Nigeria’s pension system has long excluded most of the informal sectors of the Nigerian economy.

Now, a newly licensed distribution model seeks to close that gap. If it scales, it could redefine pension inclusion across Africa.

Nigeria’s Pension Architecture Reaches Inflexion

Nigeria’s pension architecture may be entering a structural reset. In this in-depth conversation, Uade Ahimie, Editor-in-Chief of Sustainable Stories Africa, engages Tunji Andrews, Founder and CEO of Awabah, on the company’s journey from identifying a structural “missing middle” to securing Nigeria’s first Accredited Pension Agent License.

Andrews traces Awabah’s origins to a system designed primarily for formal corporate employees, leaving informal workers, who contribute over half of the national GDP, without pension protection.

What began as a recognition of near-zero pension participation among traders, artisans, and freelancers evolved into a regulatory milestone that he describes as a “paradigm shift,” signalling that last-mile distribution is as critical as fund management.

The discussion explores scepticism around whether the informal sector is “unbankable,” the governance and compliance reforms required to secure PenCom approval, and the economics of digital distribution in a high-inflation environment.

It concludes with broader implications for Nigeria’s pension architecture, African scalability, and the next defining milestone: delivering measurable volume and dignified retirement outcomes at scale.

Informal Majority Locked Out of Pension Systems

Nigeria’s contributory pension scheme was designed around formal employment payroll structures. Andrews argues that the design choice created a structural exclusion.

“The gap was a massive ‘missing middle,’” he said. “Nigeria’s pension system was built for the formal corporate world, leaving the millions of Nigerians in the informal sector, completely stranded without a safety net”.

The urgency is demographic and economic. Informal workers, including traders, artisans, and freelancers, form the backbone of Nigeria’s productive base.

However, pension penetration among them is negligible. According to Andrews, the lived consequence is visible: workers “fall into immediate poverty the moment they can no longer work”.

The issue is not merely social; it has macroeconomic implications. Without long-term domestic savings mobilisation from the informal majority, Nigeria’s capital markets remain shallow relative to economic size.

Distribution Model Challenges Pension Orthodoxy

The deeper structural insight from the interview is that pension exclusion is less about unwillingness to save and more about flawed distribution assumptions.

“Sceptics thought the informal sector was ‘unbankable’ or too ‘disorganised’ for pensions,”

Andrews said.

“They misunderstood the desire for security”.

Awabah’s model reduces acquisition costs through digital infrastructure and community-based aggregators, enabling outreach to remote markets without the additional costs associated with expanding a physical branch structure.

That shifts pension economics from fixed-asset-heavy distribution to variable, tech-enabled scaling.

Regulatory engagement was central. Andrews described moving “from scepticism to partnership,”emphasising that Awabah had to prove it was “deeply compliant” and capable of strengthening ecosystem integrity.

Licensing required institutionalising data protection, governance frameworks, and transparent reporting structures.

The governance signal is clear: innovation is permissible, but only within regulatory guardrails.

