ISSB staff have recommended a non-mandatory Practice Statement for nature-related reporting.

The proposal avoids a standalone nature standard while IFRS S1 and S2 adoption continues globally.

For African markets, the decision could shape how companies report biodiversity, water, land and ecosystem risks to investors.

Nature Reporting Faces a Softer Route

The International Sustainability Standards Board’s next big disclosure test may not arrive as a mandatory nature standard, but as a Practice Statement that guides companies without changing the core architecture of IFRS S1 and IFRS S2.

In an April 2026 staff paper, ISSB staff recommended that the board propose disclosure requirements and guidance for nature-related disclosures in the form of an IFRS Practice Statement

They are asking stakeholders to comment on alternative forms of standard-setting in the exposure draft. The paper says the ISSB aims to publish that exposure draft in October 2026.

The recommendation is not a final board decision. But it matters because it could determine whether nature risks, from deforestation and water stress to biodiversity loss and ecosystem degradation, are treated as a voluntary reporting guide or elevated into a standalone global disclosure standard.

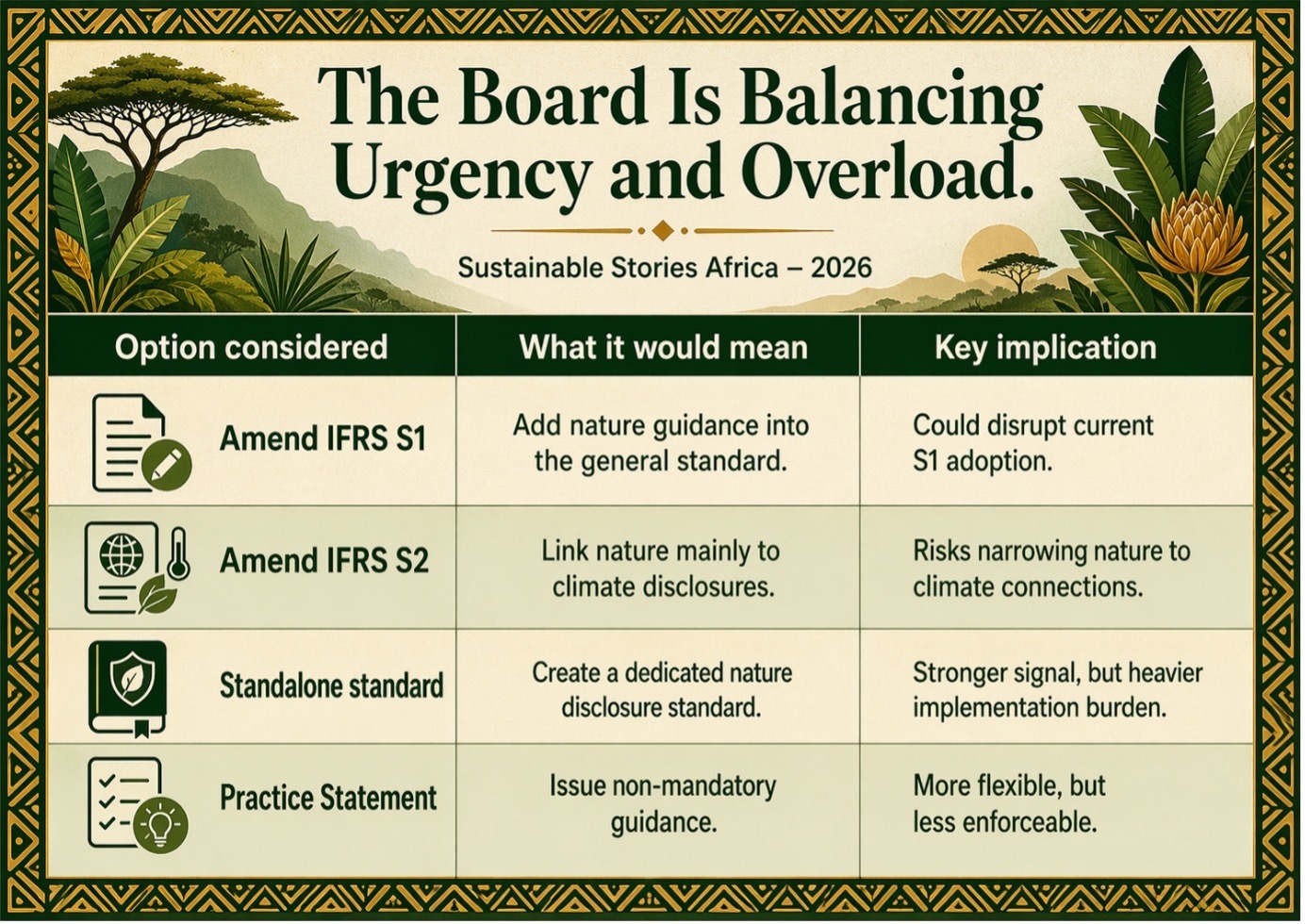

The Board Is Balancing Urgency and Overload

The staff paper frames the choice as a question of sequencing. Many jurisdictions and companies are still adopting IFRS S1, the general sustainability disclosure standard, and IFRS S2, the climate disclosure standard.

ISSB staff said Sustainability Standards Advisory Forum members had urged the board to limit disruption to S1 and S2 implementation while still establishing incremental nature-related disclosure guidance.

The staff considered four routes:

- Adding nature material into IFRS S1

- Adding it into IFRS S2

- Creating a new standalone ISSB Standard

- Issuing a non-mandatory IFRS Practice Statement.

The recommended fourth option would leave S1 and S2 unchanged for now, while giving nature-related financial information more visibility.

The staff recommendation rests on three main arguments:

- Give prominence to nature-related financial information

- Avoid disrupting S1 and S2 adoption

- Allow the ISSB to assess market practice before deciding whether a future standard is needed.

The paper also says a Practice Statement would not prevent the ISSB from publishing nature-related content as a standalone standard or using a follow-up standard.

Better Nature Disclosure Can Protect Capital

For African markets, the stakes are practical. Nature is not a remote environmental category.

