Amazon, Microsoft and Google are facing fresh investor pressure over the water and power demands of their expanding data-centre footprints.

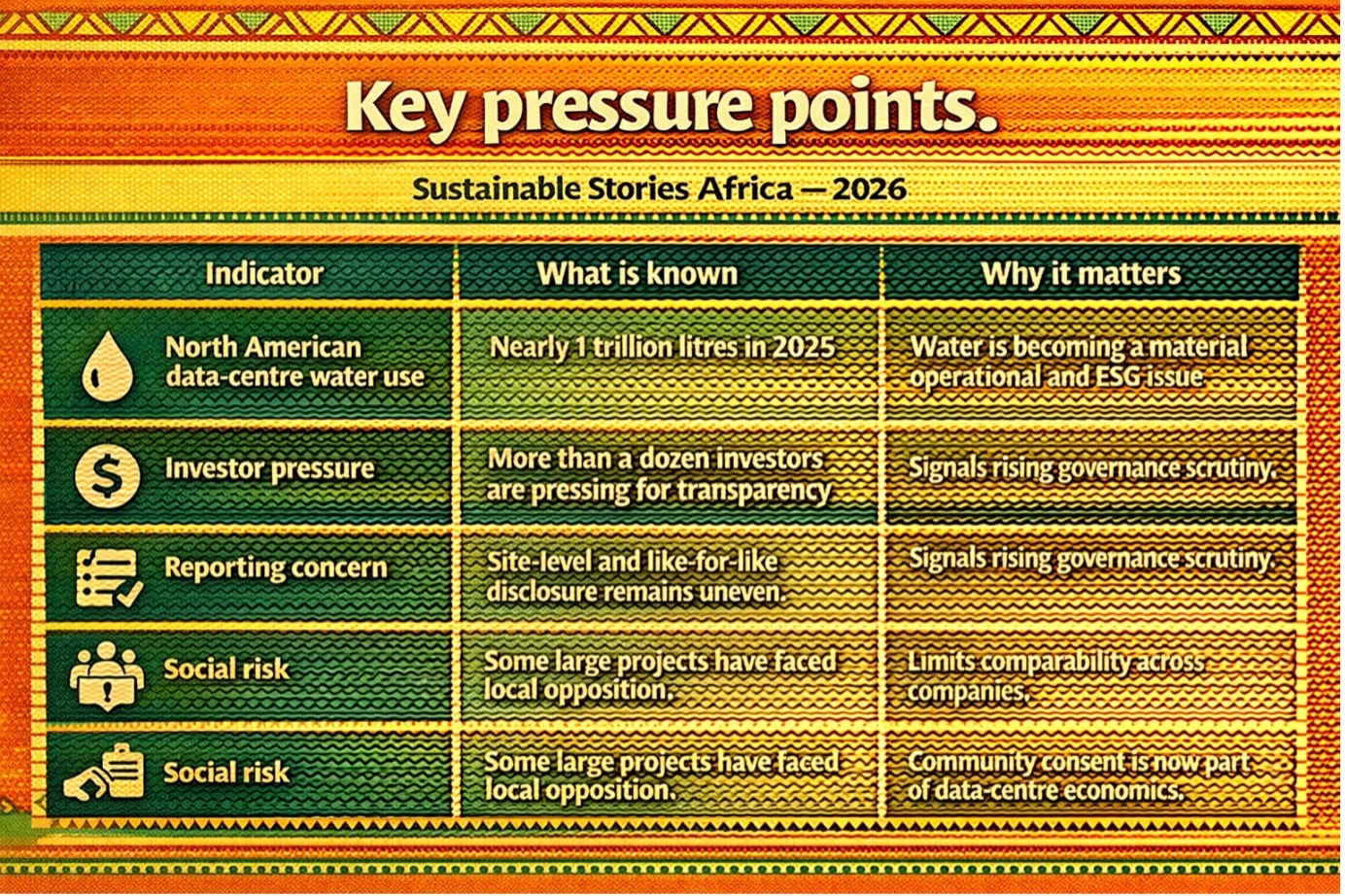

The concern matters now because North American data centres used nearly 1 trillion litres of water in 2025, as AI-driven infrastructure growth accelerates.

For markets, communities and regulators, the question is no longer only how fast digital infrastructure can scale, but whether it can do so without turning water stress into a new corporate integrity test.

Water is becoming AI’s newest accountability metric

The latest pressure on Amazon, Microsoft and Alphabet’s Google is not about carbon alone.

Investors are now demanding clearer disclosure on the water and energy burden of US data centres, arguing that rapid expansion is creating material environmental, governance and community risks.

According to Reuters, shareholder advocates, including Trillium Asset Management and Green Century Capital Management, are pressing the companies for site-specific transparency ahead of annual meetings.

The trigger is scale. North American data centres consumed nearly 1 trillion litres of water in 2025, according to market research, a volume roughly comparable to New York City’s annual water use.

The disclosure gap is now part of the risk

Investors are not arguing that hyperscale companies have done nothing. They are arguing that the current reporting architecture still leaves too much in the dark.

Google does not include third-party-operated sites in key disclosures, Microsoft has not provided site-level water reporting across its footprint, and Amazon has tended to report water use relative to power consumption rather than offering simple total figures for all facilities.

That matters because data-centre water use is intensely local. A litre withdrawn in a water-secure basin is not the same risk as a litre used in a drought-prone one.

The governance issue, then, is not only efficiency; it is whether investors and communities can see where the stress is landing, how companies are replenishing water, and whether climate promises still hold as AI demand rises.

That is why this is starting to look less like a narrow environmental story and more like a corporate-integrity test.

This is an inference based on the investor demands for site-specific disclosure and local community impact reporting.

The companies have set formal water goals. Amazon says AWS was 53% of the way to becoming water-positive by 2030 as of the end of 2024, while Google and Microsoft have also tied 2030 targets to replenishment and lower water-use intensity.

However, the harder question is whether those commitments are keeping pace with its expansion of data-centres.

Microsoft’s move to publish regional US water-use and replenishment data suggests investor and political pressure is already pushing water transparency from pledge to operating discipline today.

Better disclosure could turn risk into resilience

A stronger reporting standard would do more than answer critics. It would help investors price risk, communities weigh local trade-offs, and operators show digital infrastructure can scale without worsening water insecurity.

For Africa and other Global South markets, that lesson is urgent. As data-centre investment accelerates alongside AI and cloud demand, water disclosure, smarter siting and early community engagement cannot be deferred, especially in cities already facing water stress and fragile urban systems before infrastructure choices become harder to reverse.

This framework is a synthesis based on the issues investors are raising and the reporting gaps identified in current disclosures.

Big Tech now needs to prove growth can be water-smart

The next step is not another broad pledge. It is disciplined, decision-useful disclosure.

Investors want to know where the water is going, how much is being used, which locations are stressed, and whether claims of replenishment are measurable enough to trust.

Without that, “water positive” risks sounding like branding at the precise moment communities and capital markets are demanding evidence.

For boards, regulators and African policymakers watching the AI infrastructure race, the message is clear: data centres are no longer just energy assets.

They are water-governance assets too. In an era of tightening scrutiny of resources, companies that cannot explain their local water footprint may find that their ESG risks are reputational, financial, political and strategic.

Path Forward – Make Water Disclosure Match AI Scale

The priority now is site-level transparency, comparable reporting and clearer links between expansion plans and local water realities.

Investors are signalling that generic sustainability language is no longer enough.

For African markets, this is an early warning and a planning opportunity: build digital infrastructure, but embed water stewardship, community consent and disclosure discipline from the start.