Malawi’s reform moment has arrived under pressure, not prosperity. With inflation near 30%, exports shrinking and reserves critically low, the country faces a narrowing window to restore macroeconomic credibility.

The World Bank’s latest assessment warns that without decisive fiscal, trade and exchange-rate reforms, Malawi risks entrenching instability.

However, within the perceived crisis lies an opportunity: a chance to rebuild competitiveness, unlock exports and reset growth foundations.

Stability Before Growth: Malawi’s Reform Imperative

Malawi’s economy is not collapsing. But it is steadily constricting under the weight of imbalances.

Real GDP grew just 1.9% in 2025, below the population’s 2.6% growth, marking a fourth consecutive decline in per capita income.

Inflation averaged 28.4%, the highest in the region. Fiscal deficits have averaged 10.9% of GDP since 2022

The current account deficit is approaching 20 % of GDP.

These are not isolated statistics. They form a reinforcing cycle.

High deficits drive domestic borrowing. Domestic borrowing crowds out private credit.

Foreign exchange shortages intensify. The exchange-rate premium between official and parallel markets is over 140%, distorting incentives.

Exporters lose competitiveness as imports surge. Reserves fall below one month of import cover.

The result is a credibility deficit layered atop a fiscal one.

Malawi’s challenge, therefore, is not simply growth; it is restoration.