It is the water that keeps farms producing, the forests that are in carbon sinks, the wetlands that absorb floods, the fisheries that support coastal livelihoods and the land systems that underpin mining, food, infrastructure and real estate.

A credible nature disclosure framework could help investors understand which companies depend on vulnerable ecosystems, which operations damage natural assets, and which businesses are exposed to water shortages, land-use restrictions, biodiversity regulation or supply-chain disruption.

That is why the debate is already contested. Nature-positive campaigners and sustainability leaders have urged the ISSB to develop a dedicated nature standard, arguing that investors need standardised and comprehensive nature disclosures to support capital allocation decisions.

They also warned that nature and climate actions must be integrated, including the protection of natural carbon stocks and sinks.

African Firms Should Prepare Early

The action point for African companies is clear: do not wait for nature reporting to become mandatory before building the data systems.

Even a non-mandatory Practice Statement can influence investor expectations, lender questions, procurement requirements and assurance practices.

- Boards should ask where the business depends on nature and how it affects nature.

- Banks should identify borrowers exposed to land, water and biodiversity risk.

- Regulators should align early with ISSB, TNFD, GRI and local environmental priorities, rather than allowing fragmented reporting rules to emerge sector by sector.

For companies in agriculture, extractives, banking, energy and infrastructure:

- The first step is to map dependencies and impacts across sites, suppliers and communities.

- The second is turning that map into decision-useful disclosure: what risk exists, how it is governed, what the company is doing, and what financial consequences may follow.

The risk of a soft approach is that nature reporting remains optional until damage becomes costly.

The opportunity is that African institutions can move early, using the ISSB process as a bridge between global investor expectations and local ecological realities.

Path Forward – Make Nature Data Investment-Ready Now

Nature reporting should not wait for perfect rules. African markets need practical disclosure systems that connect biodiversity, water, land use and ecosystem risk to finance, strategy and community resilience.

The priority is early preparation: stronger data, board oversight, sector guidance and investor-ready reporting.

Whether ISSB chooses a Practice Statement or a future standalone standard, companies that understand their nature risks first will be better placed to protect value and attract capital.

Culled From: ISSB Staff Recommend Practice Statement for Nature Reporting Instead of Standalone Standard