A quiet revolution is reshaping inclusion, climate and capital interrelate. However, a high amount of research and innovations is still happening far from the communities most exposed to risk.

As sustainable financial inclusion matures, it is becoming less about access alone and more about who designs the rules, owns the data, and captures the green premium.

When inclusion meets a warming world

Sustainable financial inclusion has moved from a fringe academic concept to a defining fault line in global finance, linking access to money with climate resilience, social equity and green growth.

According to an IRENA report, between 2007 and the middle of 2025, as per peer‑reviewed research, sustainable financial inclusion surged to 1,467 documents, with annual publications spiking from 40 in 2017 to 383 in 2024, signalling an inflexion point in how scholars and policymakers frame the issue.

However, this intellectual boom is geographically skewed: China, India and Pakistan alone account for more than 77% of global publications. Sub‑Saharan Africa and Central Asia remain starkly under‑represented despite facing the most acute financing and climate vulnerabilities.

At the same time, the centre of gravity has shifted from basic access to accounts toward digital finance, ESG integration, green credit and financial literacy, reframing inclusion as a lever for the Sustainable Development Goals rather than a poverty‑reduction tool.

Behind the numbers is a deeper story about power, technology and transition risk. Digital rails, green bonds and ESG‑linked loans can either widen or narrow inequality depending on whether regulatory frameworks, literacy levels and local data shape the products, or whether global platforms simply share a one-size-fits-all model for fragile markets.

Eight clusters, one defining question

The bibliometric map of 1,467 articles reveals eight major thematic clusters that together ask one pressing question: Will the next generation of financial innovation reduce or reinforce climate inequality?

Digital financial inclusion and FinTech dominate citation networks; however, they are tightly coupled with environmental metrics such as carbon emissions, energy intensity and ecological footprint, rather than treated as purely economic variables.

Evidence is that digital tools can both narrow income gaps and accelerate decarbonisation. Studies in the "FinTech and inequality" cluster show that access to mobile and platform‑based services can significantly reduce income inequality for low‑income groups.

Other related work links digital inclusion to lower poverty vulnerability among farmers through diversified income streams. At the same time, clusters focused on CO₂ emissions and energy transition find that financial inclusion, when paired with energy‑efficient technologies and renewable electricity, can bend emission curves; however, poorly governed credit expansion can lock in high‑carbon consumption.