Imbalances Now Threaten Structural Stability

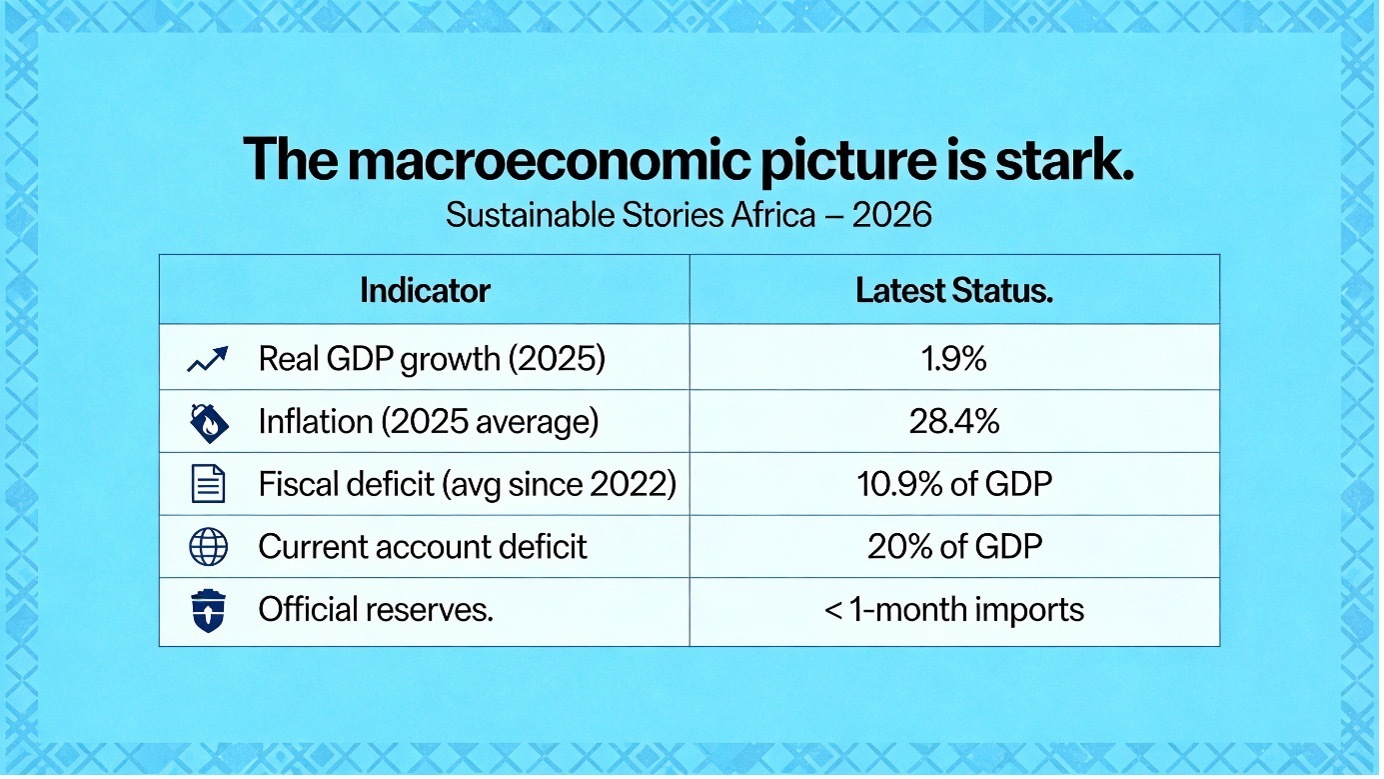

The macroeconomic picture is stark.

Indicator | Latest Status |

|---|---|

Real GDP growth (2025) | 1.9% |

Inflation (2025 average) | 28.4% |

Fiscal deficit (avg since 2022) | 10.9% of GDP |

Current account deficit | 20% of GDP |

Official reserves | < 1-month imports |

Agriculture absorbs over 10% of the national budget; however, maize yields average just 2.1 metric tons per hectare, half the national target.

Fertiliser subsidies have failed to deliver sustained productivity gains.

Meanwhile, only 6% of firms export directly. Most operate below 50% capacity due to fuel, forex and policy constraints.

The problem is not effort. It is the structure.

Exports Reveal Deeper Policy Fractures

Exports are Malawi’s pressure gauge, and they are flashing red.

After rising in the early 2000s, exports as a share of GDP have fallen back to two-decade lows. Tobacco still accounts for 61% of goods exports in 2024.

The number of product categories exported has dropped from 1,070 in 2010 to 634 in 2024.

Export participation is thin: 3.2 exporters per 100,000 inhabitants compared to an average of 28 across Africa.

This is not simply a diversification failure. It is a policy signal.

Non-tariff barriers, export licensing delays averaging four weeks, mandatory forex surrender requirements and ad hoc trade restrictions raise costs.

Each additional day at the border reduces trade by more than 1%, according to the report’s analysis.

Macroeconomic instability compounds the problem. An overvalued official exchange rate reduces exporters’ returns while subsidising imports.

The vicious cycle becomes clear:

Until this loop is broken, growth will remain consumption-driven and fragile.

Debt, Deficits and Export Concentration - Fiscal and Debt Pressures

Public debt has risen significantly over the past two decades. Nearly half of domestic revenue now goes toward interest payments.

Domestic banks hold large shares of government securities, crowding out private-sector lending.

While banks remain profitable, with ROE at 60.9%, this strength is tied to government paper, not productive credit expansion.

