Eastern Africa’s energy transition is moving from ambition to delivery, with five national compacts setting out how Tanzania, Burundi, Comoros, Ethiopia and Kenya plan to expand power access, scale renewables and attract investment.

The question now is whether utilities, regulators and financiers can turn targets into bankable projects fast enough to meet 2030 access goals.

Energy Access Becomes Eastern Africa’s Test

Eastern Africa’s road to universal energy access is now being measured in megawatts, mini-grids, cleaner cooking fuels and utility balance sheets.

A new policy brief on Eastern Africa Compact Commitments examines how Tanzania, Burundi, Comoros, Ethiopia and Kenya are using the Mission 300 framework to set national roadmaps for expanding energy affordability, strengthening power systems, scaling renewables and mobilising private capital.

The brief follows the January 2025 Mission 300 Africa Energy Summit in Dar es Salaam, where leaders presented energy-access roadmaps backed by the African Development Bank and the World Bank.

- For citizens, the stakes are immediate: reliable electricity for schools, clinics, farms, factories and small businesses.

- For governments and investors, the test is harder: build cleaner systems, reform utilities, lower losses and attract more than $45 billion in identified investment needs without making power unaffordable for households.

Forty-Five Billion Dollars Now Defines Access

Eastern Africa's energy compacts are more than electricity expansion plans — they are simultaneous tests of governance, investment capacity and climate resilience.

Five country strategies assessed in the policy brief share a common ambition: universal or near-universal electricity access by 2030, expanded renewable energy shares, stronger regional power trade, adoption of wider clean cooking, and financially transparent utilities.

The Mission 300 framework organises these goals around five pillars: cost-efficient generation, regional integration, last-mile electrification, private investment and utility reform.

The region holds exceptional renewable potential; however, it faces dual pressure: industrialising economies demand reliable energy while vast rural populations remain difficult to connect.

Energy poverty continues to shape education, health, enterprise productivity and gender outcomes, making the transition both a development priority and a measurable ESG imperative.

The brief's Dar es Salaam summit image captures the political moment precisely; energy access has shifted from a narrow infrastructure file to a continental delivery agenda.

