Asia’s LNG confidence is being shaken by the war in Iran, as disrupted Gulf supply routes expose the risks of dependence on imported gas.

The shock matters because LNG was marketed as a cleaner, flexible bridge fuel for fast-growing economies.

For Africa, the lesson is urgent: energy security must mean diversified power, local resilience, and affordable transition planning.

Attention: LNG’s Security Promise Faces New Stress

The Iran conflict is exposing a critical vulnerability in Asia's energy transition strategy. Liquefied natural gas, long positioned as a practical bridge from coal to cleaner electricity, is revealing its limits as a reliable option for import-dependent economies.

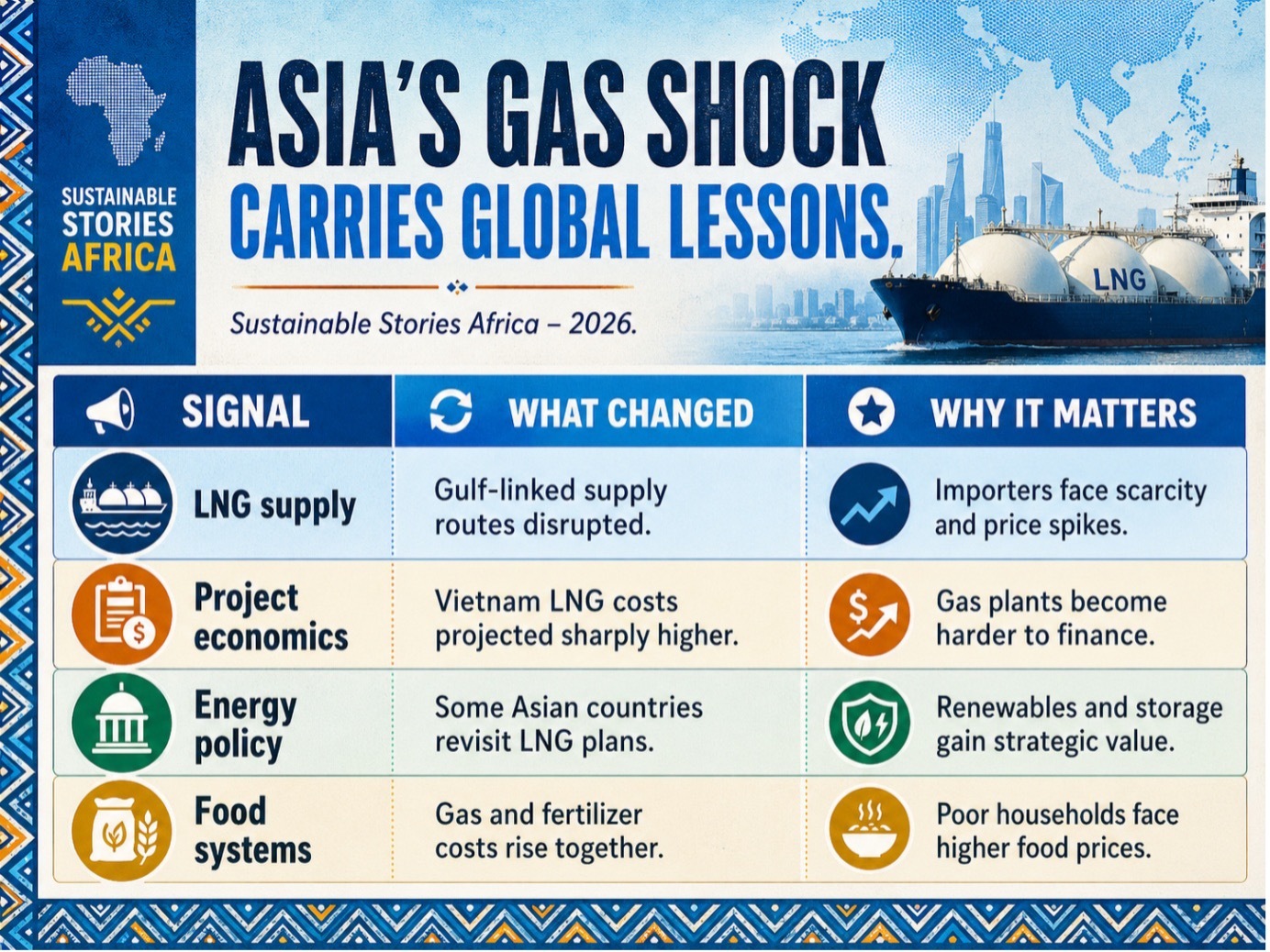

Asian LNG imports fell sharply in March 2026 after hostilities in the Middle East disrupted supply from Qatar and the UAE, two suppliers that together control roughly 20% of global LNG flow through the Gulf.

