A just transition is becoming the defining test of credibility for global finance as banks and insurers wrestle with the social consequences of climate action. From worker displacement to community resilience, financial institutions now stand at the centre of the world's sustainability transformation.

This feature explores how new frameworks, governance models, and financing tools are shaping a transition that protects people while decarbonising economies.

Finance Reimagined Through People-Centred Transition

The world's race to net zero has reached an uncomfortable truth: climate action fails when people are left behind. As extreme weather intensifies and economies shift away from fossil fuels, millions of workers, communities, and vulnerable groups face unprecedented risks. The ILO–UNEP FI Just Transition Finance report makes the case clearer than ever: finance must move beyond emissions metrics and confront the human realities of transition.

Banks and insurers are no longer passive actors in this transformation. They are becoming architects of a new financial paradigm that must integrate social protections, labour rights, community resilience, and climate science into the heart of lending and underwriting decisions.

From underwriting climate-resilient homes in flood-prone regions to financing the retraining of coal workers, financial institutions now shape outcomes far beyond balance sheets.

This opinion article explores the new frameworks, governance models, and tailored financial products shaping just transition finance. Blending narrative insight with rigorous analysis, it highlights how banks and insurers can drive climate progress while making sure no one is left behind.

Human Centred Finance in a Warming World

In every region today, the costs of an unjust climate transition are becoming clearer. Coal-dependent towns are facing economic collapse, informal workers are excluded from green jobs, Indigenous communities are displaced by clean-energy projects, and women are burdened by climate-driven care responsibilities. These are all reminders that climate action is not only about carbon; it is about people.

The ILO–UNEP FI report warns that without embedding social safeguards into financial decision-making, the world risks a "transition backlash", which is capable of slowing climate action and destabilising economies. Banks and insurers are now at a crossroads to either finance deep decarbonisation that protects livelihoods or finance a transition that fractures societies.

The Anatomy of Just Transition Finance

Just transition finance is not simply "social ESG." It is a structured approach that links climate mitigation, climate adaptation and social justice into a unified financial lens.

The report outlines three pillars for integrating just transition across banking and insurance activities: foundations, governance, and implementation.

The Three Pillars of Just Transition Finance

| Pillar | Core Focus | Examples from Banks & Insurers |

|---|---|---|

| Foundations | Strategy, commitments, internal awareness | Just transition pledges, staff training, dual environmental-social risk frameworks |

| Governance | Oversight, cross-functional decision-making | Sustainability committees, human-rights due diligence units |

| Implementation | Lending, underwriting, products | Place-based financing, inclusive insurance, and worker-support credit lines |

Why This Matters for Finance

Banks face three converging pressures:

- Regulatory: rising due diligence laws, disclosure frameworks, and human-rights requirements.

- Investor-driven: CA100+, IIGCC, and WBA now assess just transition performance.

- Economic: unmanaged transition risks increase non-performing loans, stranded assets, and social unrest.

Insurers face parallel pressures:

- Climate-related insured losses are rising sharply.

- Protection gaps widen as premiums increase.

- Vulnerable populations risk becoming uninsurable.

This convergence makes social equity a financial stability issue.

