Africa’s critical minerals moment is being framed as a green opportunity; however, raw extraction alone will not deliver green industrialisation. The real debate is whether the continent will supply the transition or shape it.

Our view at SSA is clear: African governments should treat critical minerals as leverage for value addition, regional integration and fairer partnerships.

That matters now because global supply chains are being rewritten, and late negotiators will inherit the weakest terms.

Africa Cannot Export Its Future Anymore

Critical minerals are now central to the politics of climate, trade and industrial strategy. The Southern Transitions paper makes the point plainly: Africa holds substantial reserves and production across several transition-relevant minerals; however, much of the continent still sits in the lower-value end of global supply chains, exporting raw or minimally processed material while others capture the higher-value processing and manufacturing stages.

The real issue is not whether Africa has minerals. It is more about whether African countries can use this moment to build a cleaner industry, better infrastructure, stronger fiscal capacity and more resilient jobs, rather than deepen an old extractive model under a new green label.

This is now an ESG, climate and governance question as much as a mining one. Supply-chain security, due diligence, localisation, benefit-sharing, industrial policy and community safeguards are colliding in a single debate.

If Africa negotiates badly, the energy transition could reproduce familiar asymmetries. If it negotiates well, critical minerals could become a platform for green industrialisation rather than another chapter of export dependence.

The quarry model is the wrong model

Africa has a narrow window to avoid becoming merely the green economy’s extraction base.

The central argument is that critical minerals should serve industrial transformation, rather than become an end in themselves.

Every mining licence, corridor project, strategic partnership and development-finance package should be assessed by whether it leaves behind more domestic processing, more reliable power, stronger skills, more local firms, greater public revenue, and better environmental and social safeguards.

If it does not, the activity may be commercially viable but developmentally weak.

The report’s visuals reinforce that risk. They show how uneven Africa’s leverage remains across minerals and countries, and how export flows still depend heavily on external processing hubs, especially China.

The message is clear: Africa is central to the global transition; however, it is not positioned to capture enough industrial value.

High demand alone will not guarantee structural gains. Without deliberate policy and stronger bargaining, it could instead deepen extraction, volatility, environmental strain and weak value capture.

Africa’s leverage is real, but uneven

One of the paper’s strongest interventions is its refusal to reduce Africa to a single narrative of critical minerals.

On pages 10 to 13, it shows that only a relatively small group of African countries are globally significant producers, and that most occupy narrow, mineral-specific positions within value chains.

- South Africa stands out in manganese, platinum-group metals and chromite

- DRC is central to cobalt and significant in copper

- Morocco is strategic in phosphate

- Guinea is a major bauxite producer

- Gabon, Mozambique and Zambia play more specialised roles.

The message is important: Africa’s mineral endowment is not uniform, and neither are the opportunities it creates.

That matters because strategy should follow structure. Countries with a large market share face different policy choices from those with smaller but still important deposit bases.

In the same way, countries with renewable-energy potential, port access or strong regional trade links have different industrial pathways from those constrained by weak electricity systems or logistics bottlenecks.

The paper’s central argument is that Africa’s minerals landscape is heterogeneous, and policy must reflect that reality rather than rely on a one-size-fits-all model.

On pages 17 to 20, the report shows that Africa’s policy architecture is already more developed than many outsiders assume.

It highlights the:

- The African Green Minerals Strategy

- The Africa Mining Vision

- The national or regional initiatives in Zambia, Ghana, Zimbabwe, SADC and ECOWAS.

The problem is not the absence of ideas. It is that implementation, coordination and finance still lag behind ambition.

That gap becomes even clearer on pages 22 to 24, where the paper argues that many external initiatives still begin from supply security rather than African industrial transformation.

