Climate risk is no longer only a disaster story. It is becoming a household affordability crisis.

A Brookings analysis shows how rising insurance costs can hit hardest where hazard exposure meets low adaptive capacity.

For African markets, the warning is direct: without resilience investment, climate risk can quietly become credit risk, housing stress and deeper inequality.

Insurance Becomes Climate’s Household Shock

The next climate crisis may arrive not as a storm warning, but as an insurance bill a family can no longer afford.

A Brookings Institution analysis published April 16, 2026, warns that rising climate risks are already reshaping housing affordability through the insurance market, particularly for lower-income communities with limited financial resilience.

The report links increasing premiums and policy nonrenewals to a broader structural risk: climate change could deepen existing wealth inequalities by raising the cost of maintaining coverage.

While based on U.S. data, the underlying mechanism is global. As climate shocks intensify, insurers reprice risk, lenders reassess exposure, and vulnerable households bear disproportionate costs.

For African cities and climate-exposed economies, the implication is clear: climate risk is no longer environmental alone; it is financial, systemic, and increasingly central to questions of access, equity, and urban resilience.

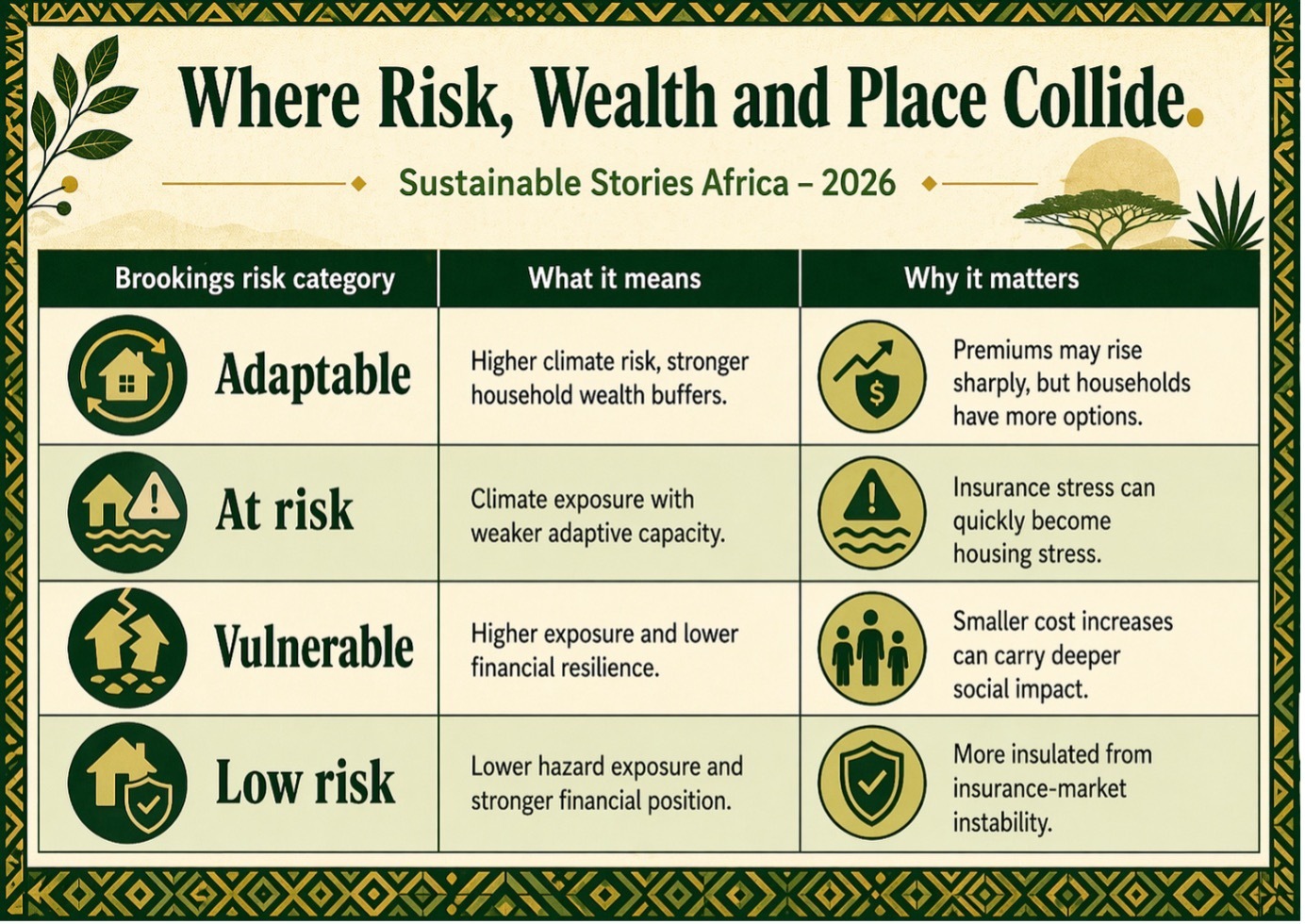

Where Risk, Wealth and Place Collide

Brookings frames “adaptive capacity” as central to how households experience climate risk.

- Higher-income households in hazard-prone areas may absorb rising insurance costs, retrofit properties, or relocate.

- Lower-income households, particularly in flood-exposed communities, face tighter trade-offs: pay more, reduce coverage, or remain exposed to loss.

Drawing on U.S. Treasury insurance data, FEMA’s National Risk Index, and Census demographics, the analysis tracks changes in premiums and policy nonrenewals between 2018 and 2022.

It categorises ZIP codes into “adaptable,” “at risk,” “vulnerable,” and “low risk,” reflecting how climate exposure intersects with income and homeownership.

Premium costs increased most in adaptable areas, up from $204 (10.66%), while in low-risk areas, it went up by $54 (4.02%).

However, smaller increases weigh more heavily in vulnerable communities. Racial disparities are also evident: Black residents are disproportionately concentrated in higher-risk areas, particularly across the U.S. South.

