By David Olujinmi

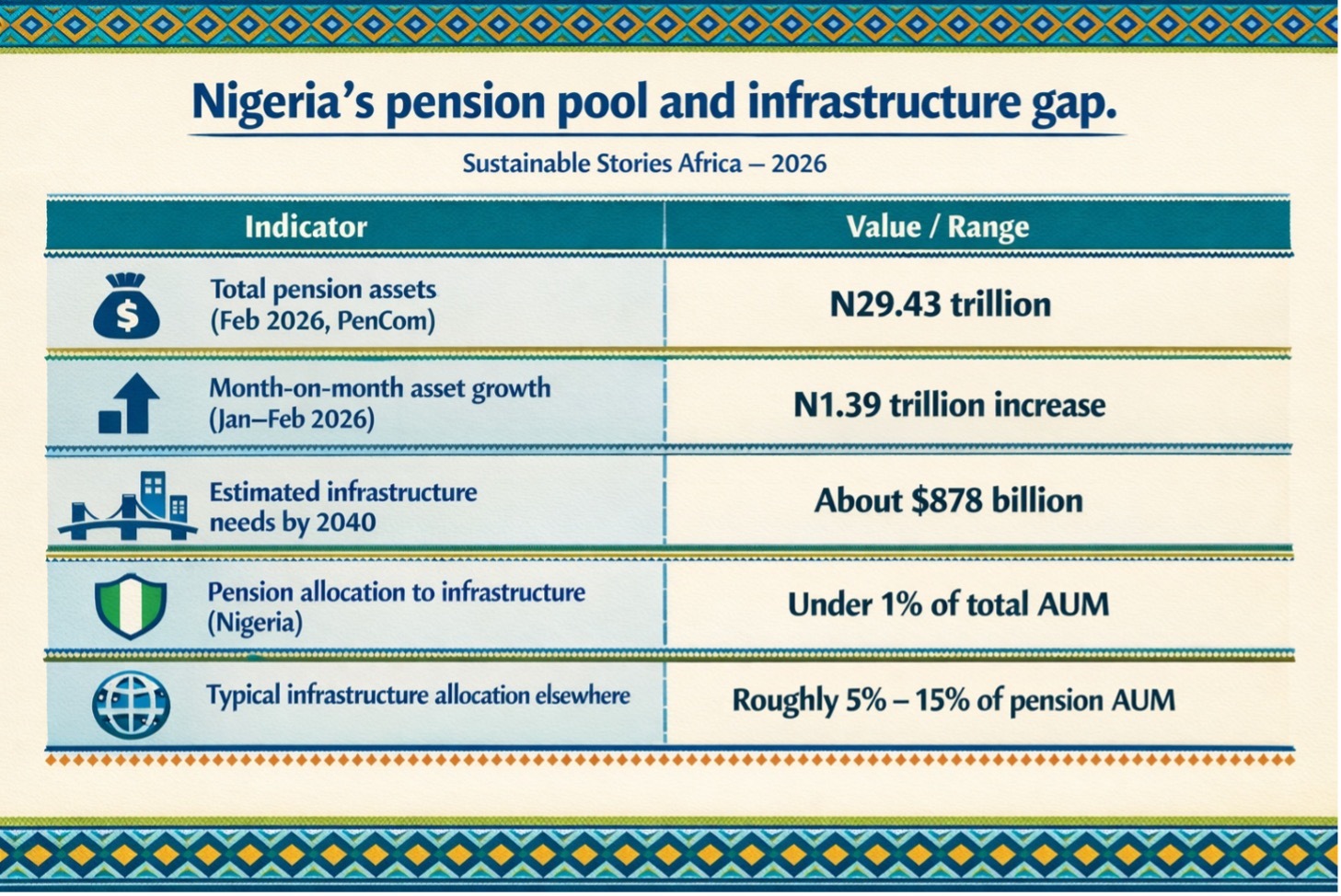

Nigeria holds N29.43 trillion in pension assets yet channels under 1% into infrastructure, even as the country faces an estimated $878 billion investment gap through 2040.