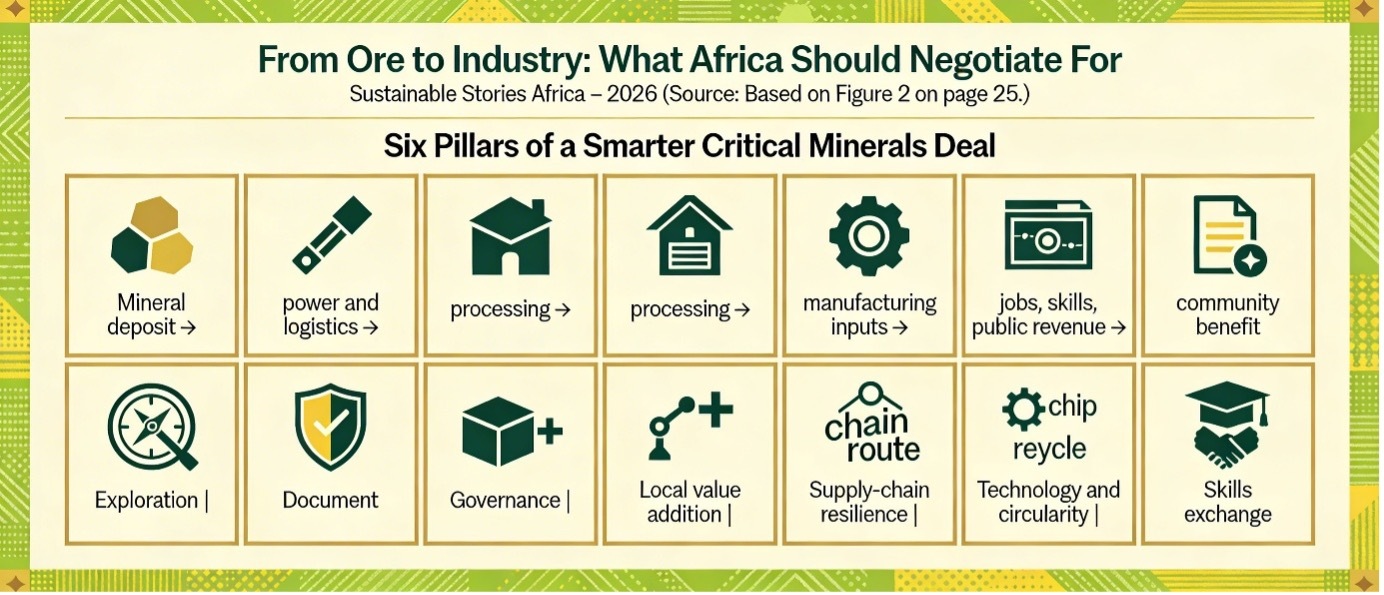

This is why the G20 Critical Minerals Framework matters.

Its six pillars, shown in Figure 2 on page 25:

- Link supply security to governance

- Local value addition

- Resilient supply chains, innovation

- Circularity and skills exchange.

The country examples bring those stakes into focus.

- Guinea’s bauxite model shows the limits of raw-export dependence, with more than 90 per cent of exports going to China.

- The DRC – Zambia corridor points to the promise of regional industrial alignment

- Morocco shows how state coordination can turn minerals into broader capability

- Zimbabwe and Namibia’s lithium pathways reveal both upgrading potential and the risks of poorly governed acceleration.

These shifts are drawn from the report’s policy analysis and pathway chapters, pages 13–20, 25–37.

What Africa could gain from negotiating differently

Picture the alternative the paper points to.

- A bauxite-rich country moves beyond shipping raw ore and uses renewable-energy investment, grid planning and industrial finance to expand into alumina and aluminium-linked manufacturing.

- A copper-cobalt belt becomes more than an extraction corridor, developing battery precursors, engineering skills, grid equipment and transport infrastructure.

- A phosphate economy grows beyond rock exports into fertiliser, food-security resilience, research and low-carbon industry

- A lithium producer pairs investment with processing, environmental safeguards and local enterprise growth.

That future would reshape more than trade statistics. It would reduce exposure to raw commodity volatility, deepen local supplier networks and increase the likelihood that communities see jobs, services and infrastructure rather than only disruption.

It would also make Africa a stronger long-term partner for investors and manufacturers.

The just-transition lens is central here. The paper argues that cooperation is shaped by

- Who sets the rules

- Bears the risks

- Captures the gains.

A minerals boom that deepens inequality or externalises environmental damage is not green industrialisation. It is an extraction with cleaner branding.

