China is scrapping its value-added tax (VAT) export rebates for solar panels effective April 1, 2026. This ends a decade-long subsidy that helped drive panel prices to historic lows.

The move signals a fundamental reset of the global solar market, closing the era of ultra-cheap Chinese modules that powered energy transitions from Lagos to Lusaka.

For Africa, which sources most of its solar hardware from China, the implications are immediate and far-reaching.

The End of an Era – Cheap Solar Is Over

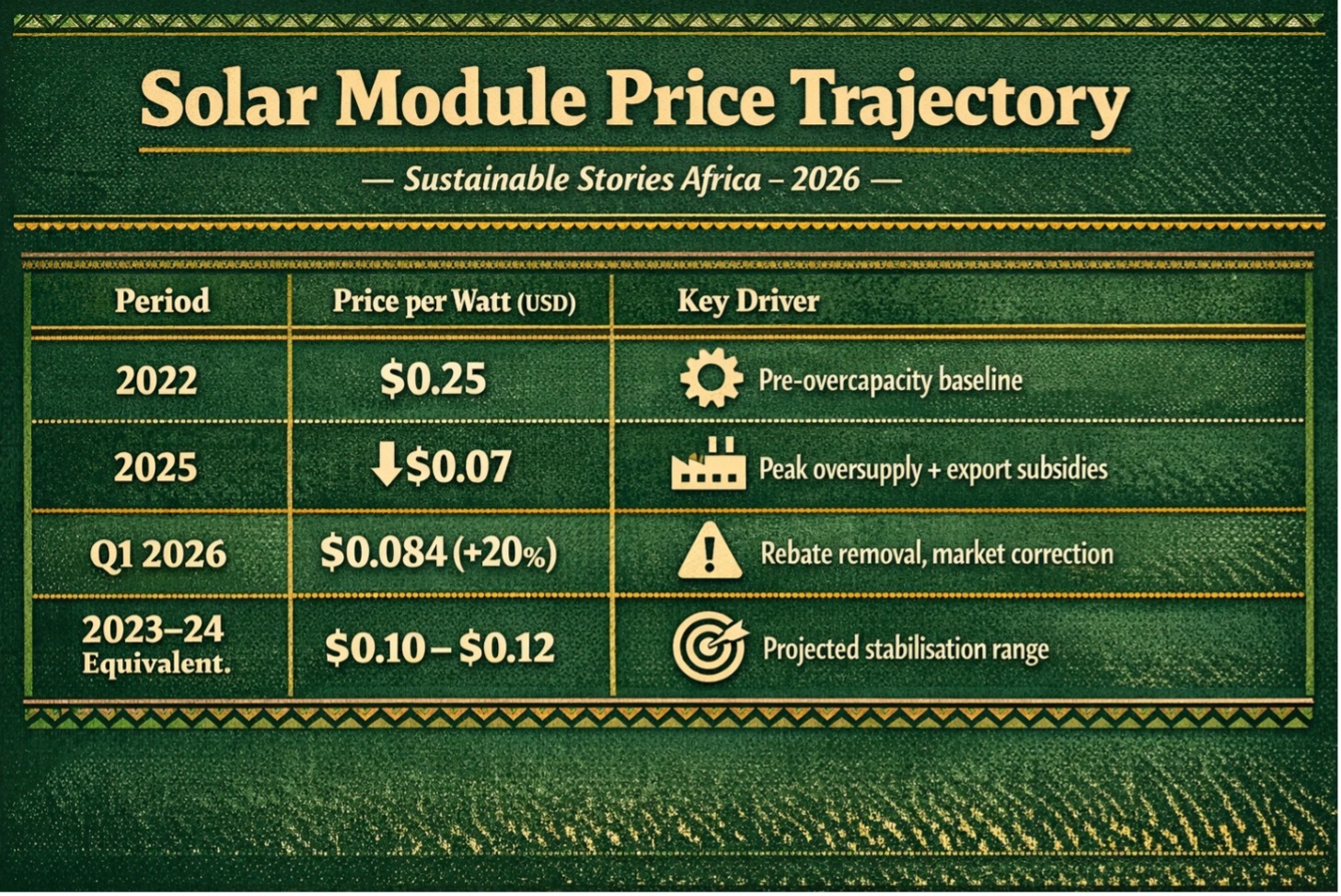

For a decade, China flooded the world with solar panels so inexpensive they seemed almost free. At just $0.07 per watt in 2025, down from $0.25 in 2022, Chinese photovoltaic (PV) modules made renewable energy economically irresistible, from rooftops in Nairobi to utility-scale farms in Morocco.