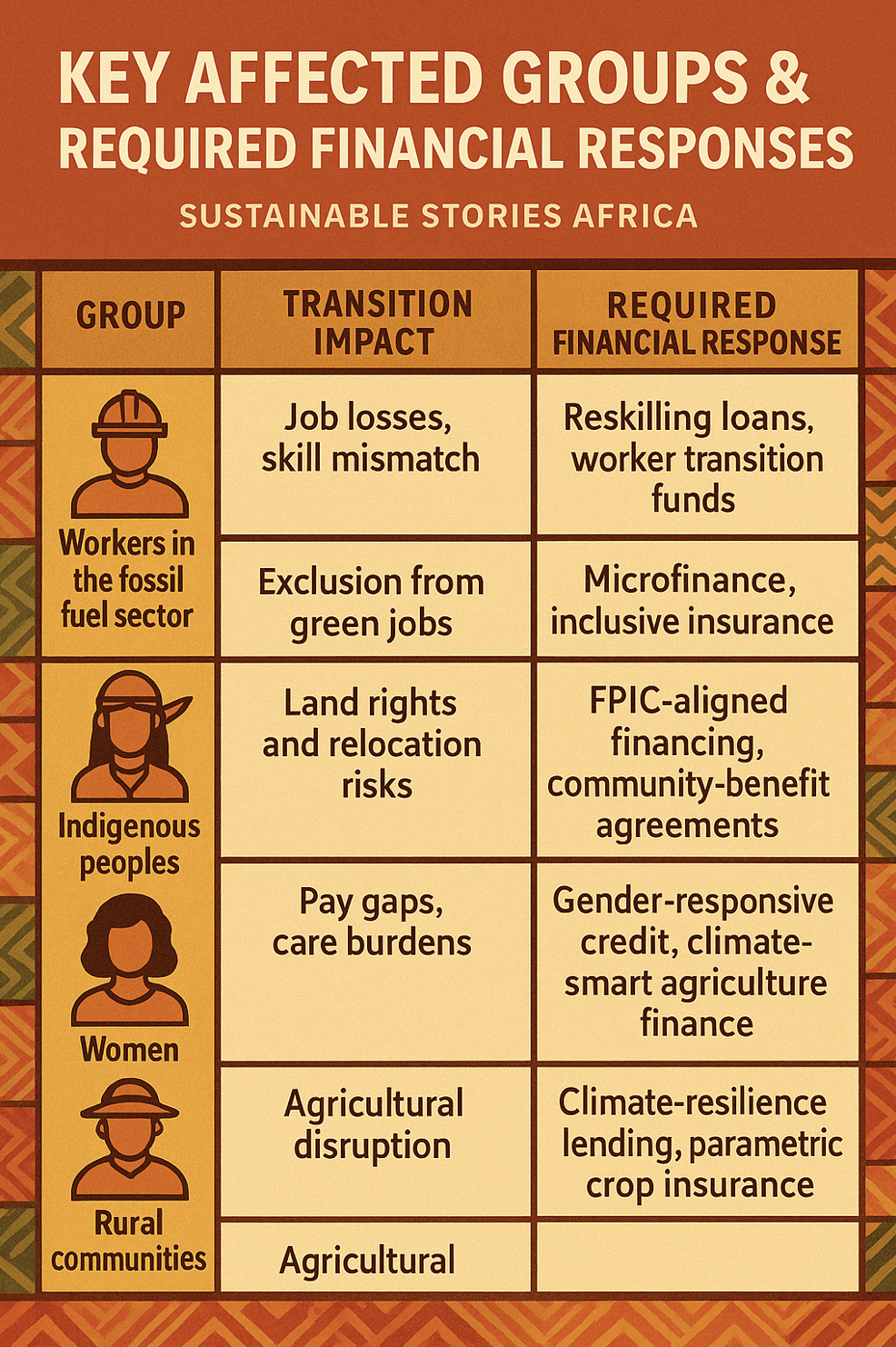

Who Is Affected? A People-Centred Transition Map

The report outlines how workers, consumers, communities, Indigenous people, migrants, rural sectors, women, and persons with disabilities experience the transition differently. These differences must inform financing and underwriting decisions.

Key Affected Groups & Required Financial Responses

| Group | Transition Impact | Required Financial Response |

|---|---|---|

| Workers in the fossil fuel sector | Job losses, skill mismatch | Reskilling loans, worker transition funds |

| Informal workers | Exclusion from green jobs | Microfinance, inclusive insurance |

| Indigenous peoples | Land rights and relocation risks | FPIC-aligned financing, community-benefit agreements |

| Women | Pay gaps, care burdens | Gender-responsive credit, climate-smart agriculture finance |

| Rural communities | Agricultural disruption | Climate-resilience lending, parametric crop insurance |

Sector Dynamics: Where Finance Must Intervene

Energy (Oil, Gas, Coal)

- High job displacement risks

- Community-wide income shocks

- Need for retraining, environmental remediation

Agriculture

- High informality

- Food security risks

- Gendered impacts on smallholder farmers

Mining

- Critical minerals create new risks: child labour, land conflicts

Transport

- Gains in electrification but losses in ICE supply chains

Construction

- Hazardous work conditions, informal labour, opportunity for green retrofits

Sectoral Transition Impacts

Energy (O&G) → Job losses | Agriculture → Productivity risk | Mining → Rights + land conflict | Transport → Workforce reskilling | Construction → OSH + informality risks

What a Just Transition Enables

When designed well, just transition finance delivers environmental gains, stimulates economic growth, and unlocks social benefits.

- Economic Transformation with Stability – Banks can reduce credit risk by supporting transition-ready clients; insurers can reduce long-term liabilities through proactive risk reduction.

- Social Cohesion – Communities supported through transition are more likely to back climate policies.

- New Markets – Financial inclusion, climate-resilient infrastructure, and green technology create new client bases.