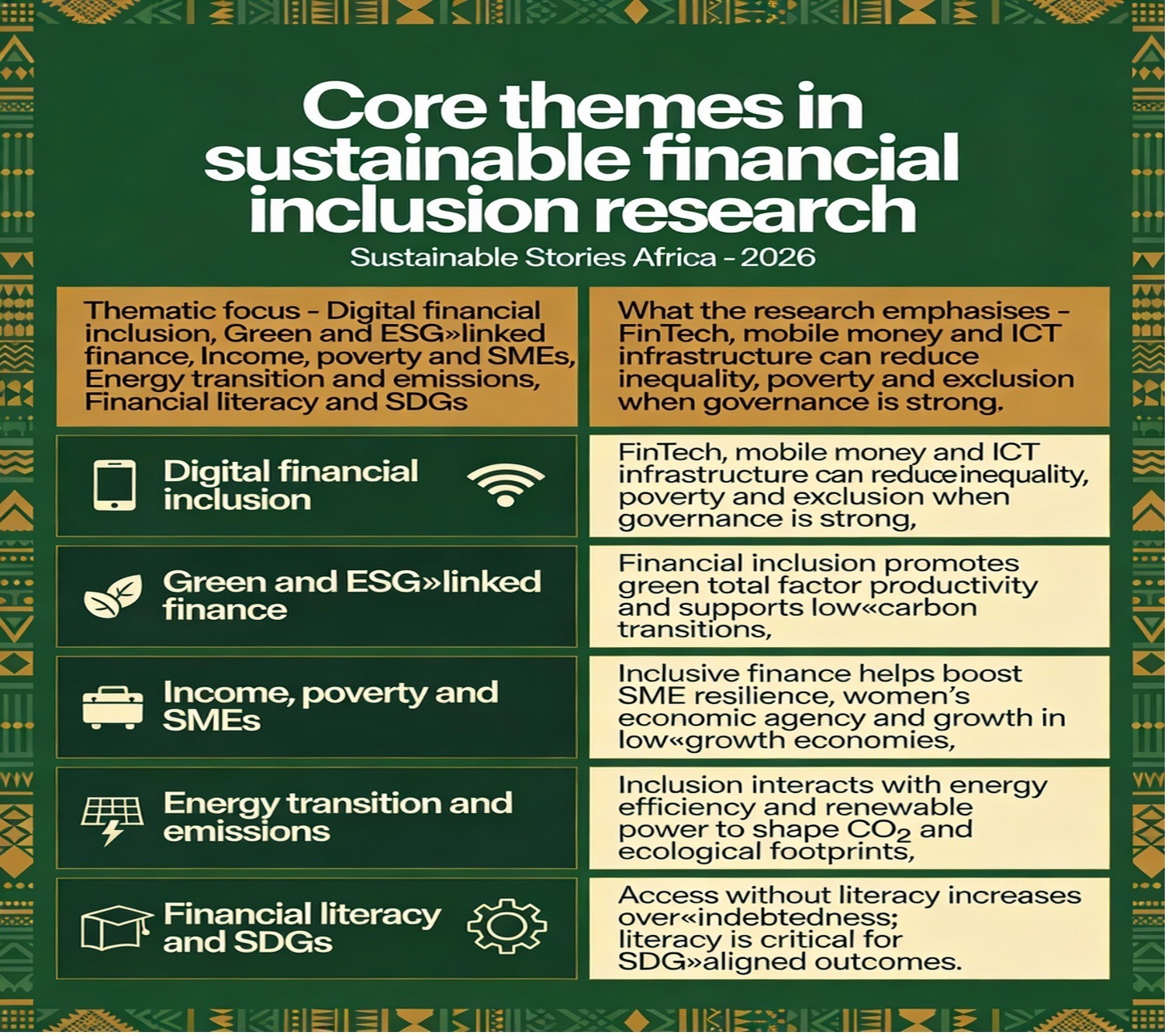

Core themes in sustainable financial inclusion research

| Thematic focus | What the research emphasises |

|---|---|

| Digital financial inclusion | FinTech, mobile money and ICT infrastructure can reduce inequality, poverty and exclusion when governance is strong. |

| Green and ESG‑linked finance | Financial inclusion promotes green total factor productivity and supports low‑carbon transitions. |

| Income, poverty and SMEs | Inclusive finance helps boost SME resilience, women's economic agency and growth in low‑growth economies. |

| Energy transition and emissions | Inclusion interacts with energy efficiency and renewable power to shape CO₂ and ecological footprints. |

| Financial literacy and SDGs | Access without literacy increases over‑indebtedness; literacy is critical for SDG‑aligned outcomes. |

Who is writing the rules, and where?

The intellectual architecture of this field is not accidental; it reflects where data, capital and digital infrastructure are concentrated.

Citation and co‑citation analyses position a handful of scholars and journals, from Demirgüç‑Kunt and his co‑authors on global financial inclusion to high‑impact outlets like Sustainability, Journal of Cleaner Production and Technological Forecasting and Social Change, as setting the agenda on how inclusive, green finance should be measured and regulated.

Geographically, China and India dominate both publication volume and network centrality. They are joined by the USA, Spain and the UK, while Africa is represented mainly by Nigeria and South Africa.

This mirrors where digital payments ecosystems, open data and ESG regulation have advanced fastest. However, this also means that many of the models being cited and replicated are calibrated towards middle‑income digital economies, not low‑capacity regulators overseeing fragmented microfinance systems.