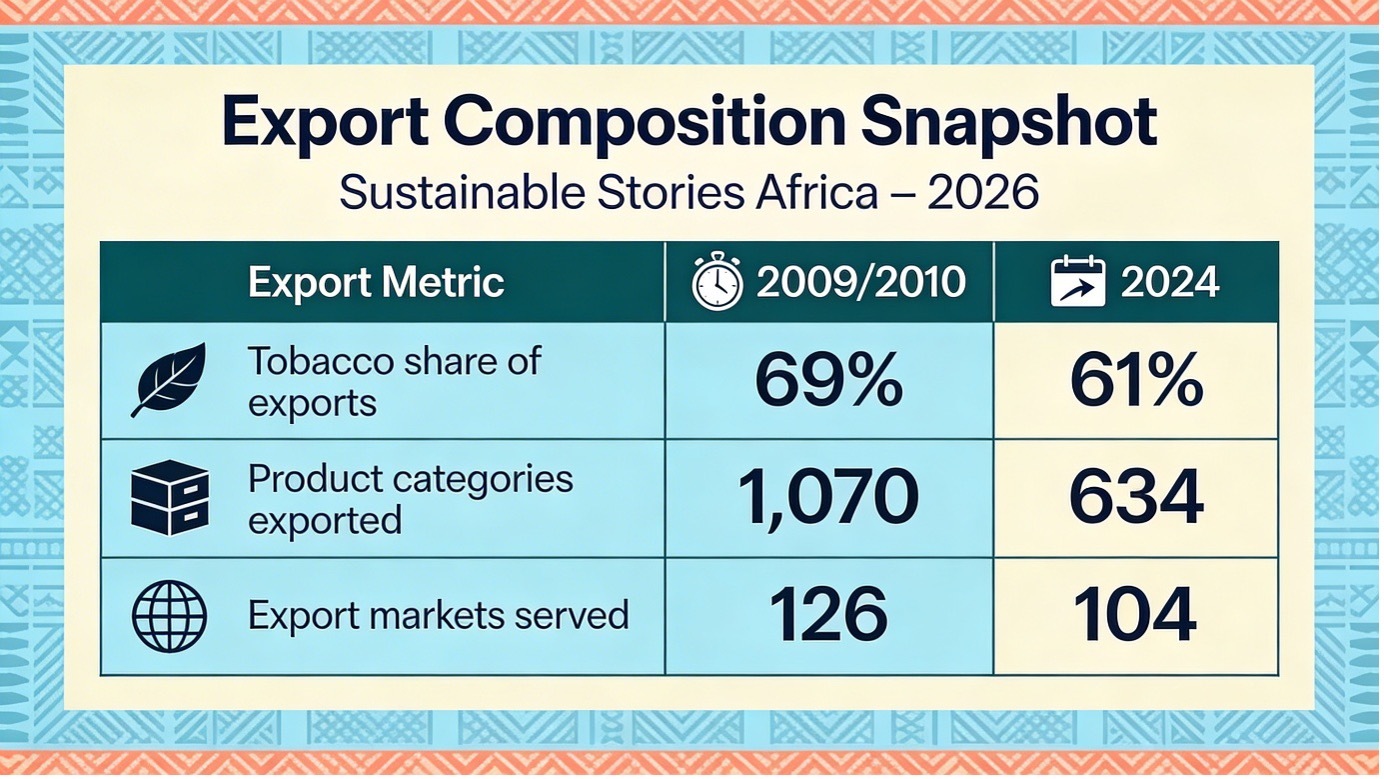

Export Composition Snapshot

Export Metric | 2009/2010 | 2024 |

|---|---|---|

Tobacco share of exports | 69% | 61% |

Product categories exported | 1,070 | 634 |

Export markets served | 126 | 104 |

The numbers show contraction, not expansion.

However, there are glimmers of possibility. Emerging agro-processing chains, including macadamia, soybeans, and groundnuts, have demonstrated that coordination, predictable policy and patient capital can generate export momentum.

The lesson is not that Malawi cannot diversify. It is that diversification requires coherence.

Reform Must Restore Credibility Fast

The reform blueprint outlined in the report is clear.

- Immediate Priorities (Sprints)

- Eliminate inefficient VAT exemptions

- Conclude external commercial debt restructuring

- Unify exchange rates

- Phase out forex surrender requirements

- Replace trade bans with SADC-compliant measures

- Medium-Term Priorities (Marathons)

- Digitise customs and export systems

- Improve public-sector efficiency via e-procurement

- Restructure domestic debt

- Strengthen energy generation and regional interconnections

- Modernise mining governance and land reforms

These are not technocratic tweaks. They are credibility restorations.

Macroeconomic stabilisation must anchor everything else. Without it, the ability for private sector investment remains cautious, exporters remain defensive, and households remain vulnerable.

PATH FORWARD – Stability, Credibility and Export-Led Renewal

Malawi must re-anchor fiscal discipline, unify its exchange rate regime and reduce policy unpredictability to restore investor confidence.

Export competitiveness, through trade facilitation, digital systems and removal of non-tariff barriers, should become the central growth strategy.

If reforms are sustained and sequenced coherently, Malawi can convert crisis into a structural reset. Delay, however, will deepen fragility and further narrow the policy space.