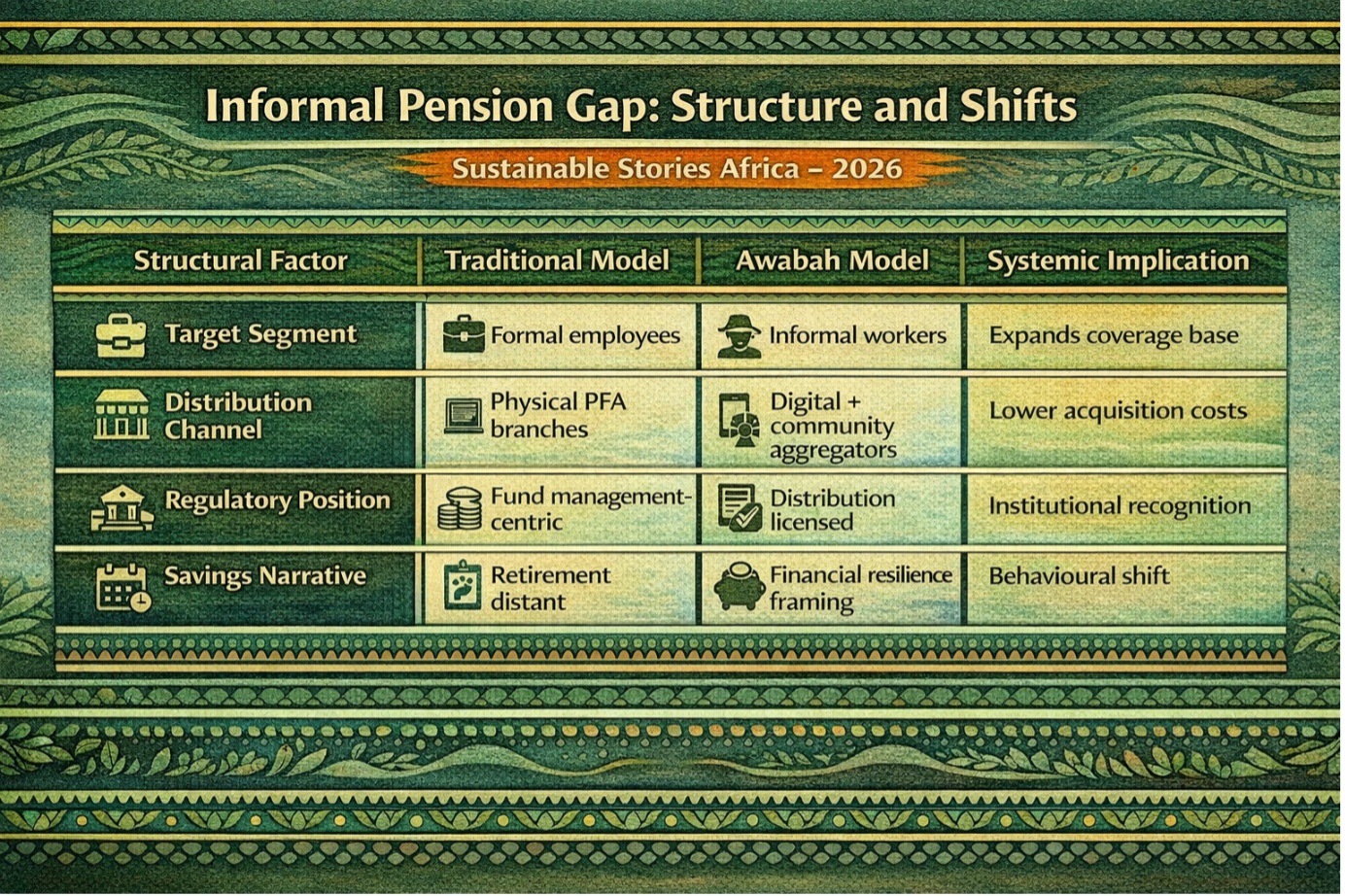

Informal Pension Gap: Structure and Shifts

Structural Factor | Traditional Model | Awabah Model | Systemic Implication |

|---|---|---|---|

Target Segment | Formal employees | Informal workers | Expands coverage base |

Distribution Channel | Physical PFA branches | Digital + community aggregators | Lower acquisition costs |

Regulatory Position | Fund management-centric | Distribution licensed | Institutional recognition |

Savings Narrative | Retirement distant | Financial resilience framing | Behavioural shift |

Andrews frames the savings challenge within Nigeria’s inflationary environment not as a retirement narrative but as a resilience-building one. “In a volatile economy, the only thing worse than inflation is having no savings at all,” he said.

This reframing aligns pensions with household risk management rather than distant retirement abstraction, which is critical in economies where income volatility is high.

Scaling Volume To Validate the Inclusion Model

The immediate test is scale. “The next milestone is ‘Volume,’” Andrews noted. “We’ve proven the tech and the legal framework; now we have to prove the scale”.

If successful, the model signals broader institutional consequences:

- Investor Implications – Larger pension participation expands long-term domestic capital pools.

- Policy Implications – Distribution-led frameworks may require further PenCom regulatory refinements.

- Governance Implications – Licensed aggregators introduce new accountability nodes within pension supervision.

- Regional Implications – “Nigeria is often the litmus test… the blueprint can be exported to Ghana, Kenya, and beyond,” Andrews said.

The model marks what he describes as the end of the “wait and see” era, shifting toward a system where “the pension comes to the person”.

