Green bonds are entering a more demanding phase as investors, regulators, and issuers push harder on credibility, reporting and measurable impact.

That shift matters because labelled debt still finances a large share of climate-aligned projects, but weaker policy signals and rising scrutiny are testing momentum.

For African markets, the stakes are practical: credibility could unlock cheaper capital, while weak compliance could stall urgently needed climate investment.

A market built on trust now faces its hardest test

Green bonds are no longer judged simply by the label on the cover page. They are being judged by what the money funds, how clearly that is reported, and whether the promised environmental benefits can withstand tougher scrutiny. That is the real story shaping the next chapter of labelled debt.

The pressure is building from several directions at once. Climate Bonds Initiative says green-labelled bonds remained the largest segment of aligned sustainable debt in 2025, with $653.5 billion issued that year alone and more than $4 trillion in cumulative issuance.

However, Reuters, citing Sustainable Fitch, reported that green bond issuance in 2025 fell sharply year-on-year, with policy uncertainty and weaker climate ambition unsettling issuers and investors.

The rules are tightening, and the market is maturing

What is changing now is not just volume, but the standard of proof. ICMA’s Green Bond Principles, updated in June 2025, continue to anchor the market around four core components:

- Use of proceeds

- Project evaluation and selection

- Management of proceeds

- Reporting.

The Principles also recommend external review before issuance and stronger post-issuance verification of how proceeds are managed.

In Europe, the compliance bar is rising further. The European Commission says the EU Green Bond Standard is designed to tackle greenwashing and open new opportunities for issuers and investors.

ESMA says any firm offering external review services under the EU Green Bond Regulation after 21 June 2026 must be registered with the regulator.

That matters well beyond Europe. African issuers that want global capital increasingly must speak a language of disclosure and assurance that international investors recognise instantly.

That shift is especially important for Africa because the continent’s green bond story is still promising but concentrated.

FSD Africa says green bond issuances have generated about $9.6 billion in financing for the continent; however, approximately 91% of that volume has come from South Africa, Nigeria, Morocco, Egypt and the African Development Bank.

