ESG audits are moving closer to the corporate mainstream.

That matters now as disclosure rules, assurance standards and investor expectations tighten across global and African markets.

For companies, the real question is no longer whether sustainability data exists, but whether it can withstand scrutiny.

ESG claims now need proof

An ESG audit is fast becoming one of the clearest tests of whether a company’s sustainability claims are real, measurable and decision-useful.

The shift is driven by increasing regulatory pressure, stronger investor expectations and the spread of assurance-ready sustainability reporting frameworks.

OneStop ESG’s explainer frames the audit as a structured review of ESG data, controls, policies and performance, at a time when businesses are being pushed to show evidence rather than ambition alone.

For African companies, that change lands at a delicate moment. Many firms are still building reporting systems; however, capital providers, lenders, customers and regulators increasingly expect sustainability information to carry the same discipline as financial information.

IFRS S1 is effective for annual reporting periods beginning on or after 1 January 2024, while the IAASB’s ISSA 5000 was issued as a stand-alone global sustainability assurance standard and is effective for reporting periods beginning on or after 15 December 2026.

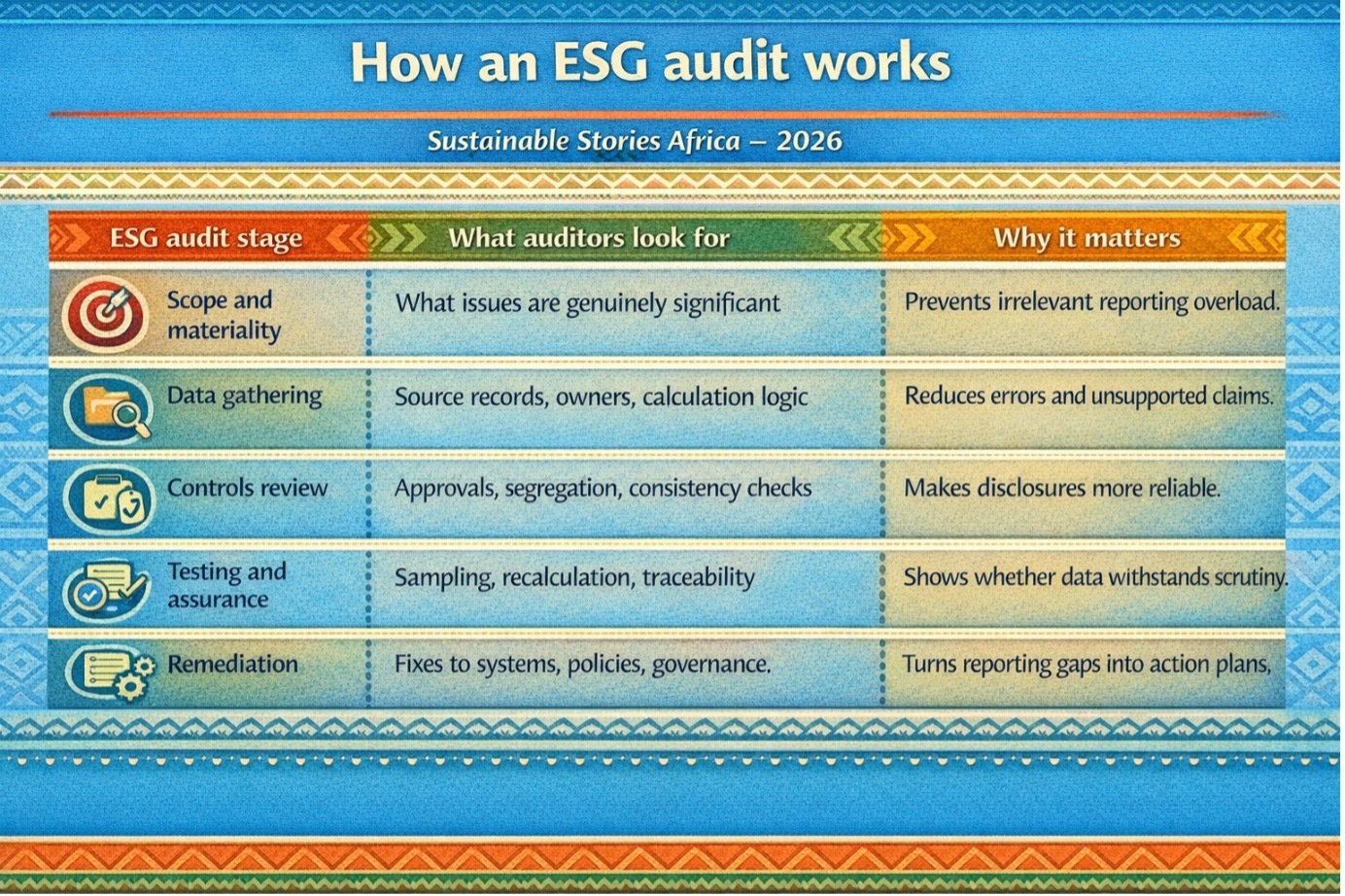

How an ESG audit works

At its core, an ESG audit asks a simple question: can the company prove what it says? That means checking whether emissions, water, waste, labour, safety, governance and risk-management disclosures are supported by source documents, consistent methodologies, internal controls and clear ownership.

OneStop ESG’s wider content on reporting systems repeatedly points to the same operational foundation: evidence repositories, version control, audit trails and sign-offs are becoming essential, not optional.

In practical terms, the audit process usually starts with scope and materiality, then moves through data collection, control testing, evidence review, gap identification and remediation.

The distinction between limited and reasonable assurance is also important. Limited assurance tests whether anything suggests a material misstatement, while reasonable assurance is closer to a financial audit, with deeper testing of methodologies and source data.

That matters especially in African and Global South markets, where many ESG risks are operational before they are reputational. A food processor facing water stress, a bank exposed to climate-vulnerable sectors, or a manufacturer dependent on diesel backup power cannot treat the audit as a branding exercise.

The process may reveal that the biggest weakness is not the narrative in the report but the weak data plumbing behind it.