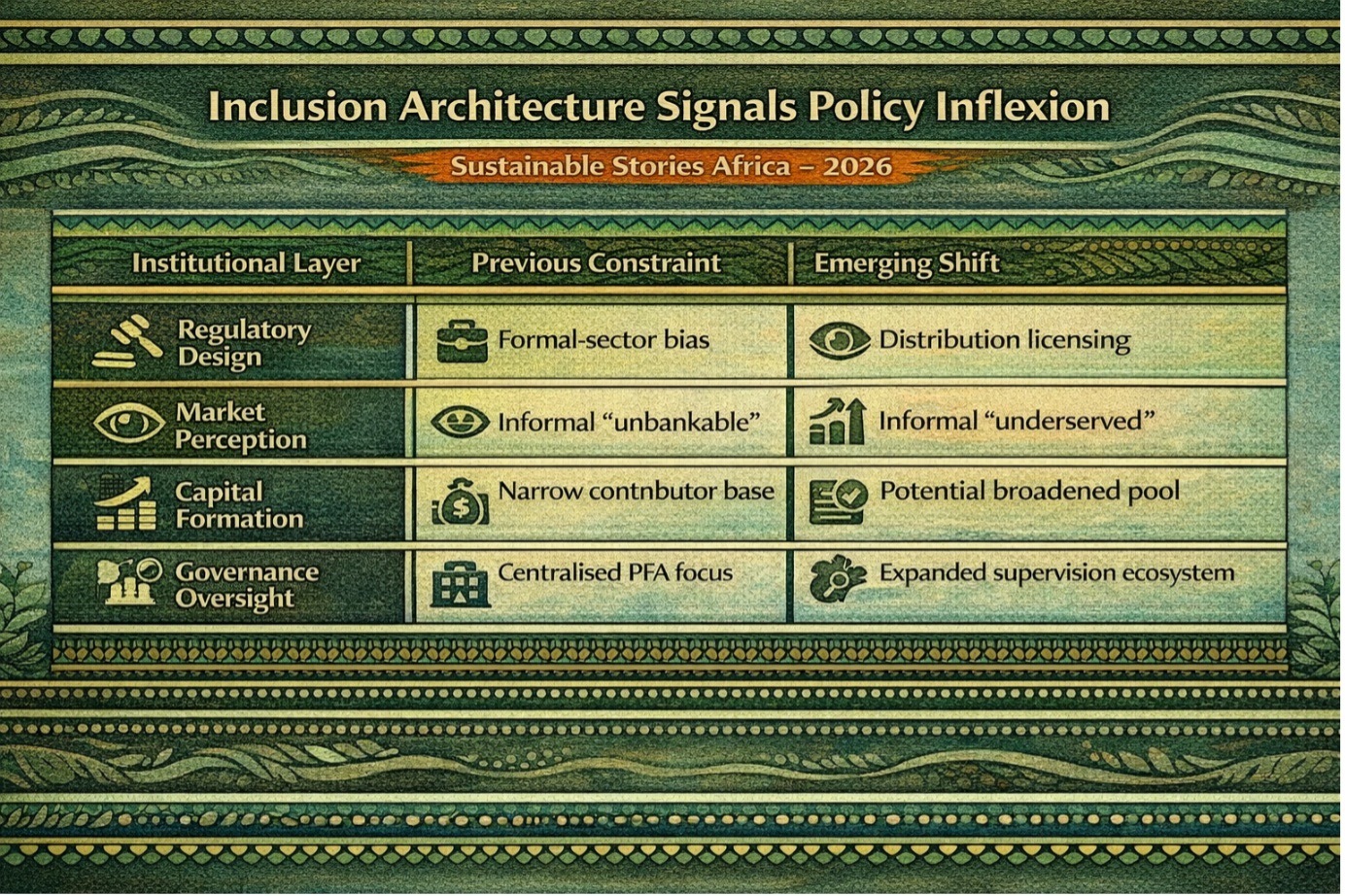

Inclusion Architecture Signals Policy Inflexion

Institutional Layer | Previous Constraint | Emerging Shift |

|---|---|---|

Regulatory Design | Formal-sector bias | Distribution licensing |

Market Perception | Informal “unbankable” | Informal “underserved” |

Capital Formation | Narrow contributor base | Potential broadened pool |

Governance Oversight | Centralised PFA focus | Expanded supervision ecosystem |

The structural tension now lies between regulatory integrity and rapid scale. The “chicken and egg” phase, which offers securing partnerships without a license while still requiring a regulatory license to scale, illustrates the fragility of innovation in tightly regulated sectors.

Patience, Andrews said, became “a strategic asset,” requiring the discipline to “hurry slowly”. In pension systems, credibility compounds as slowly and as powerfully as capital.

Scale, Governance, and Trust Must Align

The licensing milestone marks a significant transformation of Nigeria’s pension reform from concept to implementation. The next test is measurable enrolment growth among informal workers.

If distribution-led inclusion strengthens compliance, expands domestic savings and maintains supervisory integrity, Nigeria could establish a replicable African template. Success, Andrews argues, will not be regulatory symbolism, but outcomes: informal workers retiring “with dignity” because they participated early.

Institutional resilience, which offers novelty, will define whether this shift endures.