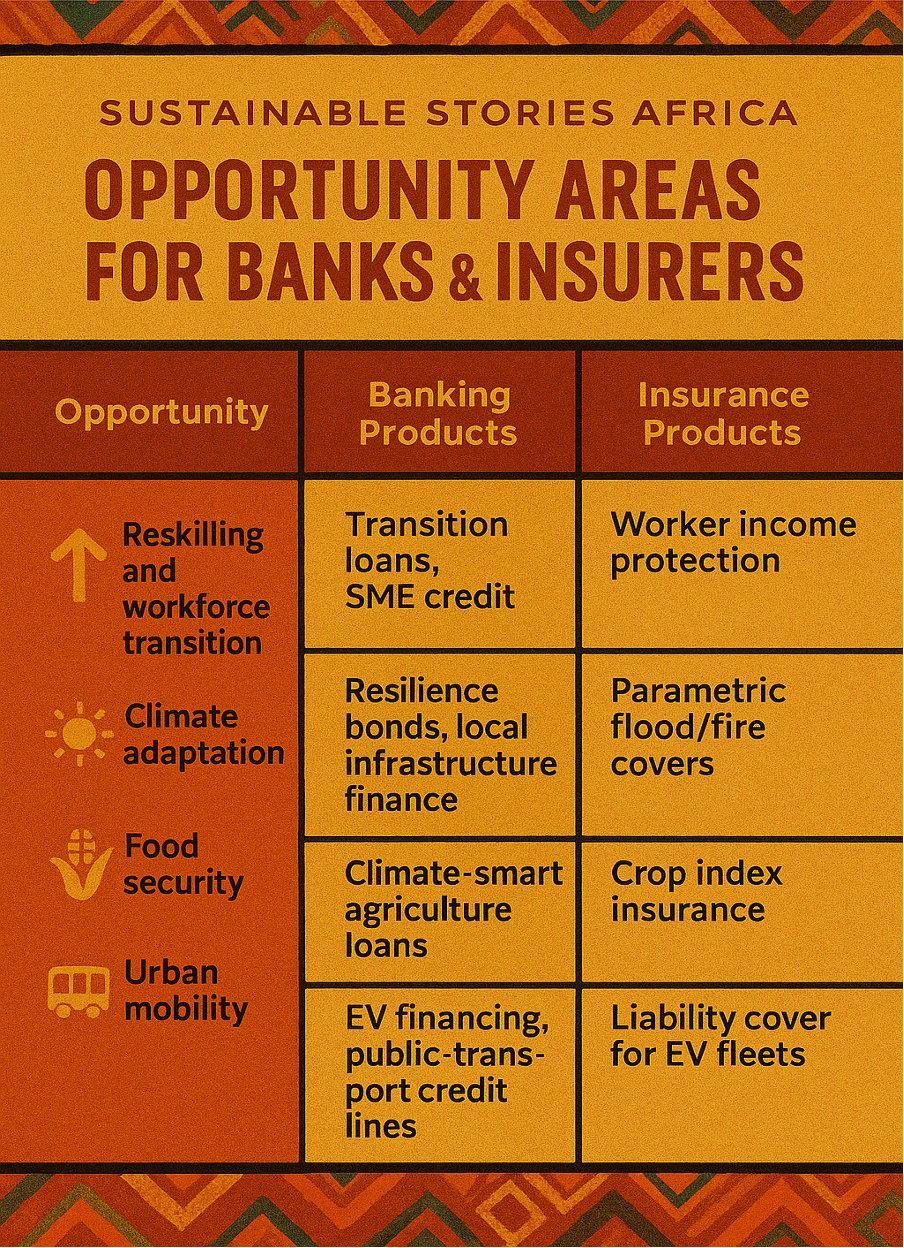

Opportunity Areas for Banks & Insurers

| Opportunity | Banking Products | Insurance Products |

|---|---|---|

| Reskilling and workforce transition | Transition loans, SME credit | Worker income protection |

| Climate adaptation | Resilience bonds, local infrastructure finance | Parametric flood/fire covers |

| Food security | Climate-smart agriculture loans | Crop index insurance |

| Urban mobility | EV financing, public-transport credit lines | Liability cover for EV fleets |

The prize is multi-trillion-dollar: 70% of net-zero investment needs could come from private finance.

How Banks and Insurers Operationalise Just Transition

Commitment and Leadership

- Board-level just transition statements

- Integration into net-zero plans

- Executive KPIs linked to social outcomes

Understanding the Landscape

- Banks map stakeholder risks (workers, communities, consumers). Insurers map protection gaps and vulnerable geographies.

Putting People at the Centre

- Social dialogue with unions, communities, Indigenous leaders

- FPIC for land-related projects

- Worker displacement analysis

Implementation in Banking

- Align credit decisions with both climate and social safeguards

- Develop products addressing community needs

- Expand financial inclusion for vulnerable groups

Three Lenses for Lending

- Environmental: emissions trajectory

- Social: worker/community impacts

- Economic: long-term viability

Implementation in Insurance

- Underwriting policies integrate climate + social risks

- Protection products tailored to low-income and affected groups

- Risk-prevention services bundled with insurance

Just Transition Underwriting Approach

- Assess → climate + social risk

- Price → equitable premiums

- Protect → vulnerable groups

- Prevent → risk-reduction incentives

Engagement & Partnerships

- Partnering with public finance for blended solutions

- Working with civil society on rights-based frameworks

- Supporting national just transition plans

Measurement & Reporting - Banks and insurers must disclose:

- social risks

- transition impacts

- workforce outcomes

- community effects

- protection-gap metrics

This is the transparency that builds trust.

PATH FORWARD - Financing Fair Futures Through Climate Equity

The next frontier of climate finance demands that banks and insurers embed equity into every lending, underwriting, and investment decision. Institutions must advance just transition frameworks, scale inclusive products, and deepen engagement with affected stakeholders. The priority is to deliver climate action without deepening inequality.

A coordinated financial system—rooted in resilience, human rights, and community participation—can turn climate risks into opportunities for shared prosperity.