Corporate governance is undergoing its biggest transformation since the early 2000s, and climate change is the force reshaping its entire architecture. According to the Global Corporate Sustainability Report 2025, boards overseeing more than 70% of global market capitalisation now have formal responsibility for climate-related decision-making, marking a shift from ESG compliance to full-scale strategic oversight.

From Europe to Asia and the Americas, climate governance is emerging as the new language of corporate power. Board committees are being redesigned, executive compensation is being tied to emissions reduction, and shareholder engagement is increasingly centred on transition risks rather than traditional financial metrics. The report shows that climate governance is no longer an environmental appendage; it is increasingly "a core financial risk domain embedded directly into enterprise strategy."

Governance Steps Into the Climate Arena

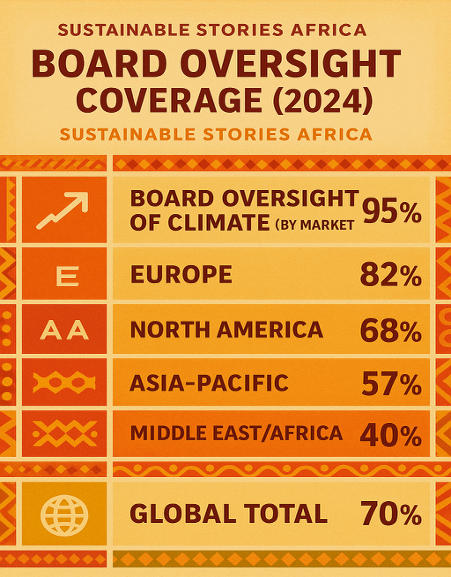

The most striking finding in the report is how climate oversight has moved into the boardroom mainstream. Nearly all large companies in Europe now disclose climate governance structures, with rapid growth seen in Asia and North America.

By contrast, only 40% of African and Middle Eastern firms have disclosed board-level climate responsibilities, though that number is rising as investors demand clearer accountability frameworks.

Board Oversight Coverage (2024)

This marks a fundamental pivot in how companies govern risk. As the report notes, climate is now treated not as a "responsibility area," but as an "economic determinant of long-term corporate value."

Shareholders Are Driving the Governance Shift

Shareholder expectations are playing a decisive role. The report highlights that institutional investors, especially pension funds and sovereign wealth funds, are increasingly demanding board-level climate fluency.

Engagements once dominated by questions of earnings performance or capital structure now include scrutiny of climate scenario analyses, transition plans, and governance responses to regulatory risk.

The rise of climate stewardship is one of the clearest market shifts: engagement intensity has increased by 28% in the past two years. Investors are no longer satisfied with ESG checklists. They want decision-useful governance signals, including:

- Climate-linked remuneration

- Disclosure of board expertise in sustainability

- Transparent oversight of lobbying activities

- Integration of climate risk into enterprise-level materiality

The report cites that more than 47% of companies now link executive compensation to climate metrics, up from 32% in 2022. While debates persist about the quality of these metrics, their adoption signals growing investor influence.

Materiality – The New Corporate Battlefield

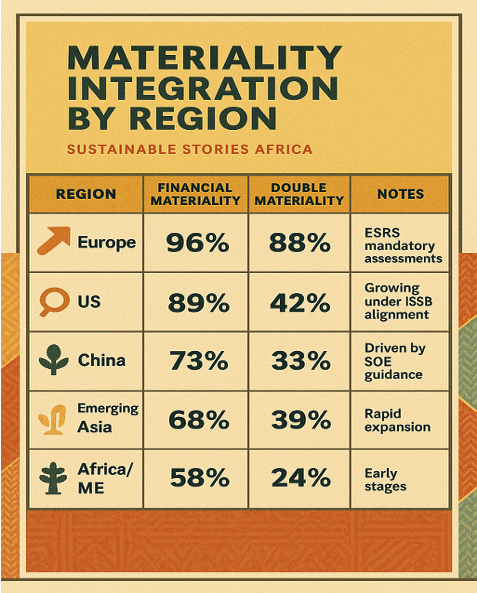

If governance represents the new climate arena, materiality is the playbook. The report notes that double materiality assessments, once largely a European concept, are spreading rapidly across global markets. Over half of the world's large companies now conduct both financial and impact materiality analyses, though the depth varies significantly.

Materiality Integration by Region

| Region | Financial Materiality | Double Materiality | Notes |

|---|---|---|---|

| Europe | 96% | 88% | ESRS mandatory assessments |

| US | 89% | 42% | Growing under ISSB alignment |

| China | 73% | 33% | Driven by SOE guidance |

| Emerging Asia | 68% | 39% | Rapid expansion |

| Africa/ME | 58% | 24% | Early stages |

Materiality has become the interpretive engine through which boards understand climate governance responsibilities. Companies that assess only financial exposure are increasingly viewed as laggards. The report argues that double materiality, evaluating both how climate affects the business and how the business affects climate and society, is critical for credible transition planning.

Governance Is Now a Transition Risk Indicator

The report's most consequential insight is that governance signals are becoming proxies for transition readiness. Companies with strong governance structures tend to:

- Disclose higher-quality emissions data

- Produce more complete transition plans

- Offer clearer CapEx pathways

- Provide better-aligned lobbying disclosures

- Deliver more consistent human-rights and supply-chain reporting

Where governance is weak, disclosure gaps widen and transition claims become harder to verify.

For example, firms with dedicated board climate committees are 2.4 times more likely to disclose Scope 3 emissions and 1.8 times more likely to disclose transition-aligned CapEx. These trends reveal a growing correlation between corporate governance maturity and climate transparency performance.

The Rise of Climate-Competent Boards

Beyond oversight structures, the composition of boards is shifting. The report notes that 29% of companies now have at least one director with explicit climate or sustainability expertise, up by 70,58% from 17% in 2021. However, this remains far below what investors expect, especially in carbon-intensive sectors.

Companies are responding by investing in board training, recruitment of climate-literate directors, and creation of cross-functional climate committees that bridge finance, risk, sustainability, and strategy.

"Climate competence is going from a specialist skill to a baseline expectation," the report states, particularly as litigation, regulatory scrutiny, and investor pressure rise globally.

Lobbying Becomes a Governance Flashpoint

One of the report's strong warnings concerns lobbying alignment. Only 18% of companies disclose climate-related lobbying positions, leaving major gaps in understanding how firms influence policy behind the scenes.

Where there is non-alignment between lobbying activities and climate targets, governance credibility collapses. For boards, this has become a top-tier risk, especially in regulated sectors such as energy, transport, and finance.

PATH FORWARD – Aligning Governance With Climate Reality

Climate governance is no longer optional. It is a core pillar of enterprise value. Boards must integrate climate expertise, materiality assessment, transparent oversight, and lobbying accountability to keep pace with investor and regulatory expectations.

As governance models evolve, companies that embed climate deeply into strategic oversight will lead the transition. Those that treat climate as a compliance issue, not a governance imperative, risk losing both market confidence and long-term relevance.