This piece argues that a Capital Market National Deal Room, as proposed by Bolaji Balogun of Chapel Hill Denham, is the most credible bridge between idle savings and urgent national need.

For Africa and emerging markets alike, Nigeria's coordination challenge is a live test of whether local capital can build climate-resilient futures without waiting on fiscal space that may never arrive.

Pension Savings Must Build Nigeria's Future

Nigeria's N29.43 trillion pension pool has grown large enough to move from the margins of the country's infrastructure story to its centre.

However, that shift will only happen if regulators, pension funds, and deal-makers accept a new coordination logic, one that treats infrastructure as an asset class, not an afterthought.

Building on Proshare's Infrastructure, Fiscal Space, and Capital Market Funding conversation and Sustainable Stories Africa's analysis, our argument is that a Capital Market National Deal Room is the most credible mechanism to bridge the gap between Nigeria's record pension savings and its estimated $878 billion infrastructure investment requirement through 2040.

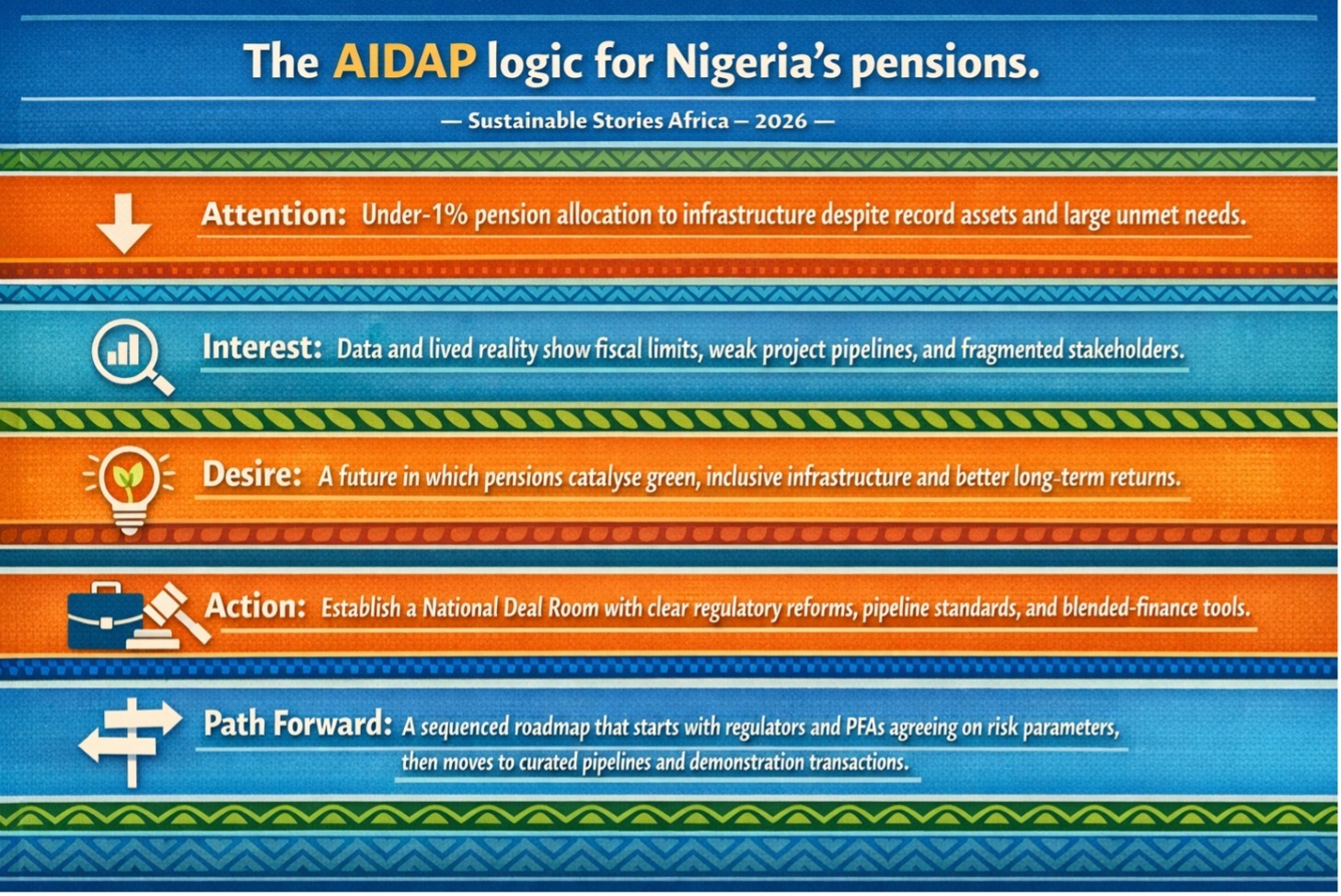

As 'Olufemi AWOYEMI, mni, rightly notes, the Proshare paper is a market signal, not a full policy blueprint. However, the signal demands urgent attention: allocating under 1% of pension assets to infrastructure, in a country with this scale of savings and this depth of need, is no longer defensible.

The proposal by Bolaji Balogun of Chapel Hill Denham for a National Deal Room deserves to be interrogated, sharpened, and funded at scale.

For African and emerging markets facing identical fiscal and climate pressures, Nigeria's choices now will determine whether local savings build resilient futures or remain spectators to decline.

Pension Savings, Empty Infrastructure, Tight Space

Nigeria’s pension assets have climbed to a record N29.43 trillion, even as the country faces an estimated $878 billion infrastructure investment requirement through 2040 and shrinking fiscal space.

