GHG Protocol has proposed a tougher boundary for Scope 3 reporting.

It would require companies to cover at least 95% of the required Scope 3 emissions.

That could reshape how firms, financiers and suppliers in African markets measure climate exposure.

The biggest emissions can no longer stay fuzzy

The GHG Protocol is moving toward one of its most significant Scope 3 revisions in years. In its March 31, 2026, Phase 1 progress update, it proposed coverage of at least 95% of required Scope 3 emissions and a new Category 16 for other value chain activities.

Though still draft guidance, the direction is clear: climate reporting is shifting toward fuller coverage, narrower exclusions, and clearer treatment of emissions that previously sat at the margins.

That matters because Scope 3 is where most corporate emissions sit. For African exporters, banks, agribusinesses, and manufacturers, weak value-chain accounting is no longer a technical shortfall but a market-access risk, as investors, lenders, and trade partners increasingly demand fuller, decision-useful climate disclosure from firms.

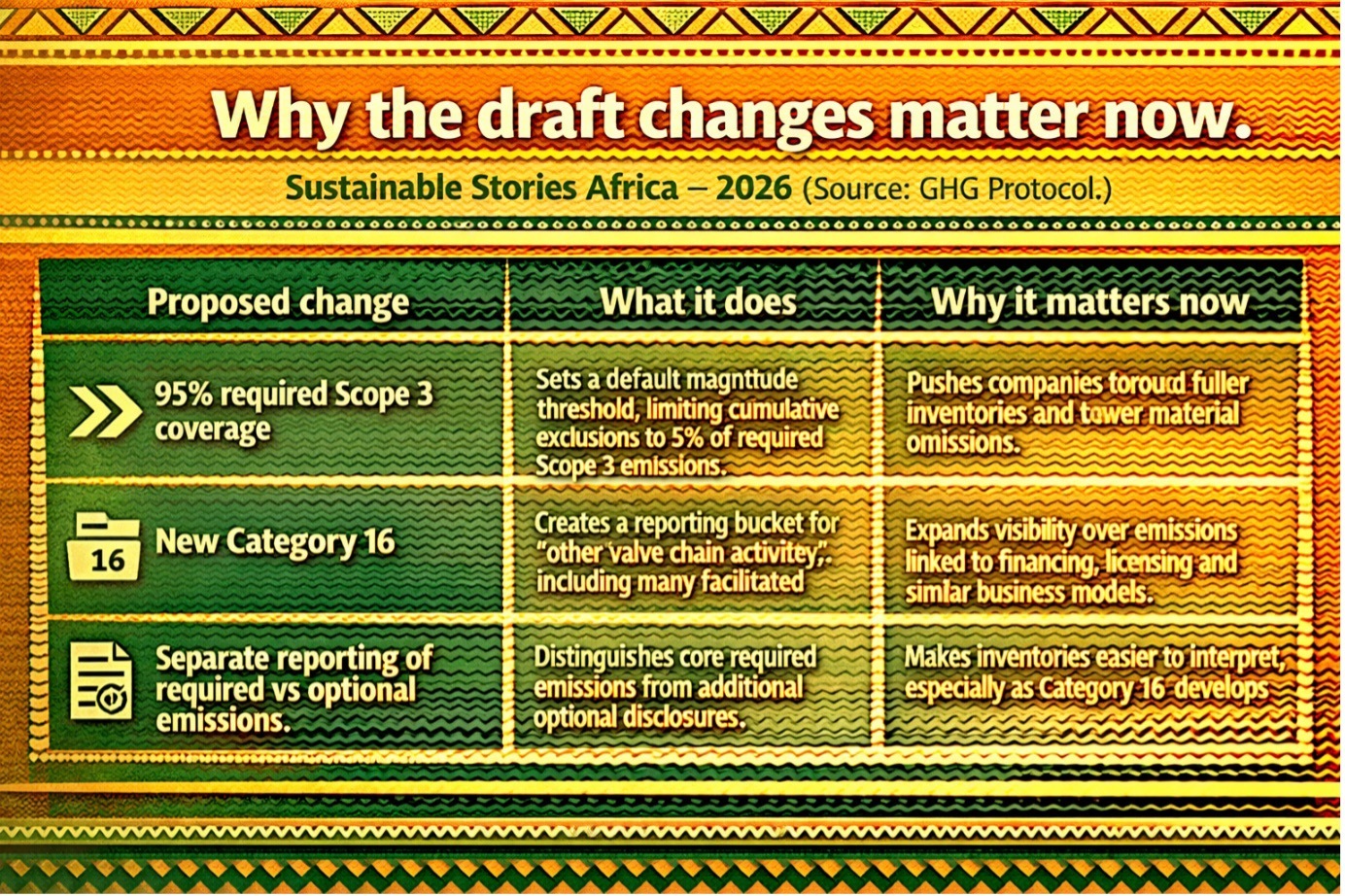

Why the draft changes matter now

Under the proposed revision, the Scope 3 framework would retain its 15 existing categories while adding a new Category 16 to capture other value chain activities that sit outside current boundaries, including facilitated activities such as underwriting, issuance, some insurance-related services, licensing, and certain commodity arrangements.

The proposed 95% reporting rule would further tighten disclosure discipline. Companies would be expected to account for at least 95% of required Scope 3 emissions, leaving limited room for exclusions.

Even where omissions fall within that 5% threshold, they would still need to be disclosed and justified, narrowing space for convenience-based underreporting in practice.

For African and Global South companies, tougher Scope 3 scrutiny is becoming a market reality, not an issue of compliance in the future.

Exporters, manufacturers, banks and telecom firms now face questions about emissions beyond their direct operations.

However, the constraint is clear: weak data systems, patchy supplier information and limited capacity still hinder reporting, even as international finance demands comparability, rather than approximation.

What better Scope 3 accounting could unlock

Done well, the update could produce something African markets badly need: cleaner visibility into where climate risk and decarbonisation opportunities actually sit.