That era is now ending, and the global south must pay close attention.

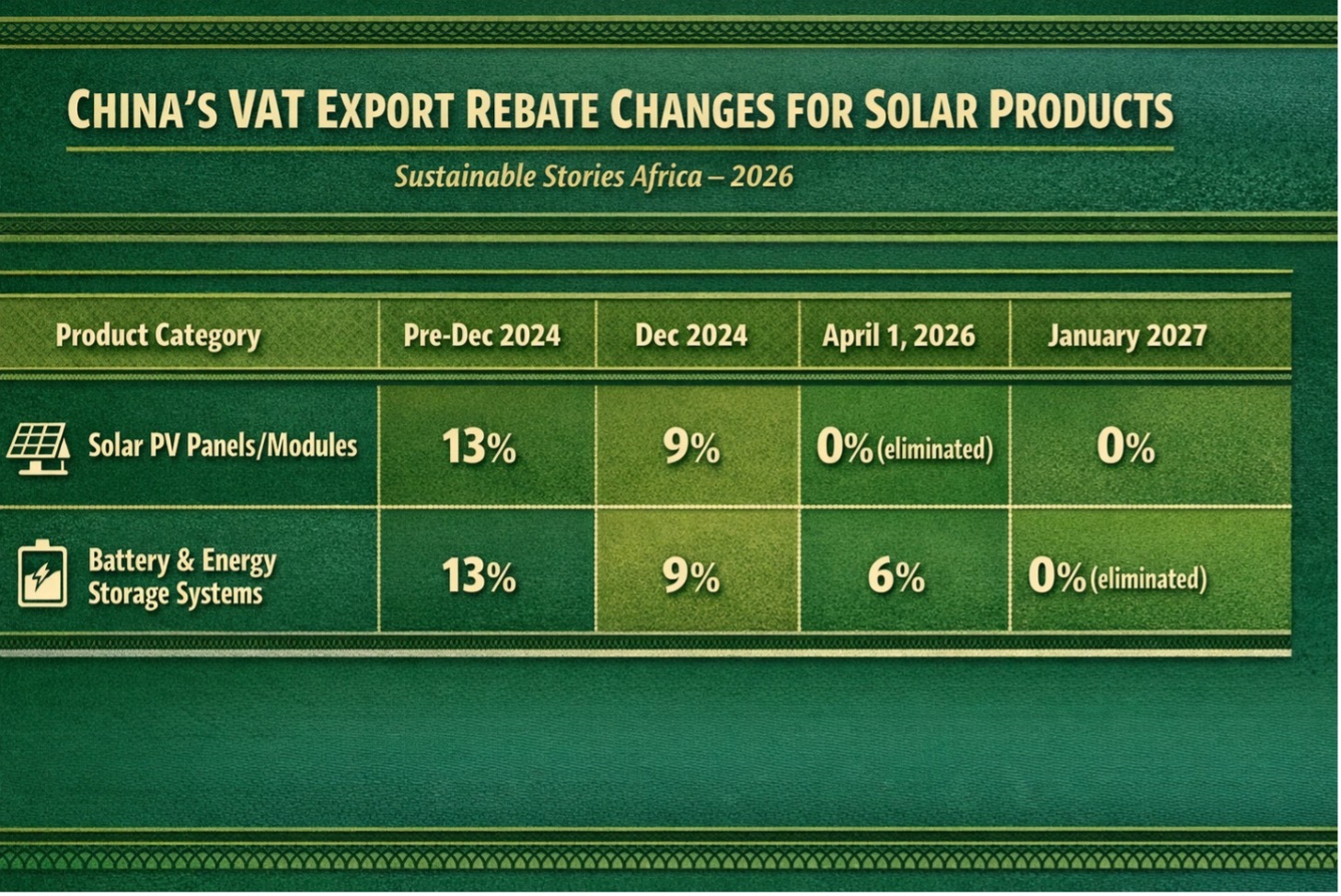

Effective April 1, 2026, China will eliminate its value-added tax (VAT) export rebate for solar panels entirely, cutting it from 9% to zero. For battery storage products, rebates drop from 9% to 6% before being fully withdrawn in January 2027.

