South Africa is mobilising climate finance at scale, but not at the speed its net-zero targets demand.

New data reveals ZAR 188.3 billion in annual climate finance flows; however, investment needs could reach ZAR 499 billion per year, leaving a structural financing gap that threatens both mitigation ambition and just transition commitments.

South Africa’s Climate Finance Crossroads

South Africa’s climate transition has moved decisively from ambition to implementation.

The South African Climate Finance Landscape 2025 report, prepared for the Presidential Climate Commission (PCC), tracks an annual average of ZAR 188.3 billion in climate finance flows between 2022 and 2023.

This marks a substantial increase from ZAR 130.6 billion between 2019 and 2021 and ZAR 62.2 billion between 2017 and 2018.

However, the headline number conceals a more sobering reality: estimated annual climate investment needs may reach ZAR 499 billion, implying a financing gap of up to ZAR 311 billion per year.

The country’s transition is accelerating, but is yet to align with the scale required to meet its tightened Nationally Determined Contributions (NDCs) and 2050 net-zero pathway.

Energy Dominance, Adaptation Deficit

South Africa’s climate finance landscape is structurally concentrated.

Of the ZAR 188.3 billion tracked annually, 74.1% (ZAR 139.5 billion) flowed into the energy sector, primarily solar PV, wind and battery storage investments.

This reflects both the urgency of the electricity crisis and policy reforms such as lifting the 100 MW licensing cap and enabling private embedded generation.

By contrast, adaptation finance accounted for only 11.3% of total flows, well below the African average of 33.7%.

This imbalance presents systemic risk. South Africa is a climate hotspot, warming at more than twice the global average, with intensifying droughts, floods and heatwaves.

However, water, agriculture, forestry and urban resilience remain underfinanced.

Climate finance is growing but unevenly.

Domestic Capital Leads, Concessional Gaps Persist

South Africa’s climate finance profile reflects its upper-middle-income status.

Nearly 60% of total flows originated domestically, led by commercial banks (ZAR 36.6 billion annually), corporations (ZAR 28.4 billion) and households investing in rooftop solar (ZAR 15.2 billion).