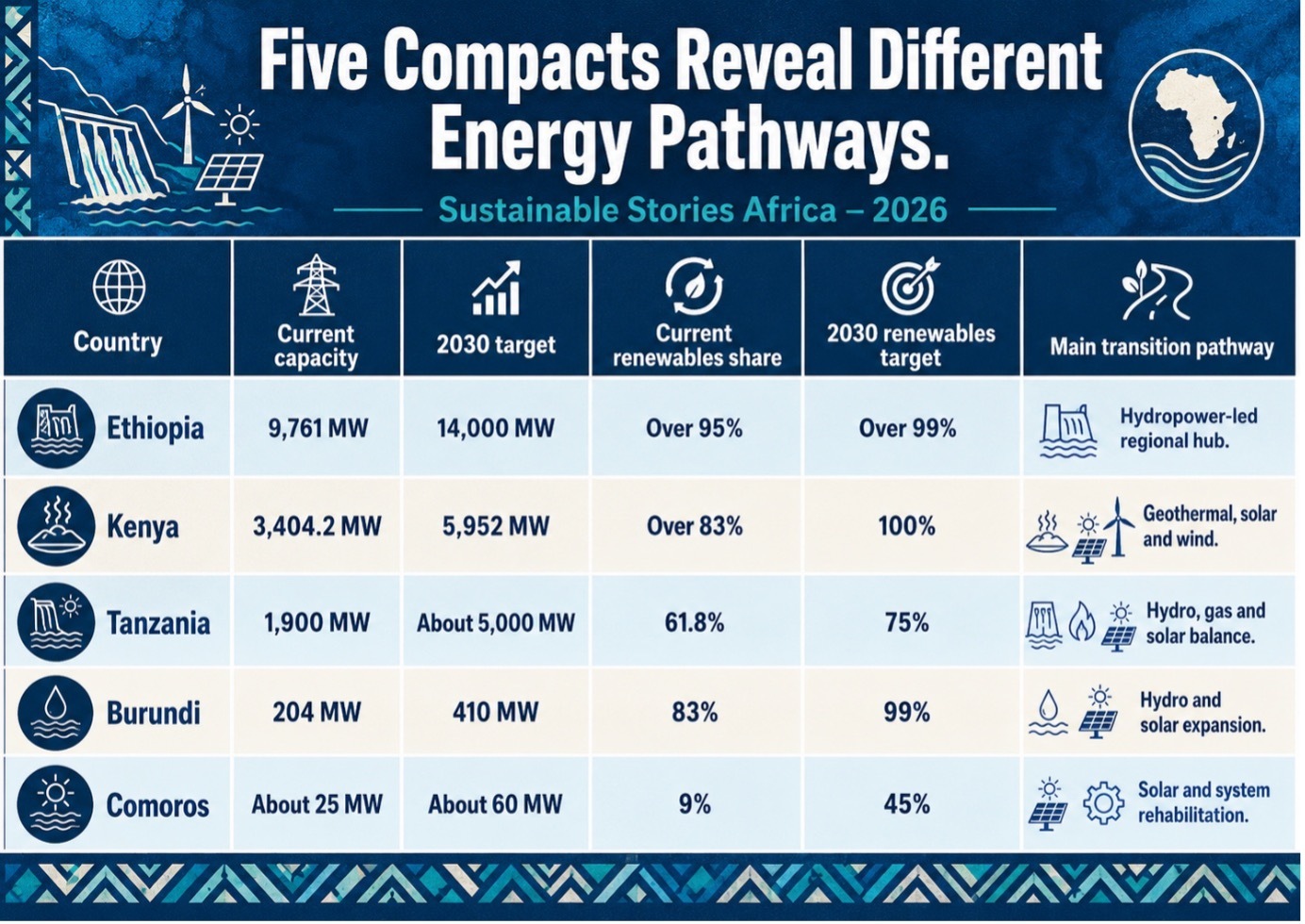

Five Compacts Reveal Different Energy Pathways

The five countries anchoring Eastern Africa's energy transition begin from starkly different starting points, and those differences define both the pace and the complexity of reform.

Kenya and Ethiopia are positioned as renewable champions: Kenya leverages geothermal resources while Ethiopia's hydropower capacity makes it a potential regional export hub.

Tanzania pursues a more gradual hybrid pathway, balancing natural gas with the expansion of solar energy.

Burundi and Comoros face a more foundational challenge, stabilising weak, loss-heavy systems before new capacity can meaningfully improve consumer access.

In Comoros, technical and commercial losses reach approximately 37%, and electricity costs exceed $0.30/kWh.

In Burundi, system losses of around 30% and REGIDESO's fragile finances make grid rehabilitation and utility reform preconditions, not afterthoughts.

At the regional level, the Eastern Africa Power Pool is advancing toward a competitive Day-Ahead Market serving 13 member countries and over 620 million people. AfDB-backed interconnectors, including the Ethiopia-Kenya HVDC line and the Kenya-Tanzania link, are building the physical infrastructure for cross-border trade.

However, unresolved barriers around harmonised grid codes, wheeling charges, off-taker creditworthiness and energy nationalism risk undermining the entire regional market architecture.

Clean Power Can Reach Last Mile

If implemented well, Eastern Africa's energy compacts offer a transformative shift, from grid expansion alone toward an integrated model encompassing mini-grids, solar home systems, clean cooking, regional trade and private investment.

Last-mile electrification anchors the agenda.

- Kenya targets 100% electricity access by 2030 through mini-grids and solar home systems.

- Tanzania targets 75% via rural densification and private mini-grid rollout.

- Ethiopia aims for 75%, with 35% of its population served off-grid.

- Burundi targets 70%, including 300 mini-grid sites.

- Comoros pursues 100% through hybridised island grids.

Clean cooking is the second critical frontier. Over 80% of people across these countries still rely on firewood or charcoal, driving household air pollution, deforestation and climate vulnerability.

The compacts now include quantified targets:

- Kenya aims for 100% clean cooking access by 2030 from a baseline of 34.4%.

- Tanzania targets 75% from 6.9%.

- Ethiopia moves from 8% to 57.7%

- Burundi from below 5% to 40%

- Comoros from 0.5% to 30%.

Technologies, such as LPG, bioethanol, biogas, improved stoves, briquettes and electric cooking, vary by country but all require financing, safety regulation and consumer trust to deliver real household gains.