The announcement by China's Ministry of Finance and State Taxation Administration represents a decisive industrial policy shift: Beijing is no longer subsidising the world's clean energy transition at its own manufacturing expense.

A Market Forced to Correct Itself

The policy reversal follows years of unsustainable price competition. By 2024, Chinese solar manufacturing capacity was roughly double global demand, triggering losses across major manufacturers, widespread factory closures, and a race-to-the-bottom that threatened the long-term health of the entire industry.

In December 2024, Beijing sent its first signal, reducing PV export rebates from 13% to 9%. The April 2026 abolition completes that trajectory.

The consequences are already materialising. Solar module prices rose approximately 20% during Q1 2026, to levels comparable to the 2023 – 2024 benchmarks.

At the same time, China's newly adopted 15th Five-Year Plan (2026 – 2030) repositions clean energy as "the main source of future power growth" and the foundation of economic restructuring, not merely an export commodity.

China's cumulative wind and solar capacity surpassed 1.8 terawatts (TW) by the end of 2025, with a national target of 3.6 TW by 2035.

For Africa, the timing is uncomfortable. The continent relies heavily on low-cost Chinese imports to close its vast electricity access gaps.

Progressive trade barriers in the US and EU are simultaneously redirecting global demand toward African and emerging markets, compressing supply just as prices climb.

China's VAT Export Rebate Changes for Solar Products

| Product Category | Pre-Dec 2024 | Dec 2024 | April 1, 2026 | January 2027 |

|---|---|---|---|---|

| Solar PV Panels/Modules | 13% | 9% | 0% (eliminated) | 0% |

| Battery & Energy Storage Systems | 13% | 9% | 6% | 0% (eliminated) |

Solar Module Price Trajectory

| Period | Price per Watt (USD) | Key Driver |

|---|---|---|

| 2022 | $0.25 | Pre-overcapacity baseline |

| 2025 | $0.07 | Peak oversupply + export subsidies |

| Q1 2026 | $0.084 (+20%) | Rebate removal, market correction |

| 2023–24 Equivalent | $0.10 – $0.12 | Projected stabilisation range |

A Repricing That Could Unlock Local Industry

While the immediate optics are challenging for solar-dependent economies, the recalibration carries meaningful structural opportunity.

A more rational pricing environment filters out inefficient manufacturers, reinforces quality standards, and creates space for African domestic solar production to become financially viable, something that was near-impossible when Chinese modules sold at or below cost.

If African governments and development finance institutions move swiftly, incentivising local assembly lines, deepening solar financing facilities, and renegotiating supply chain partnerships, this pricing reset could catalyse genuine industrial capacity on the continent.

Countries such as Nigeria, South Africa, Morocco, and Ethiopia, each with nascent solar manufacturing ambitions, are better positioned than many currently recognise.

The transition away from purely import-dependent models is not merely desirable; it is becoming economically necessary.

Act Now or Pay Later

The window to act is open, but it will not remain so for long. African policymakers, institutional investors, and multilateral development banks must move with urgency to:

- Accelerate concessional financing for domestic solar manufacturing and local assembly capacity

- Review import tax structures to prevent compounding cost increases for consumers and project developers

- Unlock blended finance mechanisms to bridge the pricing gap on utility-scale renewable projects

- Engage Chinese manufacturers on long-term supply agreements that buffer price volatility and guarantee technology transfer

The alternative, standing still while global solar economics reshape themselves, risks derailing energy access ambitions for hundreds of millions of Africans still without reliable electricity.

Path Forward – Africa's Solar Sovereignty Moment

China's rebate exit marks more than a market correction; it is a clarion call for Africa to deepen its strategic engagement with renewable energy manufacturing and financing.

Development finance institutions and regional energy bodies must fast-track investment in local solar value chains before the pricing gap widens further.

Governments must revise national energy procurement policies to incentivise local content and unlock blended capital to absorb near-term cost pressures.

With decisive action, this moment of disruption becomes Africa's opportunity to build a solar economy that is resilient, domestically anchored, and globally competitive.

Culled From: China policy shift set to reshape solar market