Africa's capital markets have expanded steadily over the past two decades, yet they remain marginal players in global finance.

Equity, bond, and institutional markets are growing, however, too slowly, too narrowly, and too unevenly to meet the continent's development needs.

An OECD report reveals why: fragmented markets, shallow investor bases, weak governance, and rising debt costs continue to constrain Africa's ability to mobilise long-term capital for growth, climate transition, and resilience.

Capital Without Scale, Markets Without Depth

Africa's capital markets are no longer absent; however, they are insufficient. Over the past 25 years, African economies have developed their stock exchanges, issued sovereign and corporate bonds, and introduced governance reforms, which are designed to attract investment. Market capitalisation has risen sharply, and digital finance has expanded access at the retail level.

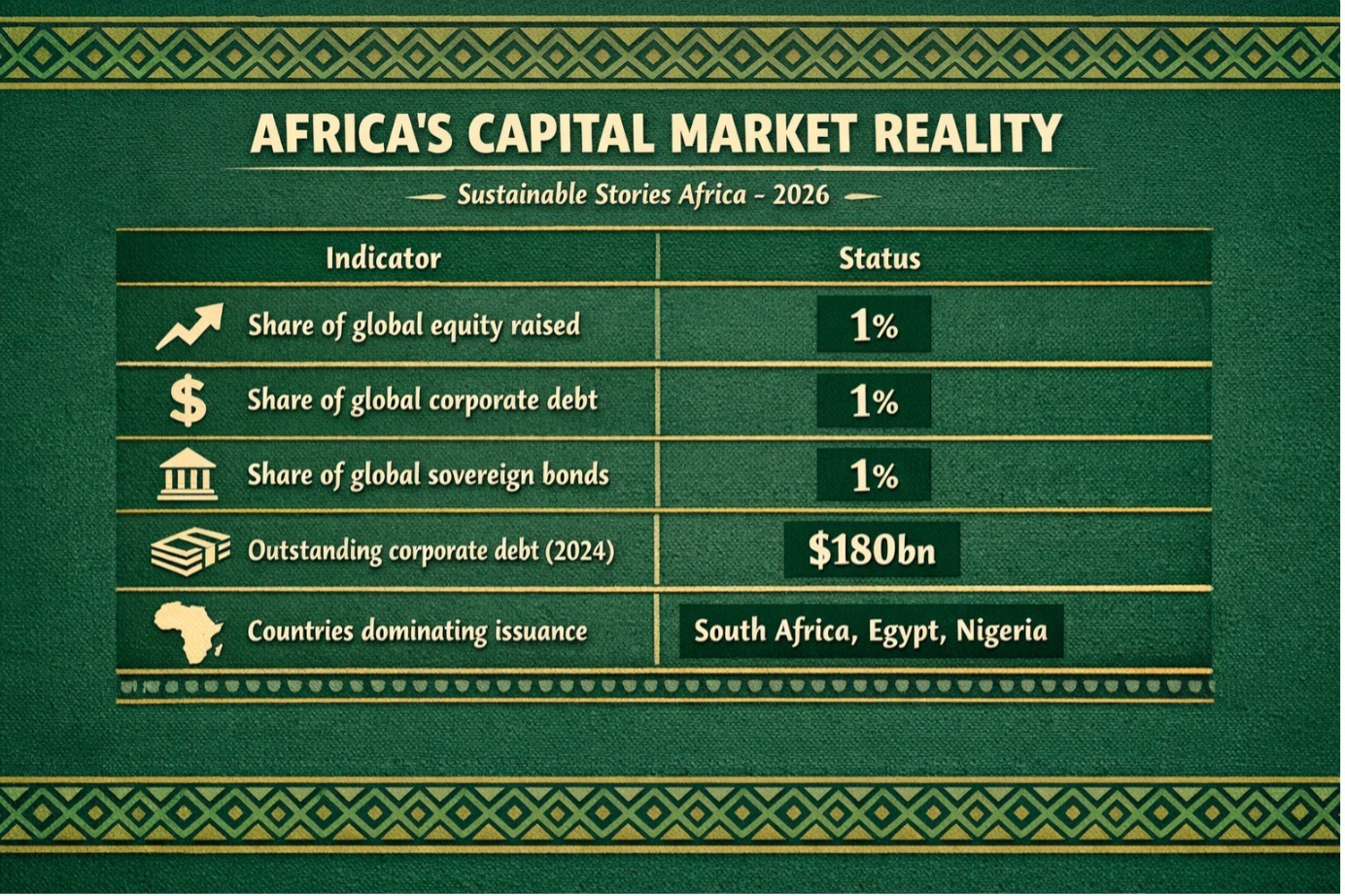

However, the numbers tell a more restrained story. According to the Africa Capital Markets Report 2025, the continent accounts for just 1% of global equity raised, 1% of global corporate debt, and 1% of sovereign bond markets, despite representing roughly 3% of global GDP. Capital market activity remains concentrated in a handful of countries, with South Africa, Egypt, and Nigeria dominating issuance and liquidity.