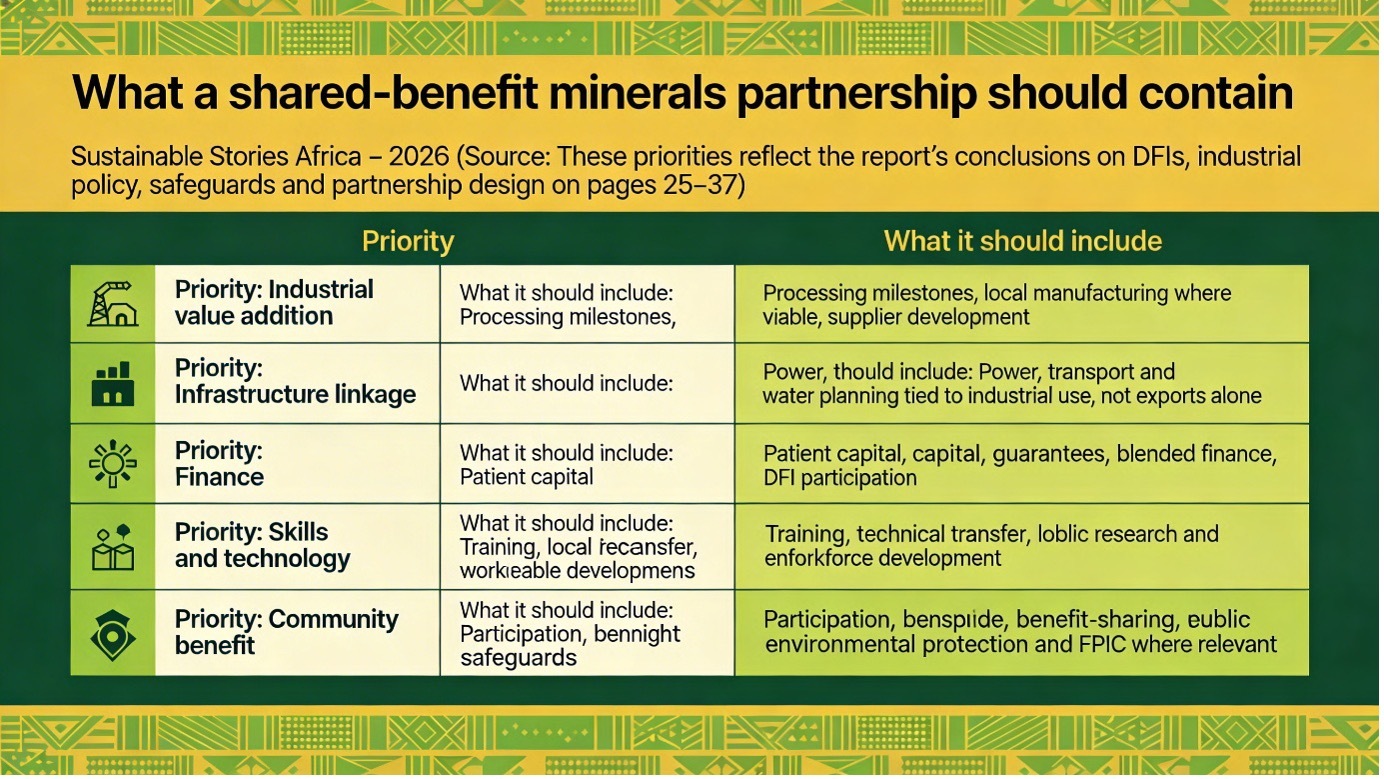

The next deals must be negotiated differently

- First, the report argues that African governments need mineral-specific industrial strategies rather than generic resource nationalism. Copper-cobalt, bauxite, phosphate and lithium each come with different processing economics, infrastructure needs, market structures and bargaining realities. Policy must reflect those differences if countries want to capture more value.

- Second, regional coordination has to move beyond conference language into transaction design. The report shows that some value chains become viable at the corridor or regional scale. That means aligning cross-border power systems, rail and port infrastructure, customs rules, industrial zones and procurement strategies so neighbouring countries can climb together rather than competing for the same low-value position.

- Third, on pages 25 and 26, the report is especially clear about the role of development finance institutions. DFIs are uniquely placed to absorb public risk, de-risk early-stage projects and link finance to broader public value. That means moving beyond extract-and-export financing towards models that support local processing, jobs, community benefit and measurable social returns.

- Fourth, the paper argues that standards must go beyond traceability. ESG compliance matters, but it should also be tied to localisation, labour conditions, environmental performance, community participation and equitable benefit-sharing. Otherwise, standards risk disciplining producers without changing who captures value.

- Fifth, the report says critical minerals should be treated as a public-development issue, not just a technical mining file. Citizens, communities, journalists and civil society all have a role in testing whether benefits, safeguards and trade-offs are clearly defined. The most durable industrial strategy will be one that can withstand public scrutiny and retain legitimacy over time.

Path Forward – Africa Must Negotiate Up the Chain

Africa does not need a bigger role in extraction alone. It needs a stronger role in processing, technology, skills, infrastructure and rule-setting.

That is where green industrialisation begins.

The next phase should be clear: negotiate mineral deals around shared benefit, back them with regional coordination and DFI capital, and measure success by what stays in African economies after the ore leaves the ground.