Global food and agriculture systems are responsible for nearly 30% of all greenhouse gas emissions; however, they receive just 7% of global climate finance, a gap undermining every climate commitment made at international summits.

As policymakers have concluded COP30, FAO data confirms that the greatest untapped potential for climate action lies in transforming agrifood systems, not solely in decarbonising energy grids.

Nowhere is the urgency sharper than in Africa, where 65 million smallholder farmers face existential climate shocks daily, waiting for finance and policy support that could turn their fields from liabilities into carbon solutions.

The Field Is Already on Fire

Agriculture sits at the centre of the climate crisis, even if global climate strategy still treats it as peripheral.

The world’s farms, livestock systems and food supply chains generate 16.2 billion tonnes of carbon dioxide equivalent each year, or approximately 30% of human-caused emissions, putting the sector among the largest contributors to global warming.

The implication is direct. Agrifood systems reform is essential, not optional, if the world hopes to keep warming within 1.5°C. For Africa’s 65 million smallholder farmers, this is not an abstract global debate.

Climate disruption is already showing up in failed harvests, prolonged droughts and destructive floods, hitting livelihoods at the point of survival.

A Sector Too Big to Ignore, Too Underfunded to Act

Agriculture embodies the climate paradox: it is both a major source of emissions and amongst the strongest pathways for carbon sequestration.

Livestock, methane, fertiliser use, farmland expansion and food waste all deepen the sector’s climate burden, making food systems central to any credible emissions strategy.

However, funding remains badly misaligned with that reality. Although food systems account for nearly a third of global emissions, they attract only 7% of climate finance.

In Africa, the gap is sharper still. Smallholder farmers need far more support for drought-resistant seeds, irrigation, early-warning systems and climate adaptation, which the financing currently does not deliver.

