Europe’s new CSRD rules are reshaping how companies report sustainability.

Early disclosures show longer, more standardised, and audit-driven reporting practices emerging.

The shift could redefine global ESG standards and corporate accountability frameworks.

From Voluntary Narratives to Regulated Disclosure

Sustainability reporting in Europe is undergoing a structural transformation, and the era of loosely defined ESG narratives is closing rapidly.

Early reports under the Corporate Sustainability Reporting Directive (CSRD) reveal a clear trend: disclosures are becoming more standardised, significantly longer, and increasingly subject to audit-level scrutiny.

For companies, this marks a fundamental shift. Sustainability is no longer a communications exercise; it is becoming a regulated, verifiable component of corporate reporting, on par with financial statements.

What Early CSRD Reports Reveal

The first wave of CSRD-aligned reports offers insight into how companies are adapting to one of the most ambitious sustainability disclosure frameworks globally.

Three key trends are emerging:

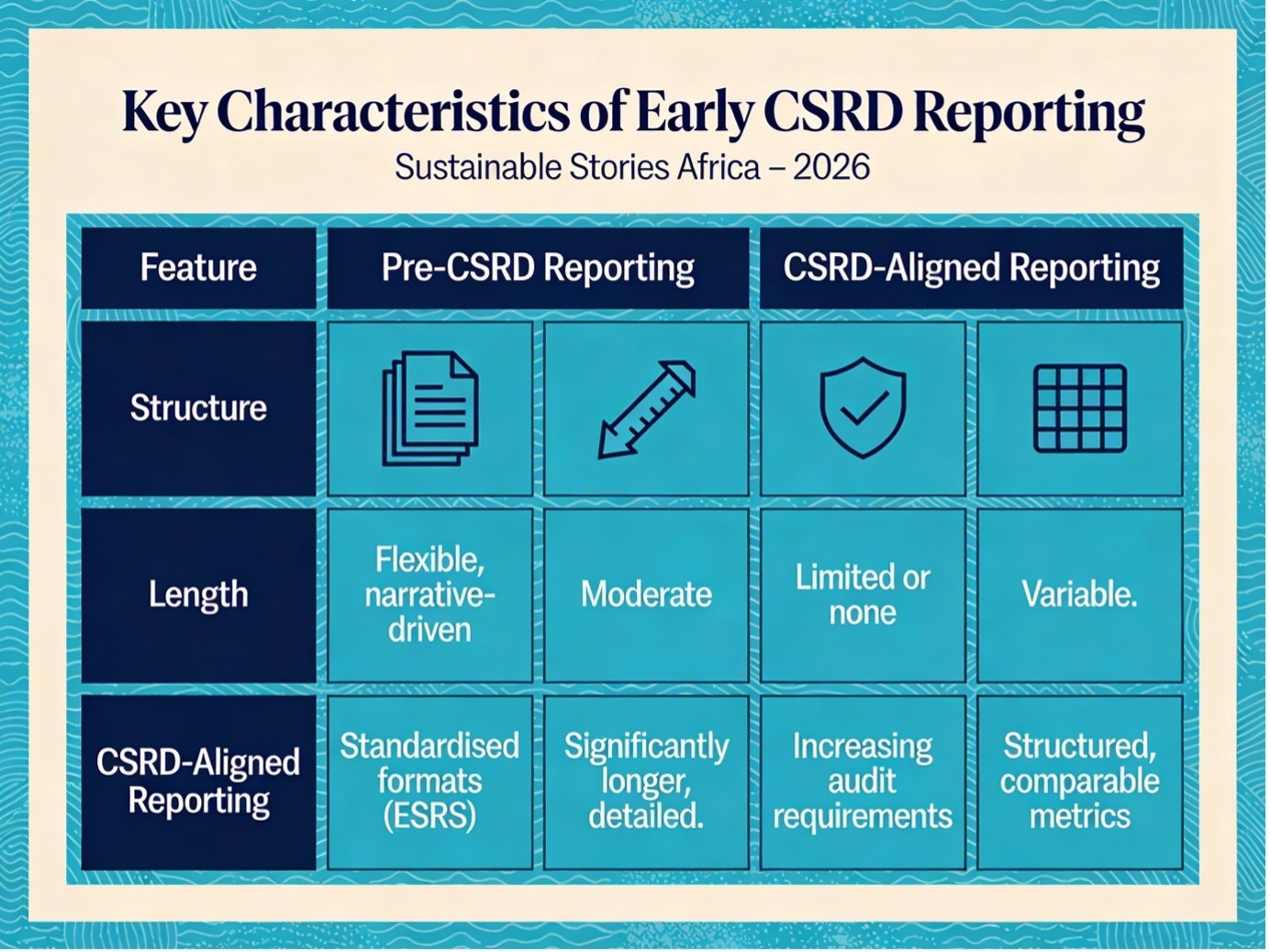

Key Characteristics of Early CSRD Reporting

Feature | Pre-CSRD Reporting | CSRD-Aligned Reporting |

|---|---|---|

Structure | Flexible, narrative-driven | Standardised formats (ESRS) |

Length | Moderate | Significantly longer, detailed |

Assurance | Limited or none | Increasing audit requirements |

Data Quality | Variable | Structured, comparable metrics |

Companies are now required to align disclosures with the European Sustainability Reporting Standards (ESRS), which demand granular data across environmental, social, and governance dimensions.

This includes:

- Detailed climate risk and transition plans

- Scope 1, 2, and 3 emissions disclosures

- Supply chain and human rights reporting

- Governance and risk management frameworks

The result is a shift toward data-heavy, compliance-driven reporting, which extends far beyond traditional annual sustainability reports.

What Standardisation Could Unlock

While the transition is resource-intensive, the long-term benefits are significant.

Standardised and audited ESG reporting has the potential to:

- Improve comparability – Investors can assess companies on a like-for-like basis

- Enhance credibility – Verified data reduces greenwashing risks

- Unlock capital flows – Strong ESG performance becomes more investable

- Strengthen risk management – Companies gain clearer visibility into sustainability risks

For global markets, including Africa, CSRD could serve as a blueprint for future disclosure regimes.

African corporates, particularly those seeking European investment or operating within EU value chains, may increasingly need to align with these standards, accelerating the adoption of structured ESG frameworks across the continent.

Preparing for a New Reporting Reality

The implications of CSRD extend far beyond Europe.

Companies, regulators, and investors must now adapt to a world where ESG disclosure is:

- Mandatory, not optional

- Standardised, not fragmented

- Auditable, not aspirational

Strategic Priorities for Stakeholders

Stakeholder | Required Action |

|---|---|

Corporates | Invest in data systems, governance, and reporting capabilities |

Regulators | Align local frameworks with global standards |

Investors | Integrate structured ESG data into decision-making |

Auditors | Expand capacity for sustainability assurance |

For African markets, the urgency is growing. Companies that fail to align risk will be excluded from global capital flows, while those that adapt early could gain a competitive advantage.

PATH FORWARD – Standardisation, Assurance: Define Future ESG Reporting

CSRD is setting a new global benchmark for sustainability disclosure, emphasising standardisation, data integrity, and auditability. Companies must adapt quickly to remain competitive.

As ESG reporting evolves into a core financial discipline, aligning with global standards will be critical, ensuring transparency, attracting capital, and driving sustainable growth across both European and emerging markets.

Culled From: Early CSRD Reports Show EU Sustainability Disclosure Becoming More Standardised, Longer and More Audit-Driven