This mismatch between ambition and capacity matters more than ever. As public finances tighten, climate investment needs rise, and bank-based lending reaches its limits, Africa's ability to finance its future increasingly depends on whether its capital markets can finally deepen, diversify, and deliver.

A Continent Financing Growth the Hard Way

Africa's economies are growing, urbanising, and digitising; however, they are doing so with capital markets that remain structurally underpowered. While equity market capitalisation reached approximately $561 billion by 2024, this represents a fraction of what comparable emerging markets have achieved. Corporate bond markets have stagnated, and outstanding corporate debt has fallen from $230 billion in 2020 to $180 billion in 2024.

The result is a financing ecosystem still dominated by bank lending, sovereign borrowing, and foreign capital, each having its limits. Rising sovereign issuance has increasingly crowded out private credit, while dependence on foreign-currency debt has amplified vulnerability to global interest-rate cycles and capital outflows.

In short, Africa is financing long-term development with short-term instruments and paying a premium for it.

Where Africa's Capital Markets Are Falling Short

Equity Markets: Size Without Liquidity

African stock exchanges have expanded in number, but not in depth. Companies have raised around $220 billion in equity over 25 years, yet trading activity remains thin and heavily concentrated. High transaction costs, low free-float ratios, and limited retail participation have left most exchanges illiquid and unattractive to new issuers.

Corporate ownership is also highly concentrated. Corporations own 24% of listed equity in Africa, compared with 19% in emerging markets and 9% globally, raising concerns about minority shareholder protection and governance standards.

Corporate Debt: A Narrow and Risky Market

Africa's corporate debt markets remain shallow, fragmented, and exposed to currency risk. Bonds and syndicated loans account for a small share of corporate financing, and issuance is concentrated in just four countries. Much of this debt is denominated in foreign currency, exposing firms to exchange-rate volatility and refinancing risk.

This structure limits long-term investment in infrastructure, manufacturing, and energy sectors that require patient capital rather than short-term bank loans.

Sovereign Bonds: Growing, But Costly

Sovereign bond markets have expanded over the past two decades, yet Africa still represents only 1% of global sovereign bonds. Since 2022, rising global interest rates and weakening foreign demand have pushed borrowing costs higher. Average real yields on local-currency bonds are around 5%, while USD-denominated bonds carry nominal yields near 9%.

These costs ripple through the financial system, raising corporate borrowing costs and tightening credit conditions across economies already facing fiscal pressure.

Institutional Investors: The Missing Anchor

Pension funds and insurance companies, one of the cornerstones of capital markets elsewhere, remain underdeveloped across much of Africa. Limited assets, conservative allocation rules, and heavy exposure to government securities restrict their ability to act as long-term investors.

Without stronger institutional investors, markets remain volatile, shallow, and overly dependent on foreign capital.

AFRICA'S CAPITAL MARKET REALITY

| Indicator | Status |

|---|---|

| Share of global equity raised | 1% |

| Share of global corporate debt | 1% |

| Share of global sovereign bonds | 1% |

| Outstanding corporate debt (2024) | $180bn |

| Countries dominating issuance | South Africa, Egypt, Nigeria |

What Deeper Markets Could Unlock

If Africa's capital markets functioned at scale, the gains would be transformative. Deeper markets could mobilise domestic savings, reduce reliance on foreign-currency debt, and provide long-term financing for climate transition, infrastructure, housing, and innovation.

The report estimates that meeting Africa's climate and energy transition goals alone will require doubling current investment levels. Capital markets; particularly sustainable bonds and equity financing are uniquely positioned to bridge this gap, especially if regional integration expands investor pools and liquidity.

Stronger markets would also support financial inclusion, allowing households and pension contributors to participate directly in national growth rather than remaining passive savers.

Reform Is No Longer Optional

The OECD's message is clear: incremental reform is insufficient. To unlock capital markets as engines of development, African policymakers must act decisively on multiple fronts:

- Strengthen corporate governance, especially minority shareholder protection

- Develop local-currency bond markets to reduce FX risk and debt vulnerability

- Expand institutional investor participation, particularly pensions and insurance

- Lower transaction costs and digitise infrastructure

- Accelerate regional market integration, including exchange linkages

- Reform SOE governance to unlock listings and transparency

Without these changes, capital markets will remain peripheral; that is, they are present, but not powerful.

PATH FORWARD: Building Markets That Finance Africa

Africa does not lack capital. It lacks capital at scale, at duration, and at home. The path forward lies in aligning governance, regulation, and technology to convert savings into long-term investment.

Regional integration, domestic institutional investors, and credible governance frameworks must become the backbone of Africa's financial architecture.

Capital markets are not a shortcut to development. But without them, Africa's growth ambitions will remain constrained by cost, volatility, and dependence.