The consequences came quickly on project economics. Vietnam's Vingroup, developing an LNG-to-power facility in Haiphong, saw projected annual fuel costs surge from approximately $3.5 – $3.8 billion to over $5.4 billion under conflict-driven pricing.

For African markets watching from the sidelines, the lesson carries weight. Importing energy is not assessed by emissions.

Affordability, foreign-exchange exposure and supply security determine whether an energy system truly serves its people or creates a different kind of dependency.

Asia’s Gas Shock Carries Global Lessons

The Strait of Hormuz sits at the heart of this unfolding crisis. Described by UN Trade and Development as one of the world's most critical maritime chokepoints, it carries roughly a quarter of global seaborne oil trade with significant LNG and fertiliser volumes.

Its disruption has pushed energy prices, freight costs, insurance premiums and food prices well beyond the Gulf region.

IEEFA argues the conflict has already eroded LNG's reputation as an affordable, secure long-term energy source.

Asian economies have responded by leaning on coal and nuclear infrastructure while accelerating renewables, storage and efficiency investments.

The consequences are more far-reaching than energy markets. A factory owner in Lagos, a maize farmer in Kenya or a cold-chain operator in Ghana may never purchase Gulf LNG directly; however, they live within systems shaped by global fuel, fertiliser and freight costs.

UNCTAD warns that developing economies carrying high debt and limited fiscal space face the sharpest exposure to these cascading shocks.

The Atlantic Council’s analysis adds an African dimension: the war is worsening fuel and fertiliser pressures, even as it may create openings for African energy producers and infrastructure investors.

It notes that countries such as Ethiopia, Kenya, Mauritius and South Sudan are already experiencing fuel shortages, while refining-constrained economies, including Ghana, South Africa and Nigeria, face additional pressure.

Resilience Can Become Africa’s Advantage

The positive lesson is not that African countries should reject gas outright. It is that gas must be planned with discipline, transparency and resilience.

Africa’s energy transition cannot be built on a single narrative of imported fuel. LNG may still support grid stability, industrial heat and flexible generation in some markets.

However, the Iran-war shock shows why long-term strategies must also prioritise solar, wind, hydro, geothermal, storage, regional power pools, efficiency and domestic value chains.

- For African governments, the better future is one where energy security is not held hostage by foreign-exchange shortages or distant chokepoints.

- For utilities, it means procurement plans that test fuel-price volatility before projects are approved.

- For investors, it means financing assets that remain viable under stress.

- For citizens, it means fewer blackouts, lower exposure to imported inflation and stronger protection for food systems.

This is the succour Africa can draw from Asia’s crisis: a chance to design energy systems that are not merely cleaner, but sturdier.

Build Energy Systems That Withstand Shocks

The next step is policy clarity. African energy ministries, regulators and development finance institutions should treat the Iran-LNG shock as a planning signal, not a distant headline.

Every major gas-to-power project should be tested against three questions.

- Can the country afford the fuel during a crisis?

- Can the grid absorb cheaper renewables and storage at scale?

- Can the project strengthen, rather than weaken, food security, public finances and industrial competitiveness?

Development banks should align support with resilience. That means funding transmission lines, battery storage, clean cooking, distributed solar, regional interconnectors and transparent gas infrastructure that will meet credible affordability and transition tests.

Businesses also have a role. Manufacturers, telecoms, agribusinesses and logistics firms should reduce diesel and gas exposure through efficiency, captive renewables and smarter power procurement.

Citizens need reliable public communication, not panic. Energy transition is no longer only about carbon; it is about economic survival.

Path Forward – Resilience Must Lead Energy Planning

Africa should use Asia’s LNG shock to strengthen energy planning, not delay transition.

The priority is diversified power: renewables, storage, efficient grids, responsible domestic resources and regional trade.

The promise is practical ESG: lower volatility, better household protection, stronger food systems and investable infrastructure.

The lesson from the Iran war is simple, energy security must be local, flexible and future-ready.

Culled From: Iran war is undercutting the role of LNG in Asia - Climate and Capital Media