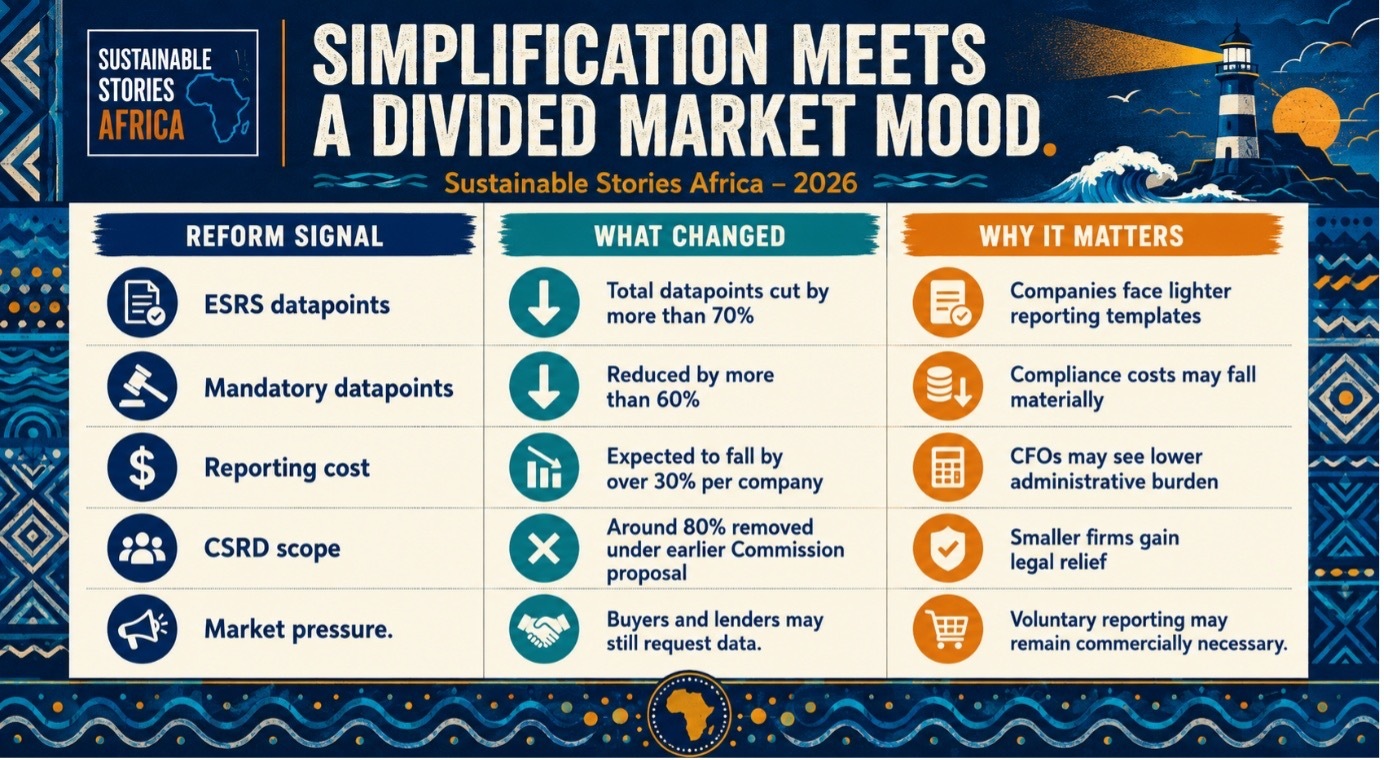

The European Commission has released revised sustainability reporting standards that cut the total number of ESRS data points by more than 70%.

The move sits within the EU’s Omnibus reform, which narrows CSRD obligations and promises lower compliance costs.

For African suppliers, the relief in Brussels may not erase pressure from investors, buyers and banks demanding credible ESG data.

Reporting Reset Puts Sustainability Rules On Trial

The European Union has moved to simplify its corporate sustainability reporting regime, releasing revised European Sustainability Reporting Standards that cut mandatory data points by more than 60% and total data points by more than 70%, while promising to reduce company-level reporting costs by more than 30%.

The reform is part of Brussels’ wider Omnibus package, designed to reduce regulatory burdens and sharpen European competitiveness.

Earlier Commission proposals said around 80% of companies would be removed from the Corporate Sustainability Reporting Directive’s scope, with reporting concentrated on larger companies above new size thresholds.

Some market analyses and post-agreement reporting have described the final scope reduction as approaching 90%, underscoring the scale of the reset.

For African companies linked to European buyers, financiers and supply chains, the headline may sound distant. It is not. The question is no longer only who must report under EU law.

It is those who must still provide sustainability data to keep contracts, attract finance and remain visible in global value chains.

Simplification Meets A Divided Market Mood

The revised ESRS are meant to make sustainability reporting shorter, clearer and more proportionate.

The Commission says the new drafts introduce flexibilities, simplify materiality assessment and reduce duplication.

The political argument is clear: Europe wants sustainability rules that do not overwhelm business.

Companies had complained that overlapping standards, complex templates and extensive value-chain requirements were turning ESG into an administrative exercise.

However, the counterargument is equally strong. Critics warn that reducing mandatory disclosure could weaken transparency, especially for climate risk, labour standards and supply-chain impacts.

For a cocoa processor in Ghana, a garment supplier in Kenya, or a renewable-energy contractor in Nigeria, the effect may be uneven.

A European buyer may no longer be legally required to report as much. However, banks, insurers, development financiers and large multinationals may still ask for emissions data, labour-risk information and evidence of governance.

Better Rules Could Strengthen Real Disclosure

The strongest case for reform is not weaker ESG. It is better ESG.

A leaner ESRS could help companies focus on material issues rather than performative reporting.

If the new framework reduces noise, businesses may spend less time filling templates and more time measuring what matters: energy use, transition risk, workforce safety, water stress, supplier exposure and board accountability.

That matters for African markets, where sustainability reporting is constrained by limited data systems, fragmented regulation and cost pressures.

A simplified global benchmark could help companies build credible disclosures without copying the complexity of larger European peers.

The risk, however, is that simplification becomes silence. If fewer firms report, sustainability data could become less comparable.

Investors may struggle to distinguish companies that manage real risks from those simply avoiding scrutiny.

Smaller suppliers may also face informal reporting demands without clear templates or support.

That is where voluntary standards become important. The Commission has said it will adopt a voluntary reporting standard to limit what larger companies and banks can demand from smaller value-chain partners.

For African SMEs, this could become a practical shield against excessive paperwork if implemented clearly.

African Firms Need Data Before Deadlines

The next move should come from boards, regulators and business associations across African markets. Waiting for EU rules to settle is not a strategy.

Companies that export to Europe or depend on international finance should map the ESG data they already hold, identify gaps and build low-cost reporting systems about material risks.

Regulators can help by aligning local sustainability guidance with global standards while avoiding copy-and-paste compliance burdens.

The commercial lesson is direct: legal obligation may shrink, but market expectation may not. Sustainability data is becoming part of credit assessment, procurement screening and investor due diligence.

Firms that treat disclosure as a strategic capability, rather than a European paperwork problem, will be better positioned.

Path Forward – Requires Practical ESG Readiness

African companies should prepare for a lighter but sharper disclosure environment by building credible, decision-useful ESG data systems now.

The priority is proportionate reporting: fewer vanity metrics, stronger materiality, clearer governance, and practical support for SMEs in supply chains. Europe may be cutting datapoints, but the market still rewards trust.

Culled From: EU Releases Revised ESRS with 70% Datapoint Cut and 90% CSRD Scope Reduction Under Omnibus Reform