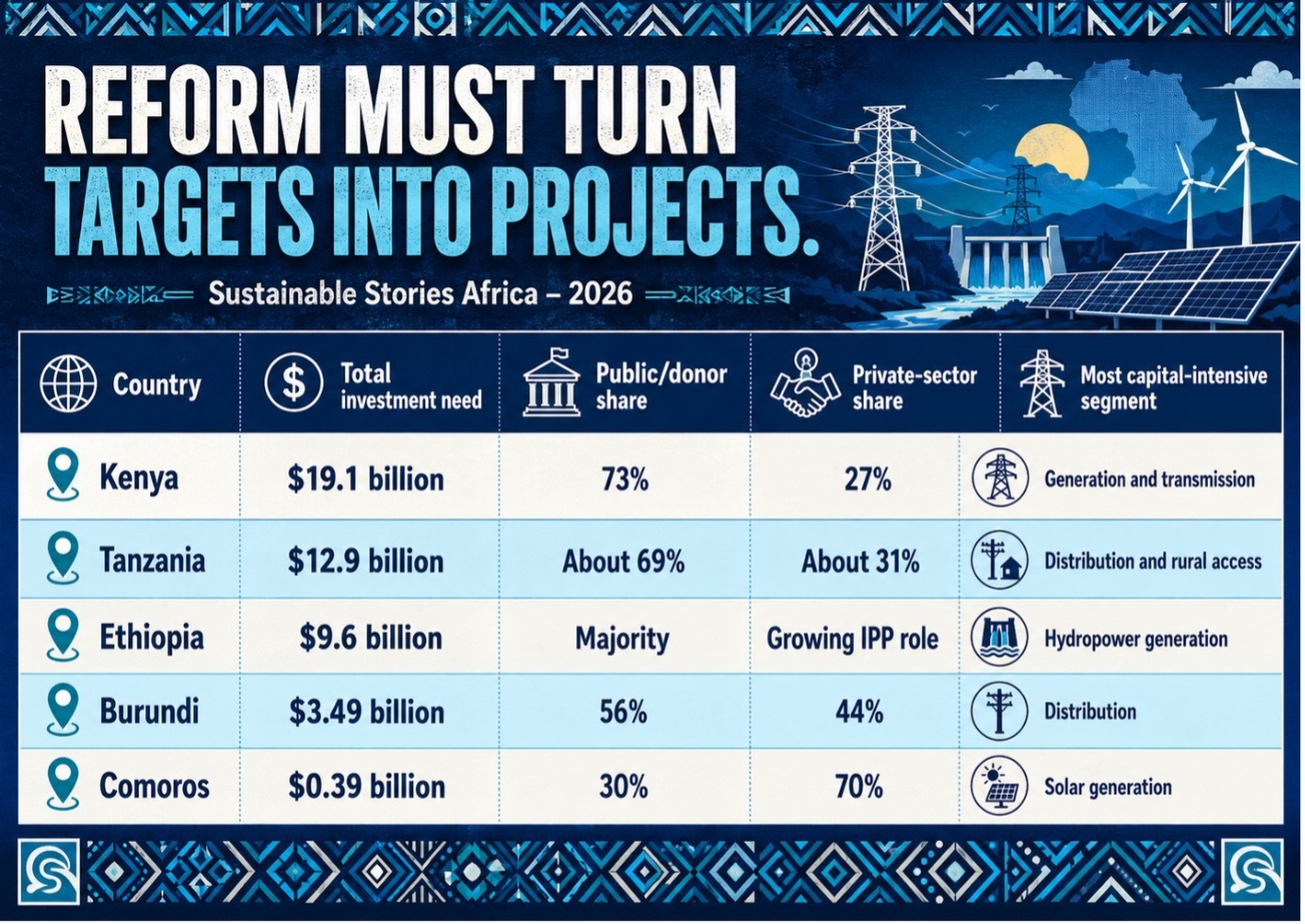

Reform Must Turn Targets Into Projects

The financing challenge is large and uneven. The five compacts identify more than $45 billion in investment needs, with private-sector shares ranging from 27% in Kenya to 70% in Comoros.

That wide range reflects differences in market maturity, creditworthiness and regulatory credibility.

Private capital will not arrive because targets are ambitious. It will respond to bankable power purchase agreements, transparent licensing, cost-reflective tariffs, credible regulators, foreign-exchange risk mitigation and utilities that can pay their bills.

Kenya has the most advanced private-sector strategy, including competitive procurement, standardised PPAs, updates of mini-grid regulation, green bonds, results-based financing and carbon-market development.

The lifting of Kenya’s PPA moratorium in November 2024 reopened space for Kenya Power to procure 1,112 MW from independent power producers through more transparent competitive processes.

Tanzania is focusing on procurement and PPP frameworks, including renewable-energy IPP procurement, revised small power producer tariffs and updated net-metering rules.

Ethiopia is pursuing private participation across generation, transmission, distribution, off-grid electrification and clean cooking, backed by blended finance and guarantees.

Burundi and Comoros remain earlier-stage markets, where utility weakness and regulatory reform will determine whether private investment can be mobilised at all.

Utility reform is therefore the hinge. The brief warns that without financially viable and creditworthy utilities, countries will struggle to establish bankable PPAs, attract private capital or integrate credibly into regional power markets.

That makes transparent financial management, audited accounts, loss reduction, tariff reform and performance-improvement plans central to the Mission 300 delivery agenda.

Path Forward – Deliver Energy Access Through Reform

Eastern Africa’s compacts should now move from ambition to sequencing: fix weak utilities, reduce losses, expand mini-grids, scale clean cooking and make regional power trade commercially credible.

AfDB’s role is catalytic. By linking sovereign lending, private-sector finance, technical assistance and regional coordination, it can help countries turn compact commitments into investable, context-specific delivery plans that advance access, climate resilience and inclusive growth.