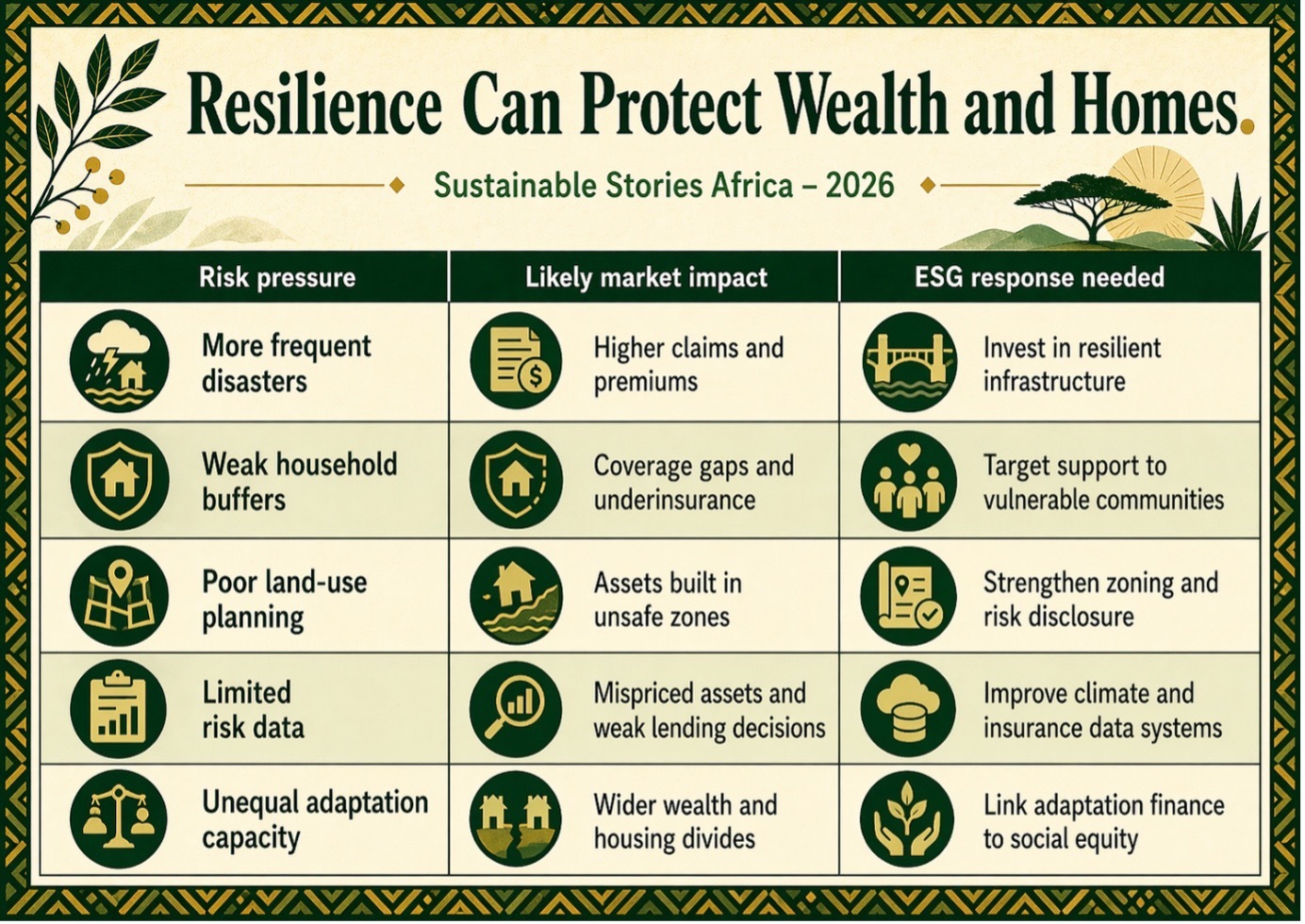

Resilience Can Protect Wealth and Homes

The positive lesson is that insurance stress is not inevitable if governments, financiers and communities reduce underlying risk before disaster strikes.

For Africa, this means treating climate adaptation as an affordability policy, not only an environmental programme.

In Lagos, Accra, Abidjan, Dar es Salaam or Durban, flood exposure is not just a drainage problem.

It can influence access to mortgages, business continuity, household savings, public budgets and investor confidence.

If climate risk is properly priced without resilience investment, insurance becomes expensive or unavailable.

If risk is reduced through better planning, resilient infrastructure, enforceable building standards and targeted support for low-income communities, insurance can remain a tool for protection rather than a signal of exclusion.

The Brookings warning is especially relevant for African financial institutions. Banks, insurers and pension funds cannot treat climate risk as a distant disclosure item.

When homes, farms, warehouses and small businesses become harder to insure, collateral values can weaken, and credit risk can rise.

Make Adaptation a Financial Priority

The urgent action is to move from disaster response to risk reduction.

- Governments should map climate exposure at the neighbourhood level, disclose property-level risk where possible and stop approving development that locks families into future danger.

- Insurers should work with regulators to reward verified risk reduction, not simply withdraw from communities seen as too risky.

- Banks should integrate climate exposure into mortgage and business lending while avoiding blanket exclusion of low-income borrowers.

For African policymakers, this also means building public adaptation finance into national development plans.

Drainage, coastal protection, heat-resilient housing, early warning systems and safer land-use planning are no longer optional public works.

They are tools for protecting household wealth, financial stability and ESG credibility.

- Without intervention, the insurance bill becomes a quiet transfer of climate risk to the people least able to carry it.

- With intervention, it can become a signal that directs capital toward safer homes, stronger cities and more resilient communities.

Path Forward – Build Resilience Before Risk Prices Families Out

Climate insurance stress should be treated as an early warning for housing, finance and social protection systems.

African markets can act now by linking adaptation finance, urban planning, insurance regulation and ESG disclosure.

The goal is simple: reduce the risk before premiums rise beyond reach, and ensure climate resilience strengthens both household security and market confidence.

Culled From: Where rising climate risks and insurance costs will hit hardest | Brookings