A new World Economic Forum report argues that nature finance has moved beyond conservation rhetoric into mainstream commercial territory, identifying more than 50 investible opportunities across 13 sectors that can generate returns while reducing pressure on ecosystems.

From precision agriculture to battery recycling, the message is clear: resilience and profitability no longer sit on opposite sides of the ledger.

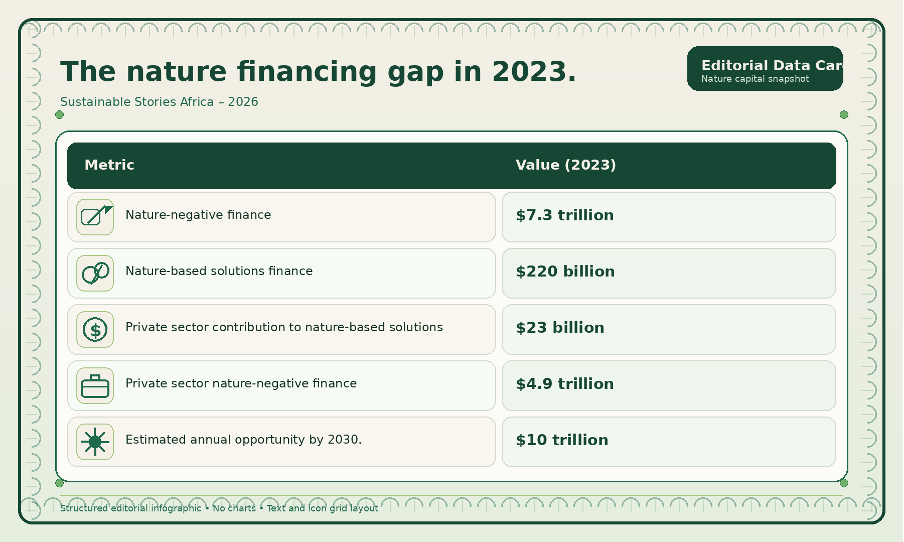

The deeper problem is capital allocation. In 2023, $7.3 trillion still flowed into nature-negative activities, while only $220 billion went into nature-based solutions.

That gap is not just an environmental failure; it is also a market distortion that leaves proven, scalable opportunities underfunded.

The Market Case for Nature

Nature finance is no longer confined to conservation grants, philanthropic pledges or biodiversity rhetoric.

The World Economic Forum argues that more than 50 investible opportunities across 13 sectors are already capable of generating revenue, cutting costs and easing pressure on land, water, materials and ecosystems.

The central question is no longer whether nature matters to business. It is whether capital will move quickly enough to back business models, technologies and systems that are already proving resilience and returns can advance together.

For African and other emerging markets, that matters because the opportunity lies in sectors that shape daily development choices: food production, mineral extraction, urban construction, water systems and waste recovery.

The issue is not only ecosystem protection. It is about redesigning real-economy value chains, so growth becomes less extractive, more resilient and more investible.

When Nature Becomes an Investable Asset

For years, nature finance sat at the margins, seen more as moral duty than economic opportunity.

The latest Forum analysis reframes that case, identifying more than 50 investible openings across major sectors.

However, the gap is wide: in 2023, $7.3 trillion was invested in nature-harming activities, versus $220 billion for nature-based solutions.

With private capital contributing only $23 billion, redirecting even part of that flow could make nature-positive investment a credible engine of growth.

The nature financing gap in 2023

Metric | Value (2023) |

|---|---|

Nature-negative finance | $7.3 trillion |

Nature-based solutions finance | $220 billion |

Private sector contribution to nature-based solutions | $23 billion |

Private sector nature-negative finance | $4.9 trillion |

Estimated annual opportunity by 2030 | $10 trillion |

The report makes a stronger commercial case for nature-positive action, framing it not as theory but as practical business activity already visible across supply chains, from precision agriculture and sustainable fertilisers to industrial water management, battery recycling and data-centre heat re-use.

It argues the opportunity is large: nature-positive transitions could unlock $10.1 trillion in annual revenues and savings by 2030, while the green economy reached nearly $8 trillion in listed equity value in 2024.

From 250 Activities to 50 Investment-Ready Opportunities

The shortlist was built on measurable business logic, not vague ambition. The Forum says it reviewed about 250 activities and screened them against three tests: value-chain relevance, positive nature impact across priority drivers, and stronger business financials through higher revenue, lower operating costs or reduced capital expenditure.

That process produced more than 50 practical opportunities across 13 sectors, including agroforestry, alternative proteins, innovative irrigation, sustainable seafood, agrivoltaics, battery recycling, e-waste recycling and wastewater treatment technologies. Across the portfolio, pollution, land use, resource use and freshwater outcomes feature most strongly.

The commercial case is equally broad. Some openings create new revenue, others cut operating costs, and some reduce capital intensity. That breadth gives boards and financiers a clearer way to assess nature opportunities through familiar financial lenses.