The numbers, highlighted in Proshare’s HardFacts discussion and a recent Sustainable Stories Africa analysis, sharpen a simple question: why is less than 1% of this pool reaching infrastructure in a country that desperately needs roads, power, and climate‑resilient systems?

This piece takes the view, shared and refined in commentary by ‘Olufemi AWOYEMI, mni, that the answer lies less in “lack of capital” and more in weak coordination, poor pipeline preparation, and timid regulation.

A National Capital Market Deal Room, as proposed by Bolaji Balogun on Proshare’s HardFacts Episode 9, is not a silver bullet, but a realistic mechanism to turn pension assets into investable infrastructure deals and a template that other African markets can adapt.

Under 1%: Africa's Most Expensive Missed Allocation

Nigeria's pension industry has achieved what many African markets still dream about: N29.43 trillion in long-term savings by February 2026, the strongest monthly expansion in over two decades.

However, pension fund administrators allocate less than 1% of total assets under management to infrastructure, well below the 5% – 15% range that other markets operate.

The consequences are tangible and daily. Fiscal space remains constrained by debt service obligations. Development banks cannot bridge the gap alone, and citizens have to live with the real costs of poor roads, unreliable power, and the absence of digital infrastructure.

Keeping pension capital parked in sovereign debt and vanilla securities is not prudent; it is a costly mispricing of risk that deepens under-investment in human development and climate resilience.

The Capital Market National Deal Room addresses this gap directly. It proposes a Nigeria-specific mechanism that can convince pension trustees that infrastructure is both bankable and rewarding over the long term.

Why The Money Won’t Move Itself

To understand why this “under‑1%” is so sticky, we need to unpack the ecosystem that AWOYEMI describes as a “five‑actor coordination framework”,

- Government

- Regulators

- PFAs

- Capital market intermediaries

- Project sponsors.

His opinion is that the framework, as currently drafted, reads like a catalogue rather than a sequenced implementation logic; everyone is listed, but no one is clearly assigned the first move.