What companies gain by preparing early

The upside of getting ready for an ESG audit is greater than compliance.

A company that can identify its emissions data, explain its safety records, verify supplier controls and document governance decisions is better placed to earn trust from investors, development finance institutions and multinational customers.

It is also better prepared for anti-greenwashing scrutiny and for the growing expectation that sustainability data should be decision-grade.

Preparation can also make businesses more resilient internally. Audit readiness forces teams to clarify roles, clean up data flows, tighten controls and connect sustainability reporting to risk, finance and operations. In many firms, that process reveals hidden inefficiencies: missing metering, inconsistent supplier data, fragmented HR records or unclear board oversight. Fixing those gaps can improve management quality long before the external auditor arrives.

The cost of inaction is equally clear. Companies that publish ambitious ESG claims without robust evidence risk restatements, reputational damage, weaker access to capital and loss of commercial credibility. In a tougher financing environment, that can become a material business risk.

Build audit readiness before rules harden

The message for boards and executives is straightforward: start before the mandate arrives.

- Companies should identify their most material ESG topics, assign accountable owners, document methodologies, centralise evidence and run internal readiness reviews.

- Internal audit teams should be brought in earlier, not at the end, especially as ESG and audit functions are increasingly expected to work together on controls, assurance and integrity.

- For regulators, advisers and market institutions in Africa, the task is to make this transition practical. That means building skills, creating proportionate pathways for smaller firms and encouraging assurance approaches that reflect local data realities without lowering standards.

The real goal is not perfect paperwork. It is credible sustainability information that supports better corporate decisions.

Path Forward – From claims to tested credibility

African firms will need to treat ESG audits as part of mainstream corporate readiness, not a specialist side project.

The work starts with better systems, clearer accountability and stronger internal controls.

As assurance standards mature and scrutiny rises, the companies that prepare early will be better placed to protect trust, attract capital and prove that sustainability reporting stands up to real examination.

Culled From: ESG Audit: What It Is, How It Works, and How to Prepare for One | OneStop ESG