Ghana's green finance narrative is often framed as a story of promise and policy momentum. The data tells a more sobering, more useful story.

Despite expanding climate finance flows, public money still dominates, private capital remains hesitant, and industrial transformation lags ambition.

New evidence from the SAGFA Ghana 2025 report shows why green finance has yet to fully reshape manufacturing and what must change for Ghana's climate ambition to translate into durable industrial growth.

When Green Finance Meets Industrial Reality

Ghana has emerged as one of West Africa's most policy-active markets on green finance. From Sustainable Banking Principles to a national Green Finance Taxonomy, climate considerations are now embedded in financial regulation, national development planning, and international partnerships. On paper, the foundations of green industrialisation appear solid.

However, the Sino-African Green Finance Alliance (SAGFA) Ghana 2025 report reveals a persistent gap between ambition and execution. Annual green finance flows are estimated at $830 million, still below the $900 – $1.55 billion required each year to meet Ghana's climate and industrial goals.

More critically, 87% of tracked finance remains public, leaving private capital marginal to the transition.

This imbalance matters. Green industrialisation, particularly in manufacturing, agro-processing, and energy-intensive value chains, cannot scale on concessional funding alone. Ghana's challenge is no longer defining green finance, but making it work for industry, productivity, and jobs.

A System Growing, but Still Imbalanced

Green finance is no longer peripheral in Ghana's policy architecture. Climate objectives are woven into the Nationally Determined Contributions, industrial strategies, and public financial management reforms. Dedicated climate units now sit within the Ministry of Finance, while regulators promote ESG integration across banks and capital markets.

However, the structure of finance remains skewed. The SAGFA report shows that public and international sources dominate, while domestic banks and institutional investors remain cautious, constrained by risk perceptions, shallow capital markets, and limited project pipelines.

The risk is structural inertia: a system that mobilises funds, but not transformation.

Following the Money: Sources, Instruments, Sectors

The report provides one of the most detailed mappings of Ghana's green finance ecosystem to date.

Scale and Sources of Green Finance in Ghana

| Source | Share of Total Climate Finance |

|---|---|

| Public (Government + Multilateral/Bilateral) | 87% |

| Private Sector | 12.8% |

Public finance includes domestic budget allocations and flows from institutions such as the World Bank, AfDB, GCF, CIFs, and bilateral partners. Private contributions—around $106 million annually – remain modest and concentrated in niche impact investments and blended structures.

Instruments Used in Ghana’s Green Finance Mix

Instrument Type | Approximate Share |

|---|---|

Grants | 45% |

Concessional Loans | 35% |

Market-rate Loans & Equity | 20% |

This heavy reliance on grants and concessional finance reflects debt constraints and perceived project risks but also limits scalability and market discipline.

Sectoral allocation shows a near-even split between adaptation (53%) and mitigation (47%), with agriculture, forestry, water, and energy dominating flows. Manufacturing and industrial upgrading receive comparatively limited attention, despite their centrality to long-term growth.

Why Industrial Transformation Remains Elusive

The report's most consequential insight is not about funding volumes, but institutional readiness.

Despite strong policy frameworks, such as the Sustainable Banking Principles (2019), Green Bond Guidelines, and the Green Finance Taxonomy (2024), implementation remains uneven. Enforcement is largely voluntary, ESG supervision is still evolving, and coordination across ministries and regulators is fragmented.

Local banks have begun experimenting with green lending, but activity remains project-specific and externally driven.

Selected Green Lending Initiatives by Ghanaian Banks

| Bank / Program | Focus Area |

|---|---|

| GCB & CalBank (SUNREF) | Renewable energy, energy efficiency |

| Absa Bank Ghana | Utility-scale solar |

| Ecobank Ghana | Climate-smart agriculture |

| DBG Green Window | SME green investments |

These initiatives demonstrate progress but not scale. Manufacturing firms, particularly SMEs, still struggle with feasibility costs, technical standards, and access to long-term finance.

The result is a paradox: green finance exists, but green industry struggles to bank it.