Consider the current reality.

- Government is fiscally constrained and tends to see pension assets as quasi‑public money rather than strictly governed savings.

- Regulators are rightly conservative, wary of saddling retirees with the fallout of failed projects.

- PFAs are judged quarterly on mark‑to‑market performance and benchmarked against peers heavily loaded in federal government securities.

- Project sponsors often arrive at the market with incomplete feasibility studies, unclear revenue models, and shaky governance structures.

- Capital market intermediaries are willing to structure, but cannot conjure away underlying project risks.

Signals Without Sequencing Risk Policy Graveyard

Across East Africa and other emerging markets, dedicated infrastructure funds, credible PPP frameworks, and blended-finance vehicles have successfully mobilised pension capital at scale.

Nigeria has fragments of this architecture, including listed infrastructure funds, early PPP experiments, but they remain fragmented and underscaled, as PenCom data confirm.

Signals are valuable, but in a country where infrastructure gaps are actively eroding productivity, climate resilience, and investor confidence, market signals must rapidly translate into sequenced action, or risk becoming another well-intentioned document filed away without consequence.

When Workers’ Savings Build Their Own Future

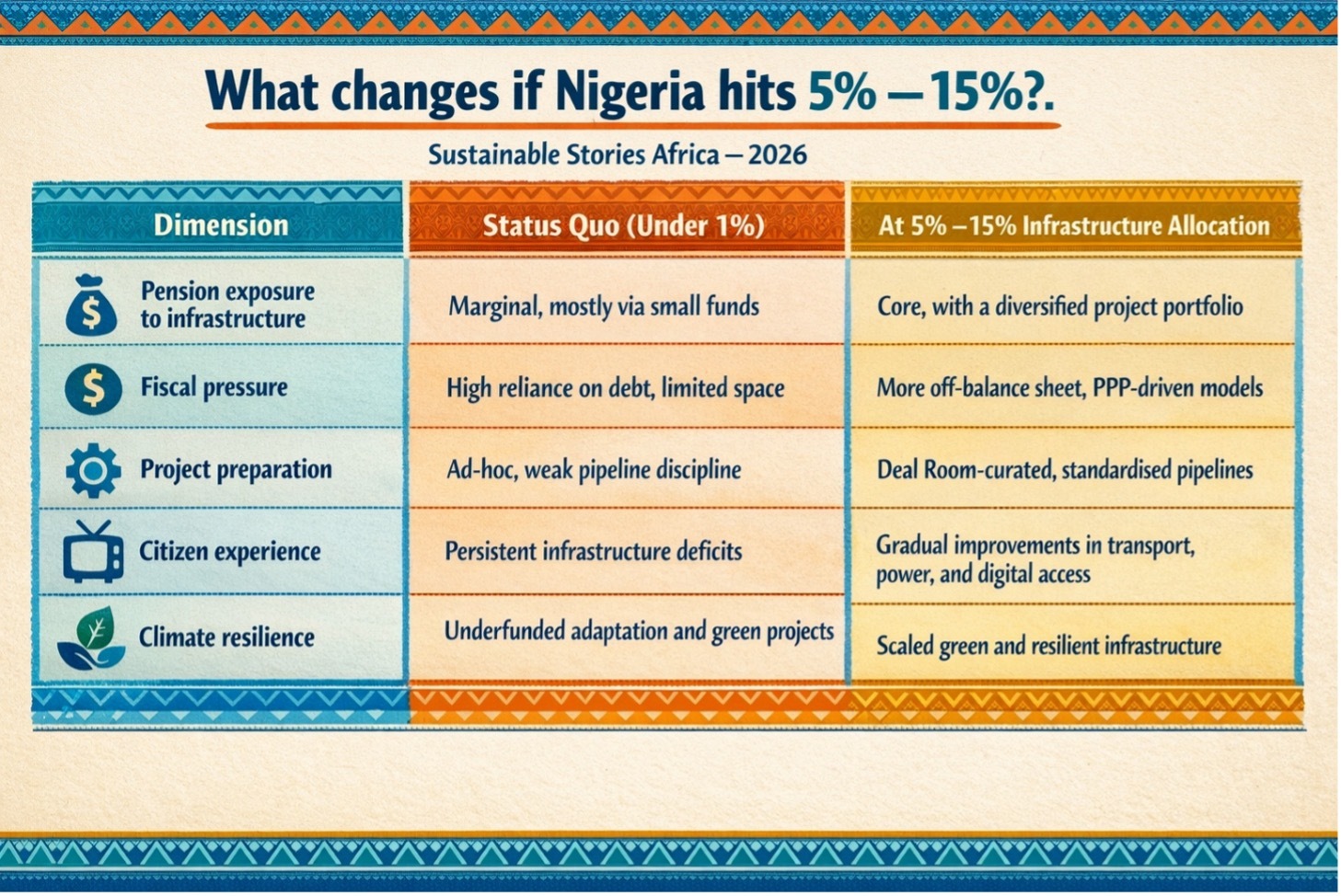

If Nigeria moves from under 1% to even the lower end of the 5% – 15% infrastructure allocation bands seen in comparable markets, the impact over a 10 – 15-year horizon would be transformative.

A fraction of the N29.43 trillion pension pool, compounded by continued contribution growth driven by increased job creation opportunities and investment gains, could anchor roads, mass transit systems, renewable energy parks, digital infrastructure, and climate-resilient water and housing projects at the national scale.

For citizens and communities, the change would be tangible, with lower logistics costs, more predictable business environments, and better-paid jobs across construction, operations, and supply chains.

For markets and institutions, infrastructure-linked instruments offer long-duration, inflation-hedged cash flows that match pension liabilities more efficiently than short-dated sovereign securities, provided structures are transparent and revenue models are credible.