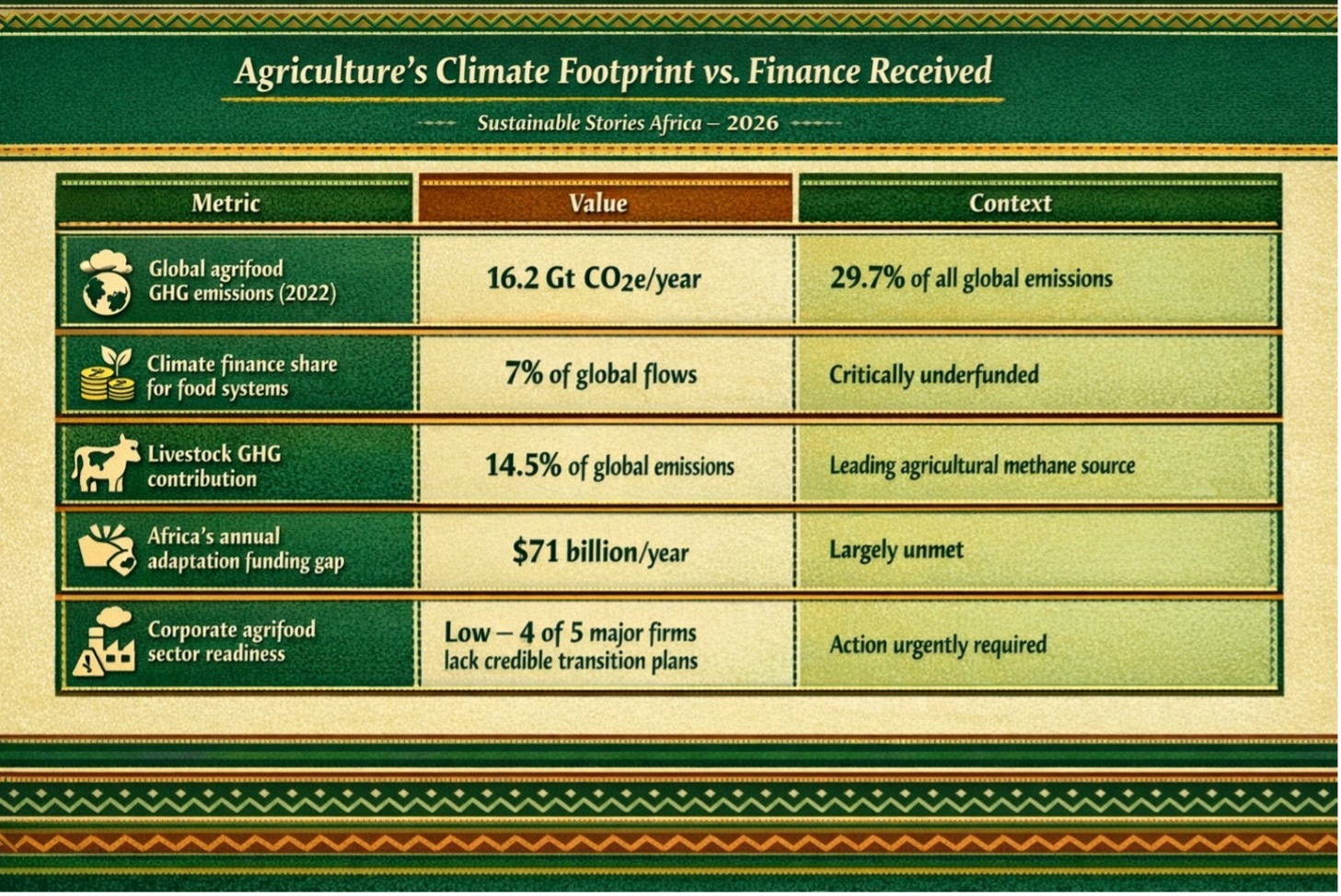

Agriculture's Climate Footprint vs. Finance Received

| Metric | Value | Context |

|---|---|---|

| Global agrifood GHG emissions (2022) | 16.2 Gt CO2e/year | 29.7% of all global emissions |

| Climate finance share for food systems | 7% of global flows | Critically underfunded |

| Livestock GHG contribution | 14.5% of global emissions | Leading agricultural methane source |

| Africa's annual adaptation funding gap | $71 billion/year | Largely unmet |

| Corporate agrifood sector readiness | Low – 4 of 5 major firms lack credible transition plans | Action urgently required |

Africa is already paying the economic price of climate disruption. The AfDB warns GDP could shrink 3% annually by 2030, as farm losses deepen poverty.

On the corporate side, a 2025 assessment of five of the world's largest agrifood companies, including Danone, JBS, Mars, Nestlé, and PepsiCo, found that current climate commitments are "unlikely to result in meaningful emission reductions."

What a Transformed Food System Could Deliver

The solutions are practical, immediate and increasingly hard to ignore. The FAO’s pre-COP30 white paper argues that if agriculture moves from the margins to the centre of climate strategy, the gains for emissions reduction, food security and economic resilience could be significant.

Better soil carbon management, wetland restoration, cleaner rice cultivation and improved livestock practices together offer substantial annual emissions cuts, while also strengthening farm productivity and resilience.