From Fragmented Flows to Functional Markets

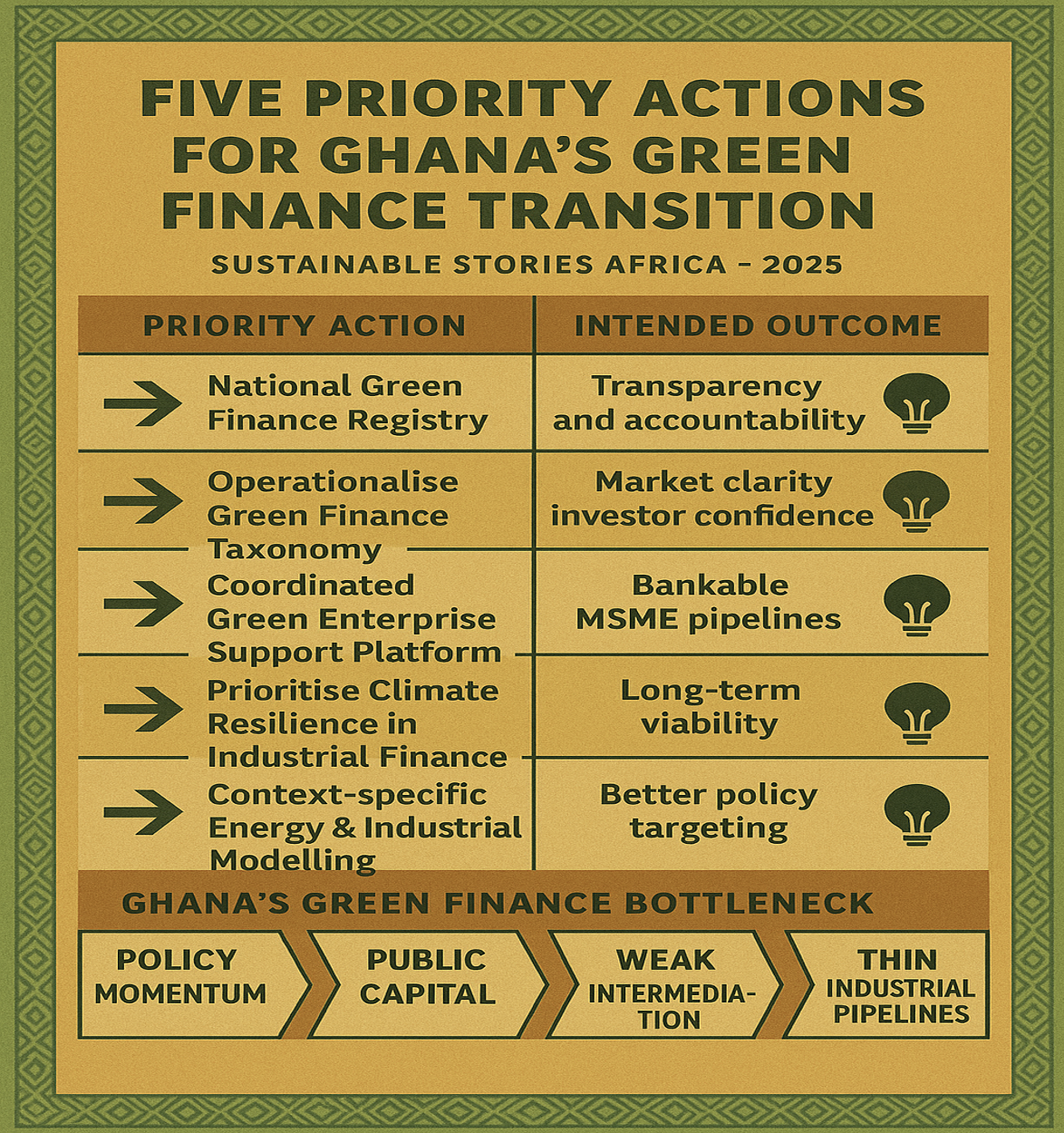

The SAGFA report identifies a clear pathway for unlocking Ghana's green industrial potential, one rooted in execution rather than new pledges.

Five Priority Actions for Ghana's Green Finance Transition

| Priority Action | Intended Outcome |

|---|---|

| National Green Finance Registry | Transparency and accountability |

| Operationalise Green Finance Taxonomy | Market clarity, investor confidence |

| Coordinated Green Enterprise Support Platform | Bankable MSME pipelines |

| Prioritise Climate Resilience in Industrial Finance | Long-term viability |

| Context-specific Energy & Industrial Modelling | Better policy targeting |

International partnerships, particularly under FOCAC, remain important, but the report urges Ghana to move from passive recipient to strategic architect, aligning external finance with domestic industrial priorities.

PATH FORWARD – Turning Finance into a Green Industry

Ghana's green finance challenge is no longer about frameworks, but follow-through. Stronger enforcement, coordinated institutions, and credible project pipelines must now take centre stage.

By shifting focus from fragmented funding to functional markets—where private capital, domestic banks, and industrial actors align—green finance can become a true engine of sustainable industrialisation, not just a policy aspiration.