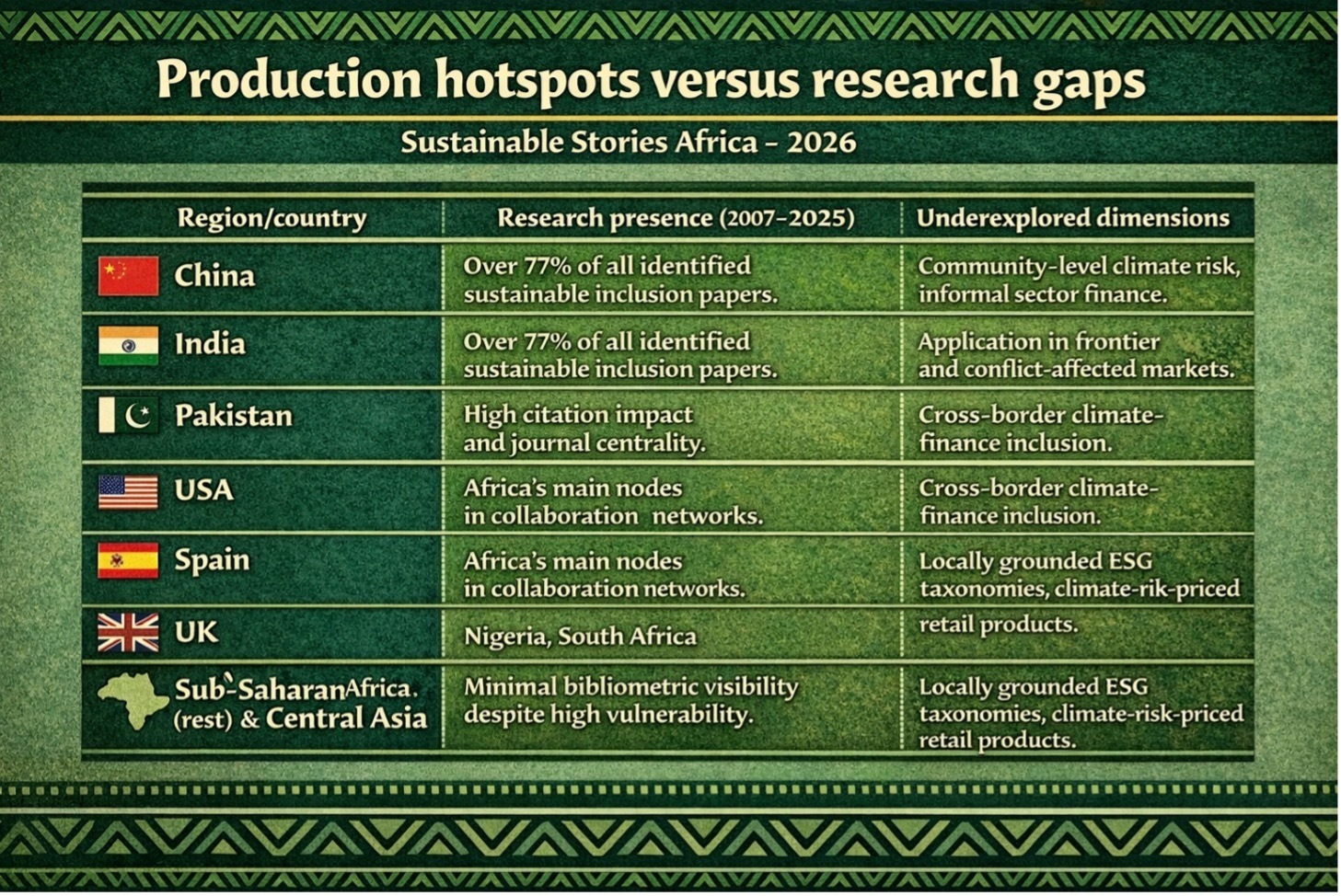

Production hotspots versus research gaps

| Region/country | Research presence (2007–2025) | Underexplored dimensions |

|---|---|---|

| China, India, Pakistan | Over 77% of all identified sustainable inclusion papers. | Community‑level climate risk, informal sector finance. |

| USA, Spain, UK | High citation impact and journal centrality. | Application in frontier and conflict‑affected markets. |

| Nigeria, South Africa | Africa's main nodes in collaboration networks. | Cross‑border climate‑finance inclusion, regional regulatory design. |

| Sub‑Saharan Africa (rest) & Central Asia | Minimal bibliometric visibility despite high vulnerability. | Locally grounded ESG taxonomies, climate‑risk‑priced retail products. |