There is also a political dividend. When workers see their retirement savings professionally managed and visibly tied to public infrastructure, they use daily, trust in both the pension system and the broader social contract deepens, a non-financial asset no African democracy can afford to waste.

Three Actors, One Sequence, No Excuses

The five-actor coordination framework that Olufemi AWOYEMI, mni, identifies becomes a genuine strength only when Nigeria is explicit about who moves first and under what conditions. In practice, three actors must lead in order, without ambiguity.

- Regulators – PenCom, SEC, and relevant PPP and infrastructure agencies, must move first by defining and publicising a clear, evidence-based risk framework for pension investment in infrastructure.

This means setting realistic exposure bands, clarifying eligible instruments, and mandating strict governance, ESG, and reporting standards for every vehicle seeking pension capital.

Without this regulatory north star, PFAs will continue defaulting to sovereign securities as the path of least resistance.

- Second, PFAs and capital market intermediaries must co-design the Capital Market National Deal Room, with regulators embedded as rule-setters from inception, not consulted after the fact.

The Deal Room, operating as a permanent physical and digital platform, should maintain a rolling pipeline of vetted infrastructure opportunities from early-stage to financial close, standardise transaction documentation, embed climate resilience and just-transition principles, and structure blended-finance solutions that credibly de-risk early projects for pension capital.

- Third, the federal and state governments must commit to a transparent pipeline of priority projects backed by clear legal, tariff, and land frameworks.

The government's role is to provide guarantees, viability gap funding, and policy stability, not to treat pension assets as off-budget fiscal relief.

Path Forward – Sequencing Markets, Savings, and State

Nigeria no longer has a capital shortage; it has a coordination and courage deficit, and that is fixable if regulators, PFAs, and government accept a sequenced roadmap for pension‑backed infrastructure.

The immediate priorities are clear: enshrine a robust regulatory risk framework, operationalise a National Deal Room with real projects and real money, and move decisively from under 1% to a disciplined, transparent 5% – 15% infrastructure allocation band over time.