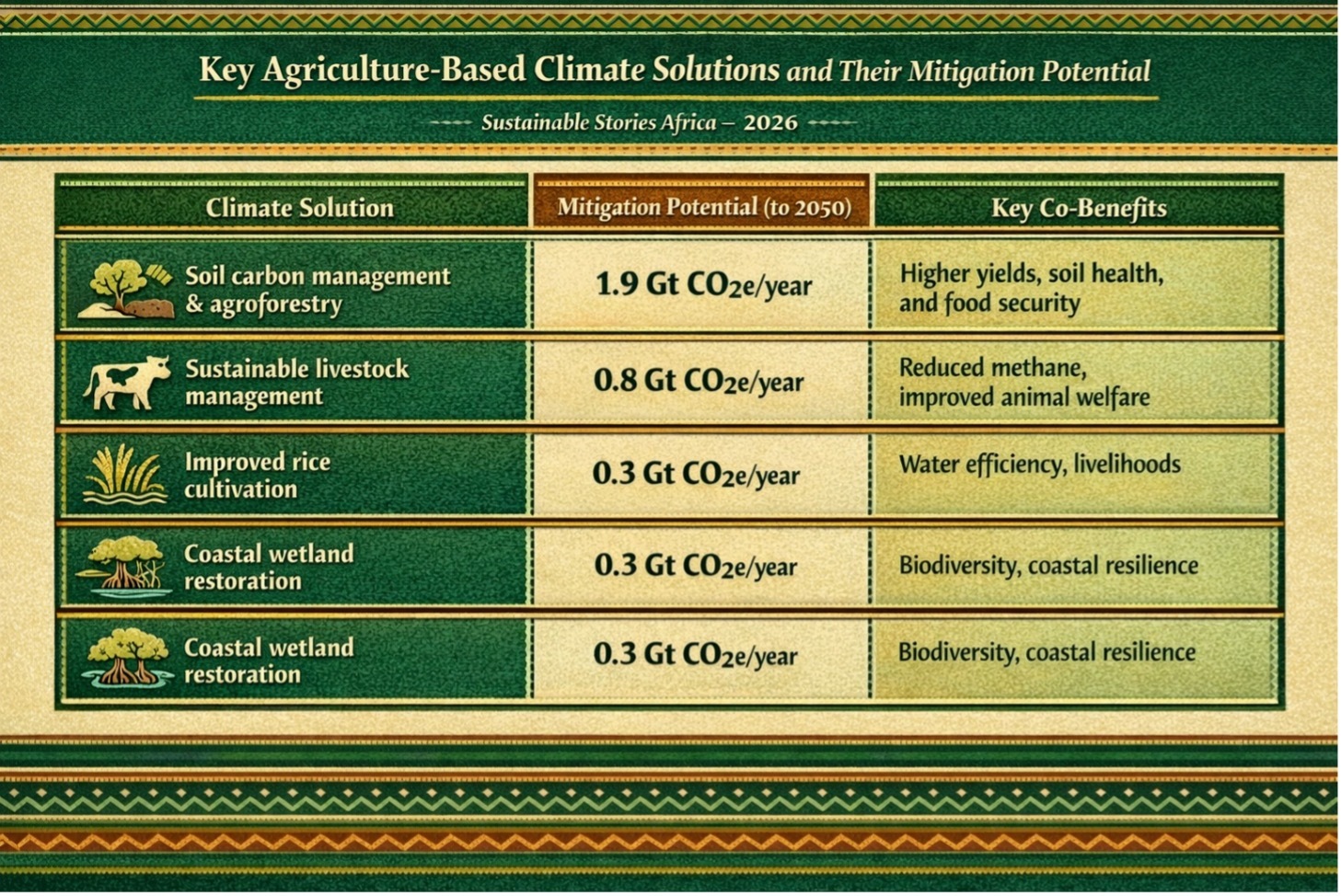

Key Agriculture-Based Climate Solutions and Their Mitigation Potential

| Climate Solution | Mitigation Potential (to 2050) | Key Co-Benefits |

|---|---|---|

| Soil carbon management & agroforestry | 1.9 Gt CO2e/year | Higher yields, soil health, and food security |

| Sustainable livestock management | 0.8 Gt CO2e/year | Reduced methane, improved animal welfare |

| Improved rice cultivation | 0.3 Gt CO2e/year | Water efficiency, livelihoods |

| Coastal wetland restoration | 0.3 Gt CO2e/year | Biodiversity, coastal resilience |

Climate-smart agriculture in Africa is commercially viable. The ARAF Fund, backed by a $23 million GCF guarantee and $58 million capital, has reached over 2 million farmers, with 90% reporting higher incomes and SunCulture delivering 100%-plus income growth.

The World Must Rebalance Its Climate Investment

Food systems remain one of climate finance’s clearest failures. Governments, development banks and private investors need to redirect capital toward agrifood transformation, treating it not as charity but as a high-return climate strategy.

That means embedding agriculture more clearly in national climate plans, with measurable targets for livestock emissions, fertiliser use and land-use change.

It also means pushing food companies to adopt transition targets tied to protein shifts, lower-input farming and food waste reduction.

For Africa, the stakes are even higher. Agriculture supports about 60% of the workforce and underpins growth across much of the continent.

Climate-smart agriculture is therefore not only an environmental necessity; it is a practical route to economic resilience, food sovereignty and stronger global climate credibility.

Path Forward – Finance the Fields, Save the Future

With COP30 over, global institutions need to close the agrifood climate finance gap by scaling green instruments, embedding food systems in NDCs and directing catalytic capital toward Africa’s smallholder farmers.

The FAO’s evidence is clear: better soil management, agroforestry and sustainable livestock practices can cut emissions, while strengthening food security and rural incomes.

For Africa, the way forward requires stronger policy, faster blended investment and credible corporate accountability across food value chains. Farming is not peripheral to climate action. It is central.

Culled From: Agriculture Is the Real Climate Battleground