What stronger integrity could unlock

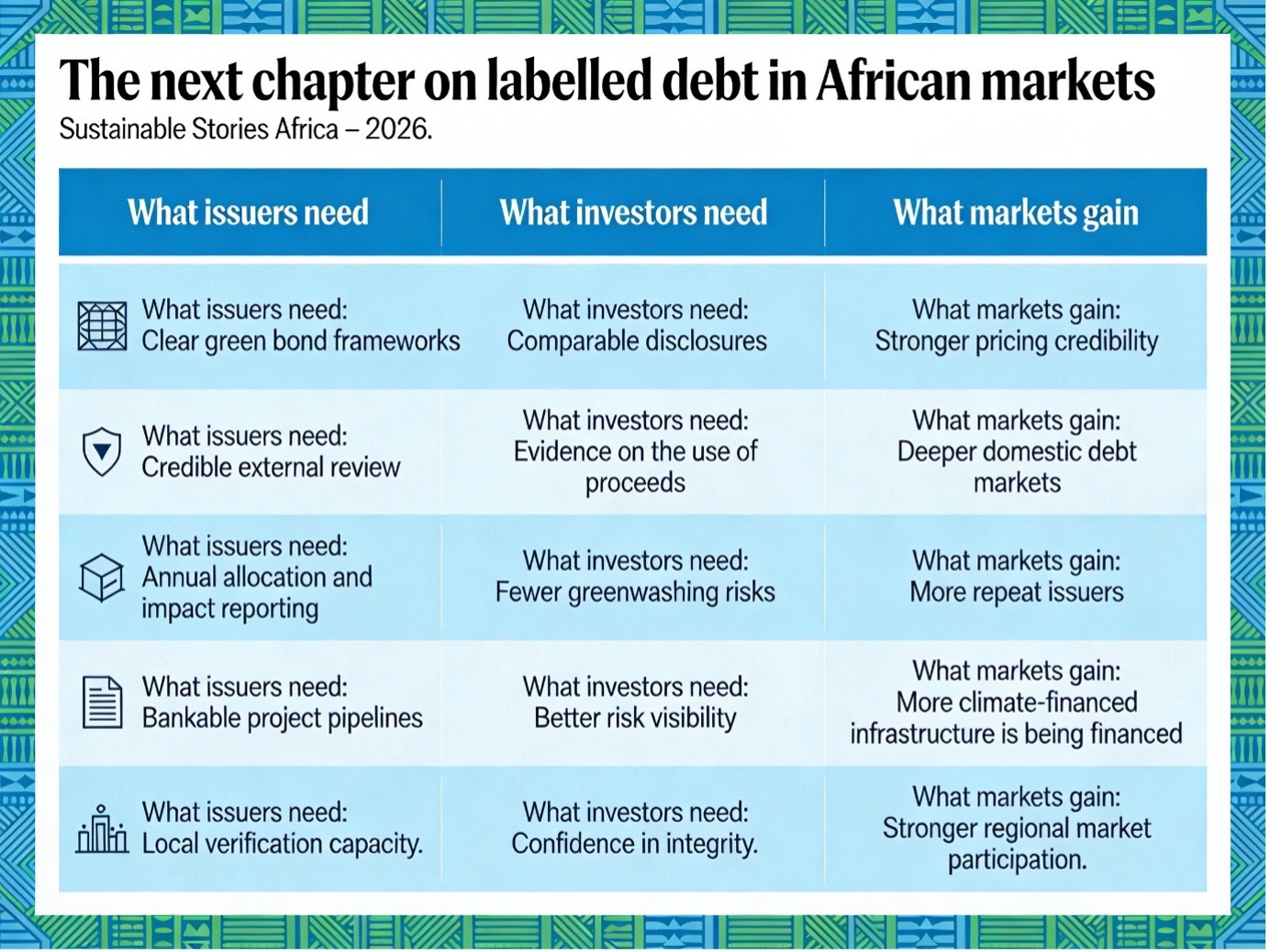

If this next phase is handled well, green bonds can do more than fund projects. They can lower the cost of climate finance, deepen domestic capital markets, and help African issuers ensure that sustainability claims are not marketing language but financing discipline.

That upside is why the compliance debate matters so much. In practical terms, better frameworks mean pension funds and insurers can allocate capital with greater confidence.

Sovereigns and corporates can finance energy, transport, water and resilience assets without facing constant doubts about credibility. And local regulators can build markets that attract repeat issuance rather than one-off transactions.

The African Development Bank’s sustainable bond programme and FSD Africa’s work on market development both point in that direction: labelled debt can support capital-market deepening, environmental outcomes and social co-benefits when frameworks, reporting and pipeline quality are strong.

However, the opposite is also true. If reporting is vague, project categories are stretched, or impact metrics are weak, issuers risk higher reputational costs and thinner investor demand.

Labels must now earn their legitimacy

The next step for the market is straightforward, even if it is not easy. Issuers need tighter frameworks, sharper project selection, and reporting that explains not just where money went, but what changed because it went there.

Regulators need clearer taxonomies, deeper reviewer capacity and rules that reward integrity rather than box-ticking. Investors, meanwhile, need to keep demanding evidence, not slogans.

For African markets, this is not an abstract compliance debate. It is about whether labelled debt can become a reliable bridge between climate ambition and affordable capital. The opportunity is real.

However, the market’s next chapter will belong to issuers that can prove environmental impact with the same seriousness they bring to credit quality.

Path Forward – Proof, Policy and Pipeline Must Align

Green bonds still have room to grow, but the growth will be harder won. The priority now is stronger reporting, credible assurance and clearer taxonomies that reduce investor doubt and protect market integrity.

For African markets, the promise lies in building repeat issuance pipelines, local verification capacity and rules that connect global standards to domestic realities.

That is how labelled debt can move from promise to durable climate finance.

Culled From: Green Bonds at a Crossroads: Impact, Compliance, and the Next Chapter for Labelled Debt