The geography of knowledge matters. When the most cited work on "inclusive green finance" is built around data‑rich Asian and OECD contexts, it risks becoming the default blueprint for regulators and banks in places where informal livelihoods, climate shocks and governance constraints look very different.

From access metrics to triple‑bottom‑line systems

Across clusters, one conclusion keeps resurfacing: sustainable financial inclusion must be designed as a triple‑bottom‑line system balancing people, planet and profit. It should not be seen as an exercise in opening more accounts.

Studies linking inclusion to ecological footprint, energy structure and CO₂ emissions show that the quality of products: What is financed and on what terms, is at least as important as the quantity of credit.

When inclusion is aligned with green credit, ESG-screened portfolios, and targeted incentives for clean technologies, it becomes a lever for energy transition—reducing environmental degradation while strengthening long-term financial stability.

However, when inclusion merely accelerates consumption of energy-intensive goods, without parallel investment in efficiency, literacy, and demand-side management, it expands the ecological footprint even as it delivers fragile, short-term resilience.

For African and other under‑represented regions, the opportunity lies in leapfrogging into inclusion models that are "green‑by‑design": digital rails that default to clean‑energy loans for SMEs, savings products linked to adaptation projects, and climate‑indexed insurance tailored to smallholders.

The bibliometric evidence underscores that such models require not only FinTech and data, but also capable governance institutions and context‑specific ESG frameworks grounded in local development priorities.

Five practical levers for inclusive green finance

The review's synthesis points to a concrete policy and market agenda that goes beyond rhetoric about "win‑wins" to focus on institutions, incentives and skills. For regulators in Africa and other climate‑vulnerable markets, five levers emerge from the global evidence:

- Hard‑wire sustainability into inclusion policy – National financial inclusion strategies should explicitly integrate ESG criteria, green microfinance targets and climate‑risk disclosure for banks and FinTechs, rather than treating climate as a separate agenda.

- Invest in digital rails with governance – The countries that lead the literature combine digital payment infrastructure with clear rules on interoperability, consumer protection and data governance.

- Make literacy a core climate‑finance tool – Studies show that access without financial literacy can increase over‑indebtedness and mispricing of risk; embedding sustainability‑focused literacy into inclusion programmes is critical to avoid "greenwashed" debt traps.

- Scale-inclusive green instruments – From blended‑finance vehicles and social impact bonds to small‑ticket green loans, the most promising experiments link concessional capital with pro‑poor, climate‑positive products for SMEs, women‑led enterprises and rural households.

- Close the research gap where risk is highest – The bibliometric imbalance calls for deliberate investment in Africa and Central Asia‑led research. This includes local repositories and multi‑lingual databases. This ensure s that models for sustainable inclusion are informed by ground realities, not just imported metrics.

Path Forward – Local knowledge, global stakes, narrowing window

The bibliometric record issues a clear warning: research on sustainable financial inclusion is advancing faster than the practice s in the regions that need it most. On current trajectories, the architecture of inclusive green finance, ranging from ESG taxonomies to digital credit scoring, will be designed in data-rich economies, then transplanted into markets with very different vulnerabilities and social contracts.

Correcting the course will require more than pilots. It means resourcing African and other underserved research institutions, integrating community-based evidence into a quantitatively dominant area, and holding SDG-aligned finance accountable to those most exposed to climate and financial shocks.

The 2007-2025 trajectory shows what is possible; the next decade will test whether growth can be matched with justice.