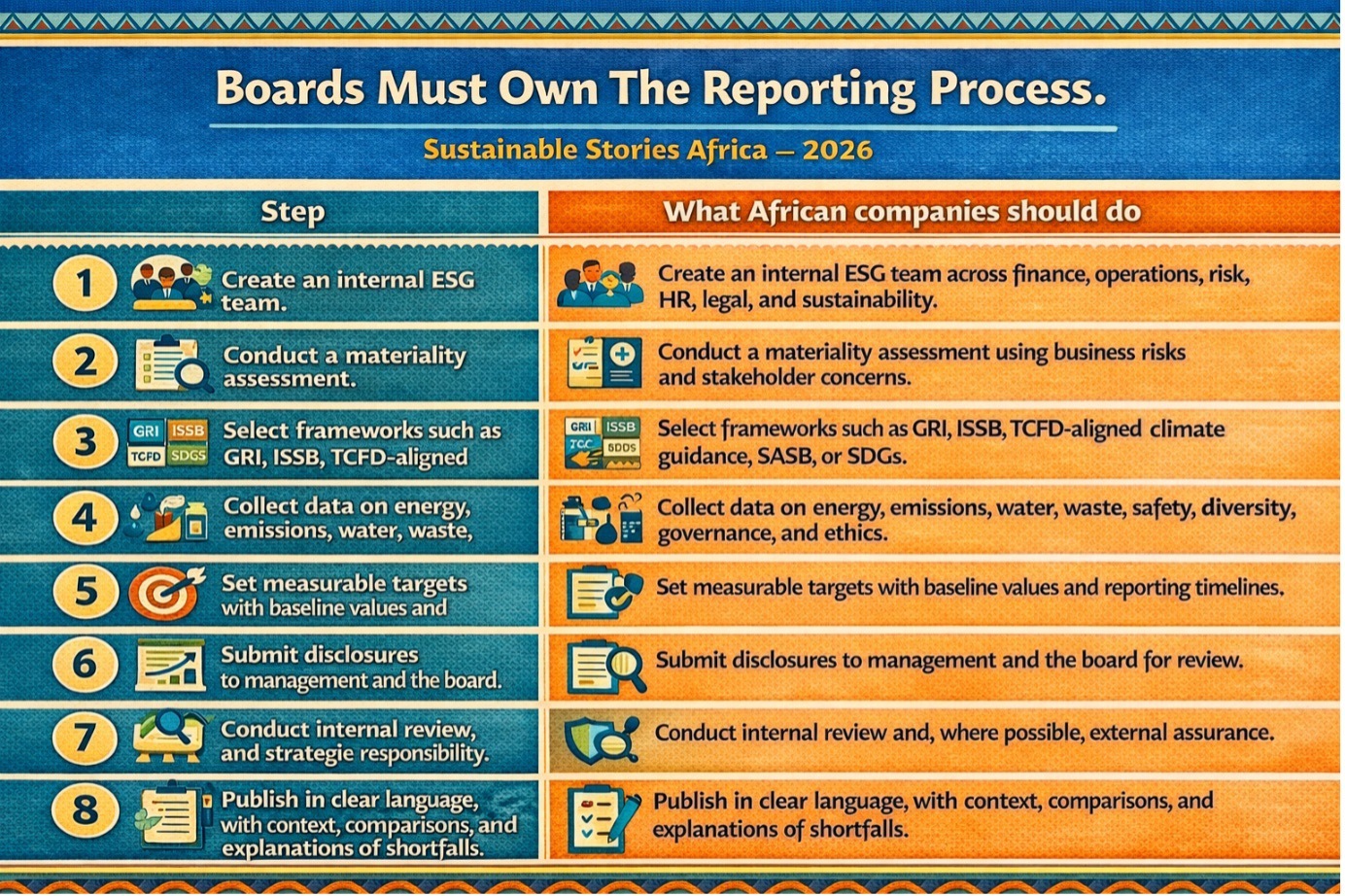

Boards Must Own The Reporting Process

The Singapore model places clear responsibility on boards. The document states that the board has ultimate responsibility for the sustainability report, must set ESG strategic objectives, approve material factors, and ensure governance structures cover sustainability issues.

This is a critical lesson for African companies. ESG cannot remain trapped inside communications, compliance, or corporate social responsibility departments. It needs board-level ownership, finance-team discipline, operational data, and internal controls.

A practical African reporting pathway would look like this:

The document’s step-by-step guide follows a similar sequence, beginning with assigning responsibility and identifying material ESG factors, then moving through targets, frameworks, data collection, drafting, review, assurance, publication, and follow-up.

The Metrics That Make ESG Credible

One of the most useful parts of the Singapore guide is its list of core ESG metrics.

- Environmental indicators include absolute greenhouse gas emissions, emissions intensity, total energy consumption, energy intensity, water consumption, and waste generated.

- Social indicators include gender diversity, age-based diversity, turnover, employee numbers, training hours, fatalities, high-consequence injuries, and recordable injuries.

- Governance indicators include board independence, women on the board, women in management, anti-corruption disclosures, anti-corruption training, certifications, framework alignment, and assurance status.

For Africa, these metrics are not abstract. They can help banks evaluate borrower transition risk. They can help regulators spot systemic governance weaknesses.

They can help exporters respond to supply-chain disclosure demands. They can help communities understand whether companies are managing environmental and social impacts transparently.

The key is comparability. Reporting one year of emissions without a baseline tells little. Reporting safety incidents without targets tells little.

Reporting “commitment to diversity” without board and workforce data tells little. Singapore’s model pushes companies toward measurable disclosure.

Simple Language Builds Public Trust

Another practical lesson is communication. The document warns against overly technical language, inconsistent data, unmeasurable targets, lack of prioritisation, missing context, skipped board statements, and delayed publication.

That warning speaks directly to African ESG reporting, where many sustainability reports still read like marketing brochures rather than accountability documents.

A strong report should say what improved, what failed, why it happened, and what management will do next.

- For a Nigerian manufacturer, that could mean disclosing electricity consumption, generator fuel use, emissions intensity, workplace injury rates, water withdrawal, waste diversion, supplier risks, and anti-corruption training.

- For a bank, it could mean climate risk exposure, financed emissions, board oversight, sustainable finance targets, and complaint handling.

- For a telecoms operator, it could mean energy mix, network resilience, digital inclusion, data privacy, and supplier labour standards.

Regulators Should Build Local Pathways

African regulators do not need to wait for perfect systems before acting. Singapore’s example suggests that markets can start with mandatory sustainability reporting, require board statements, recommend recognised frameworks, and gradually deepen climate disclosure, assurance, and sector-specific metrics.

A phased African model could begin with large, listed companies and financial institutions, then extend to high-impact sectors such as oil and gas, mining, cement, power, agriculture, telecoms, banking, and manufacturing. Smaller companies could use simplified templates, especially when supplying larger listed firms.

The most important principle is proportionality. A multinational bank and a mid-sized agribusiness should not face identical reporting burdens.

However, both should be able to explain their material risks, targets, governance systems, and performance data in a credible format.

Path Forward – From Compliance To Market Confidence

Africa’s ESG reporting agenda should move from broad declarations to board-owned, data-backed disclosure.

Singapore’s model shows that credibility comes from materiality, targets, performance data, internal review, assurance, and clear language.

The next step is local adaptation: regulators, exchanges, companies, and financiers should design practical templates that reflect African risks while aligning with global frameworks.

When done well, sustainability reporting creates a bridge between corporate integrity, investor confidence, and long-term development.