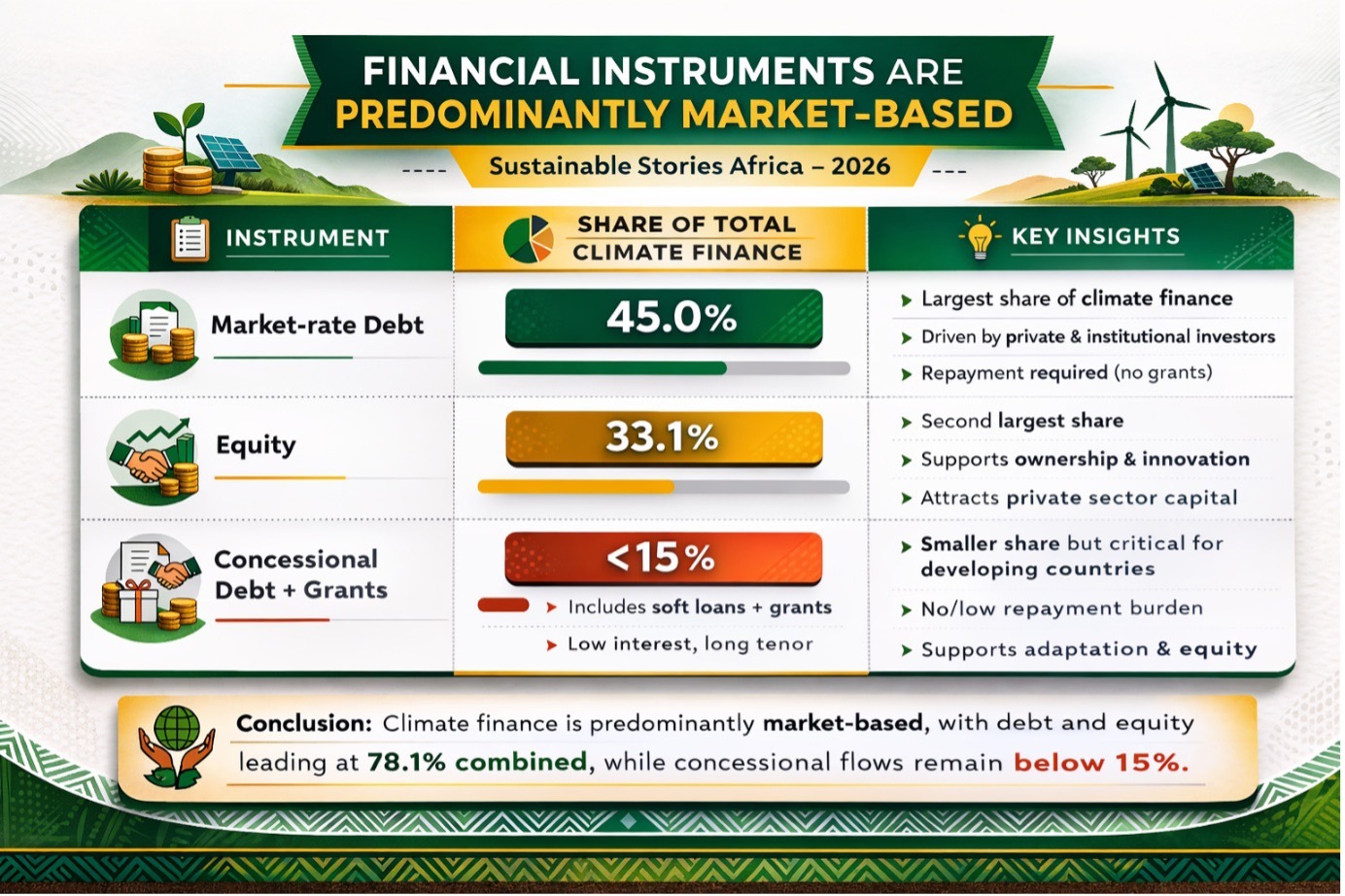

Financial instruments are predominantly market-based:

Instrument | Share of Total Climate Finance |

|---|---|

Market-rate debt | 45.0% |

Equity | 33.1% |

Concessional debt + grants | <15% |

Financial instruments are predominantly market-based

While this signals strong private sector participation, it also exposes structural constraints.

With the repo rate peaking at 8.25% in 2023, borrowing costs remain elevated. Municipalities and small enterprises are facing difficulties in accessing capital, especially for adaptation and just transition projects.

International climate finance, which is averaging ZAR 73.7 billion annually, is dominated by bilateral and multilateral development finance institutions (79.2% of international flows).

The Just Energy Transition Partnership (JETP) remains central, despite the United States’ withdrawal in early 2025, as European partners reaffirm commitments.

However, concessional capital remains insufficient to de-risk transmission expansion, adaptation infrastructure and worker transition programmes.