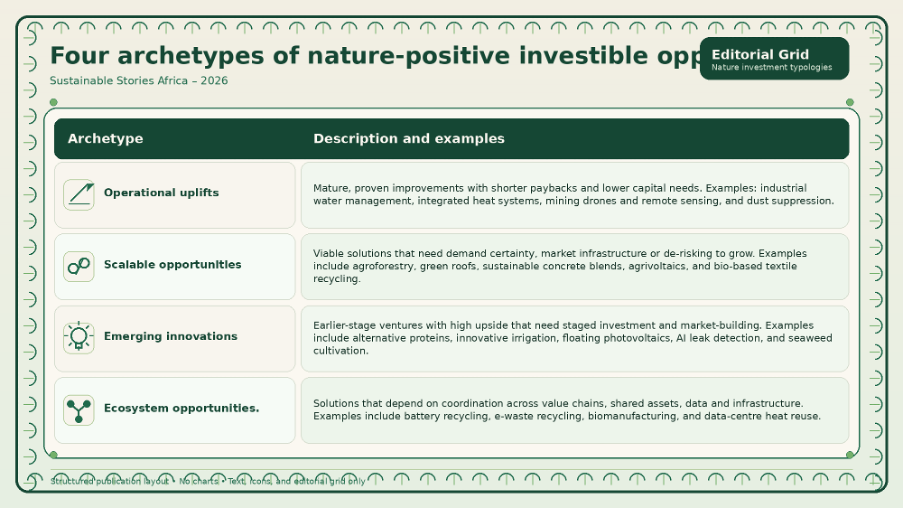

Four archetypes of nature-positive investible opportunities

Archetype | Description and examples |

|---|---|

Operational uplifts | Mature, proven improvements with shorter paybacks and lower capital needs. Examples: industrial water management, integrated heat systems, mining drones and remote sensing, and dust suppression. |

Scalable opportunities | Viable solutions that need demand certainty, market infrastructure or de-risking to grow. Examples include agroforestry, green roofs, sustainable concrete blends, agrivoltaics, and bio-based textile recycling. |

Emerging innovations | Earlier-stage ventures with high upside that need staged investment and market-building. Examples include alternative proteins, innovative irrigation, floating photovoltaics, AI leak detection, and seaweed cultivation. |

Ecosystem opportunities | Solutions that depend on coordination across value chains, shared assets, data and infrastructure. Examples include battery recycling, e-waste recycling, biomanufacturing, and data-centre heat reuse. |

The framework helps explain why some nature solutions scale faster than others. Simpler operational fixes can move quickly, while capital-intensive options often depend on stronger infrastructure, contracts, regulation and coordination.

One sign of progress is ING’s $700 million sustainability-linked facility for Sucafina, which is linked to traceability, deforestation monitoring, certified sourcing and regenerative agriculture.

Desire: What Makes the Business Case Stick

What makes the report persuasive is that it frames nature not as a niche asset class, but as a pathway to stronger operating models. Industrial water management cuts freshwater use and treatment costs, while integrated heat systems improve efficiency and reduce exposure to fuel-price volatility.

In agriculture, smarter irrigation can protect scarce water resources, lift yields and reduce wasted inputs, especially in water-stressed markets.

In construction, sustainable cement and concrete blends can lower dependence on virgin materials, divert waste from landfill and reduce emissions.

Green roofs add rainwater management, urban cooling and biodiversity benefits. For African markets, these blended returns matter because they align directly with food security, jobs, infrastructure quality, industrial resilience and resource efficiency.

The cost of delay is also rising. Nature loss is already showing up through volatile input costs, operational disruption, tighter permitting, legal risk and reputational pressure, making inaction an accumulating commercial liability.

Five Pathways for Financial Institutions

The Forum’s recommendations are pragmatic.

- First, it calls on financial institutions to build institutional “nature fluency”, using existing net-zero governance, risk tools and finance frameworks as entry points for bringing nature into mainstream decision-making.

- Second, it urges banks and investors to use transition-plan discussions with clients to identify nature-positive opportunities hidden within everyday capital expenditure and supply-chain choices.

- Third, the report says institutions should work with data already available inside operations, supply chains and public sources, even when the evidence is still directional.

- Fourth, it argues that many opportunities can already be financed through familiar instruments such as corporate loans, project finance and sustainability-linked products; however, more complex cases may need blended finance, guarantees, insurance or performance-based support.

- Fifth, it calls for coalitions that bring together corporates, financiers, public institutions and philanthropy, especially where infrastructure, shared systems or market-building are required.

Path Forward

Nature-positive investment will scale when markets stop treating it as a specialist sustainability theme and start treating it as part of core economic infrastructure.

The report’s 50-plus opportunities suggest that the commercial case already exists across sectors, technologies and risk profiles.

The real test now is execution: redirecting capital, standardising metrics, de-risking early markets and building the coalitions needed to move pilots into mainstream business systems.

If that happens, nature finance will no longer sit at the margins of development. It will help determine how development itself is financed.