Better Scope 3 reporting can help companies identify hotspots in procurement, logistics, product use and financed activities.

It can also improve supplier engagement, strengthen transition plans and give lenders and investors a more credible view of where carbon-linked risk may hit margins, trade exposure or asset values.

There is a deeper governance gain, too. Category 16 signals that the old reporting map no longer captures the full shape of modern business models.

Financial institutions, insurers, licensors and intermediaries increasingly create value through activities they do not physically own but materially enable.

Bringing more of those emissions into view will not solve carbon accountability overnight, but it could close one of the most persistent blind spots in corporate integrity reporting.

Africa should prepare before the rules harden

The sensible response is not panic. It is preparation.

- Companies should start by identifying their largest missing Scope 3 data gaps, especially in purchased goods, transport, product use, investments and facilitated activities.

- Regulators, stock exchanges and industry groups in African markets should also pay attention now, because once global disclosure expectations tighten, local firms will be judged against them, whether local readiness is complete or not.

This is where policy and business strategy meet. If African markets wait until the standard is final, compliance could become expensive, reactive and externally defined.

If they move early, companies can shape better supplier data systems, sector guidance and proportional reporting pathways that reflect local realities while still meeting global expectations.

The real prize is not just better disclosure. It is stronger competitiveness in a world where carbon data increasingly travels with capital, contracts and credibility.

Path Forward – Count deeper, disclose earlier, align faster

African companies should treat the draft as an early warning and a strategic opening.

The priority now is to map material Scope 3 gaps, improve supplier and partner data, and build internal systems that can support fuller value-chain accounting.

For regulators and market institutions, the next step is clear: develop sector-aware guidance early, especially for finance, commodities, manufacturing and export-heavy sectors.

That is how climate reporting becomes more credible, more usable and more investable across African markets.

Culled From: GHG Protocol Proposes 95% Scope 3 Coverage Rule and New Category 16 in Reporting Standard Update