Tracking the Transition

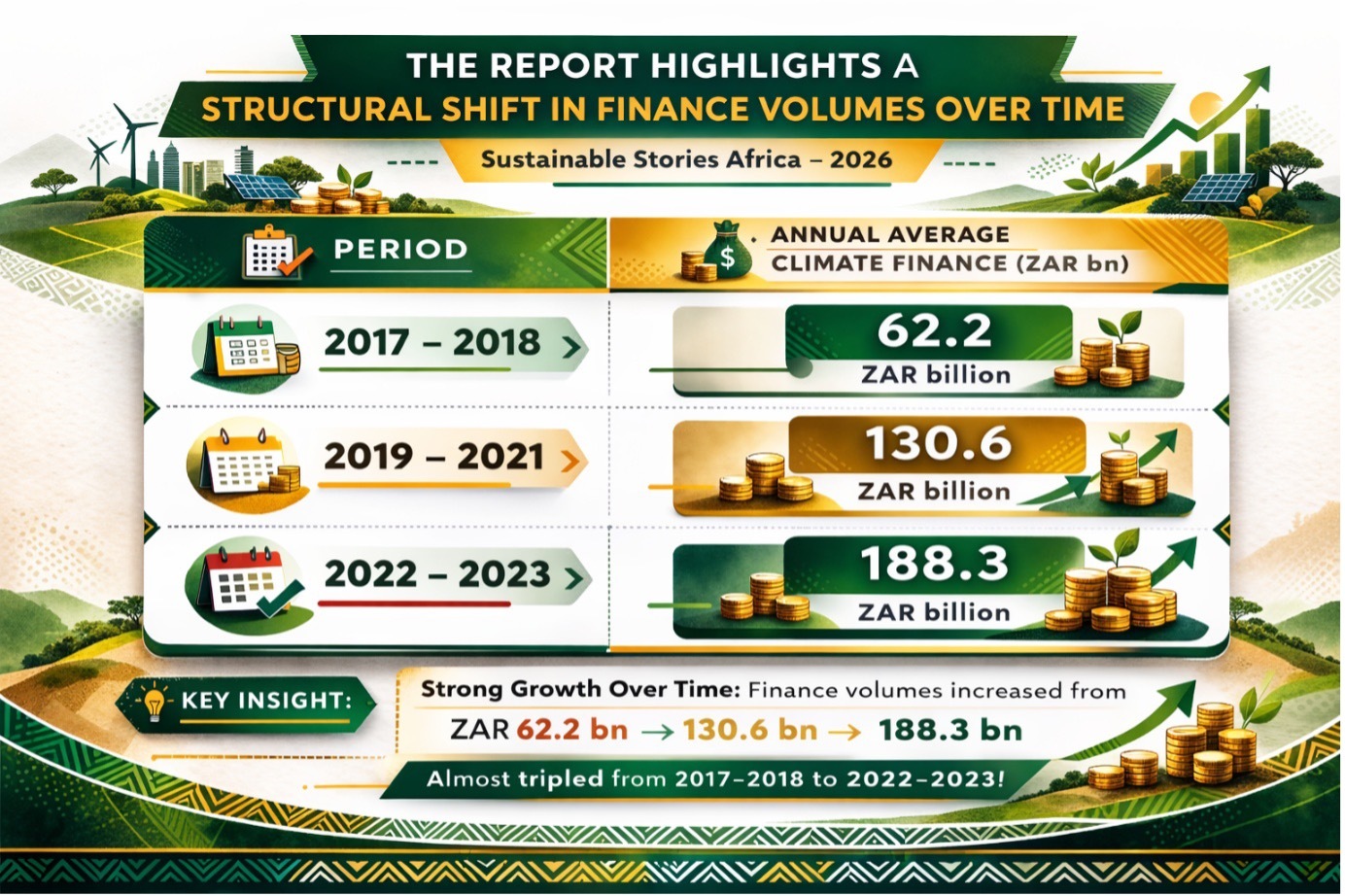

The report highlights a structural shift in finance volumes over time:

Period | Annual Average Climate Finance (ZAR bn) |

|---|---|

2017 – 2018 | 62.2 |

2019 – 2021 | 130.6 |

2022 – 2023 | 188.3 |

This upward trajectory reflects regulatory reform, tax incentives (including solar rebates), and improved project bankability.

However, sectoral investment needs remain substantially higher:

- Electricity system expansion and grid build-out require large-scale capital (Section 4; Table 2).

- Industrial decarbonisation pathways (steel, cement, chemicals) demand substantial investment (Table 3).

- Transport, buildings, agriculture and water sectors face cumulative underinvestment.

Importantly, just transition-aligned finance averaged only ZAR 16.0 billion between 2022 and 2023. This is modest relative to the scale of socioeconomic restructuring required in coal-dependent regions.

Immediate Levers and Structural Reform

The report reveals dual pathways: near-term acceleration and structural reform.

Immediate Actions:

- Institutionalise climate budget tagging across government levels.

- Finalise the Integrated Resource Plan (IRP 2023).

- Expand concessional and blended finance for adaptation and just transition.

- Scale risk mitigation tools (guarantees, first-loss tranches).

- Strengthen project preparation pipelines.

Structural Reforms:

- Establish a dedicated climate finance unit within the National Treasury.

- Empower municipalities to issue green bonds and pool finance.

- Fast-track grid and transmission expansion under electricity reform.

- Deepen domestic capital markets aligned with the South African Green Finance Taxonomy (SA GFT).

These reforms aim to embed climate finance governance within South Africa’s fiscal architecture, rather than treating climate flows as ad hoc or externally driven.

PATH FORWARD – Scale, Diversify, Institutionalise

South Africa must double or triple annual climate finance flows to align with NDC targets and long-term net-zero commitments.

This requires scaling domestic capital mobilisation, crowding in concessional resources for adaptation and a just transition, and accelerating grid and infrastructure reform.

The transition is underway, but to become resilient and inclusive, climate finance must transition beyond energy dominance to a broader, system-wide investment strategy.